Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper mainly investigates the strong convergence and stability of the truncated Euler-Maruyama (EM) method for stochastic differential delay equations with variable delay whose coefficients can...

Based on the classical probability, the stability criteria for stochastic differential delay equations (SDDEs) where their coefficients are either linear or nonlinear but bounded by linear functions...

In this paper, we consider the generalized Ait-Sahaliz interest rate model with Poisson jumps in finance. The analytical properties including the positivity, boundedness and pathwise asymptotic esti...

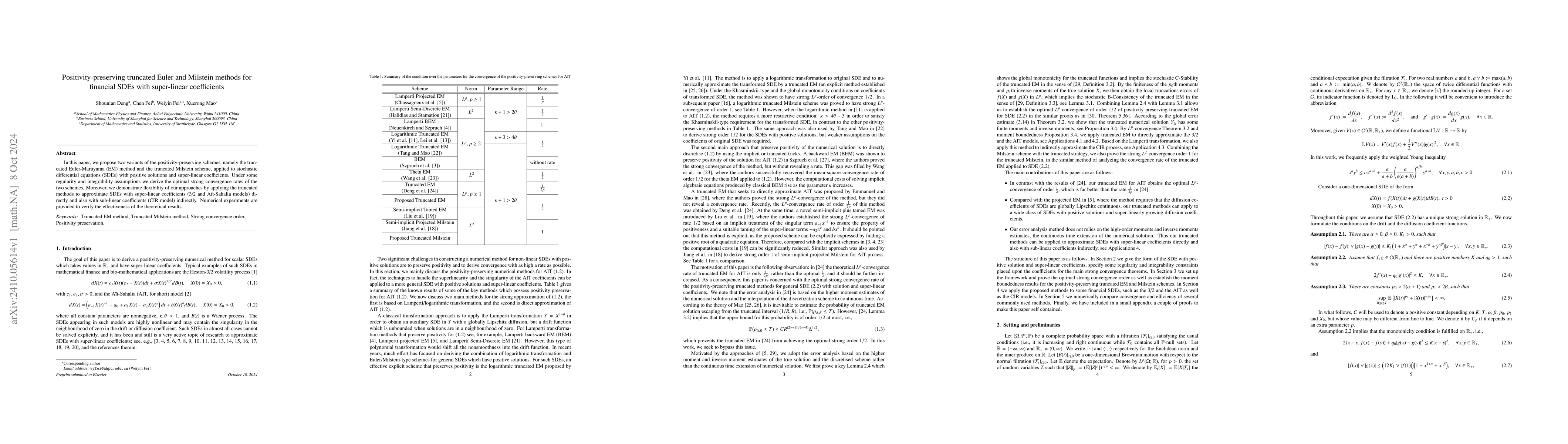

In this paper, we propose two variants of the positivity-preserving schemes, namely the truncated Euler-Maruyama (EM) method and the truncated Milstein scheme, applied to stochastic differential equat...

Considering that the decision-making environment faced by reinforcement learning (RL) agents is full of Knightian uncertainty, this paper describes the exploratory state dynamics equation in Knightian...

Most existing literature focuses on pointwise convergence (i.e., convergence at a fixed time point) of numerical solutions for Stochastic functional differential equations (SFDEs). In contrast, this p...