01

MethodologyHow they did it

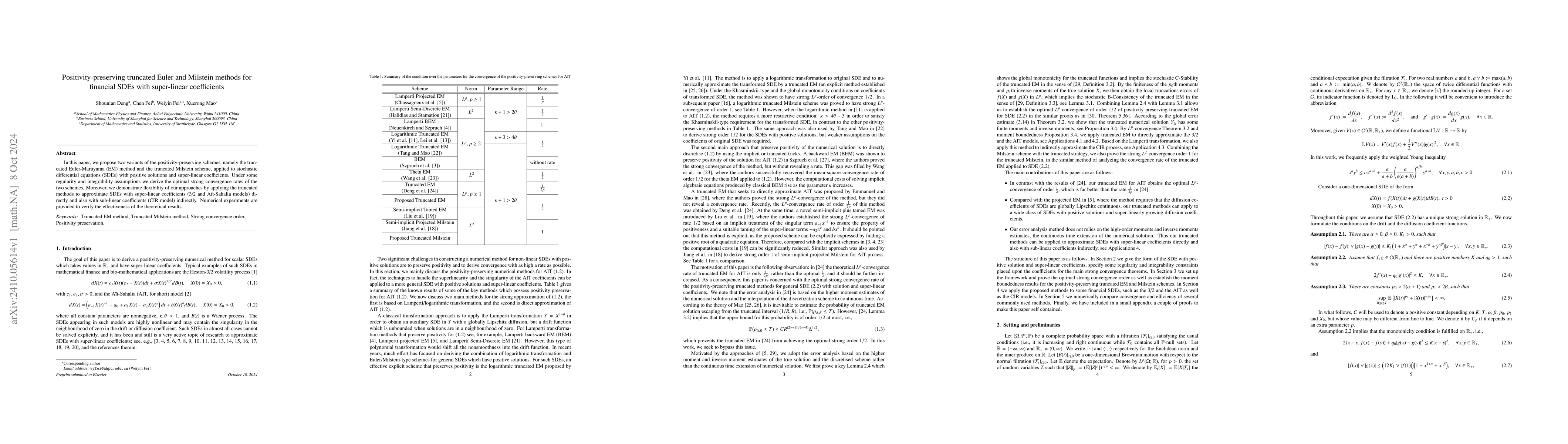

The paper proposes two positivity-preserving numerical schemes, the truncated Euler-Maruyama (EM) method and the truncated Milstein scheme, for stochastic differential equations (SDEs) with positive solutions and super-linear coefficients. It derives optimal strong convergence rates under certain regularity and integrability assumptions.

Discussion 0