Academic Profile

Statistics

Similar Authors

Papers on arXiv

The G-Brownian-motion-driven stochastic differential equations (G-SDEs) as well as the G-expectation, which were seminally proposed by Peng and his colleagues, have been extensively applied to descr...

Releasing sterile Wolbachia-infected mosquitoes to invade wild mosquito population is a method of mosquito control. In this paper, a stochastic mosquito population model with Wolbachia invasion pert...

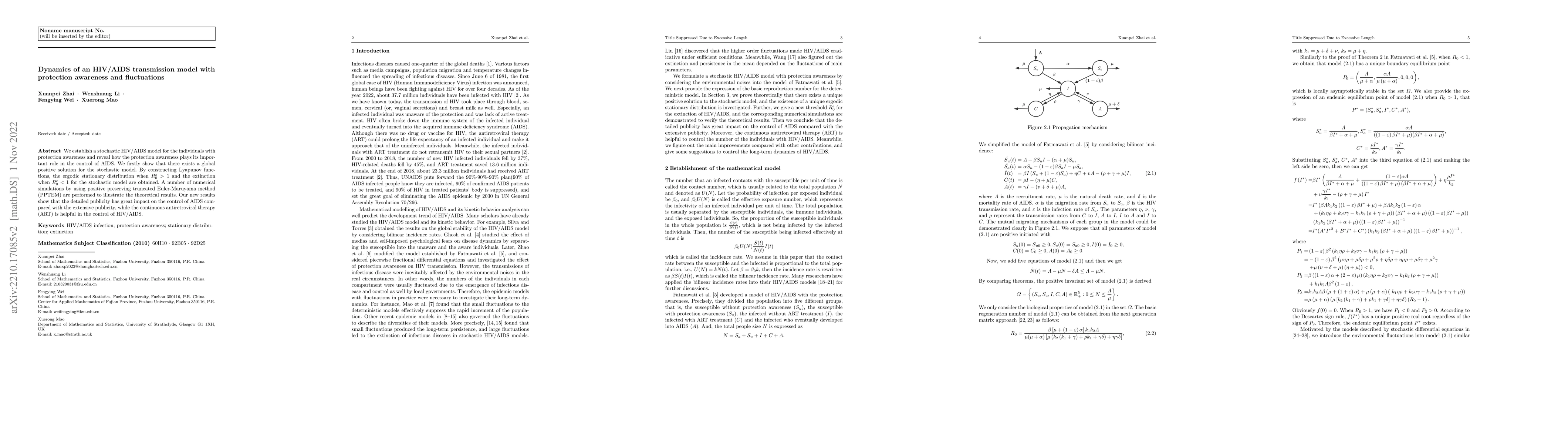

We establish a stochastic HIV/AIDS model for the individuals with protection awareness and reveal how the protection awareness plays its important role in the control of AIDS. We firstly show that t...

Since it is difficult to implement implicit schemes on the infinite-dimensional space, we aim to develop the explicit numerical method for approximating super-linear stochastic functional differenti...

The backward Euler-Maruyama (BEM) method is employed to approximate the invariant measure of stochastic differential equations, where both the drift and the diffusion coefficient are allowed to grow...

Fractional Brownian motion with the Hurst parameter $H<\frac{1}{2}$ is used widely, for instance, to describe a 'rough' stochastic volatility process in finance. In this paper, we examine an Ait-Sah...

This paper mainly investigates the strong convergence and stability of the truncated Euler-Maruyama (EM) method for stochastic differential delay equations with variable delay whose coefficients can...

Based on the classical probability, the stability criteria for stochastic differential delay equations (SDDEs) where their coefficients are either linear or nonlinear but bounded by linear functions...

In this article we introduce several kinds of easily implementable explicit schemes, which are amenable to Khasminski's techniques and are particularly suitable for highly nonlinear stochastic diffe...

In this paper, we consider the generalized Ait-Sahaliz interest rate model with Poisson jumps in finance. The analytical properties including the positivity, boundedness and pathwise asymptotic esti...

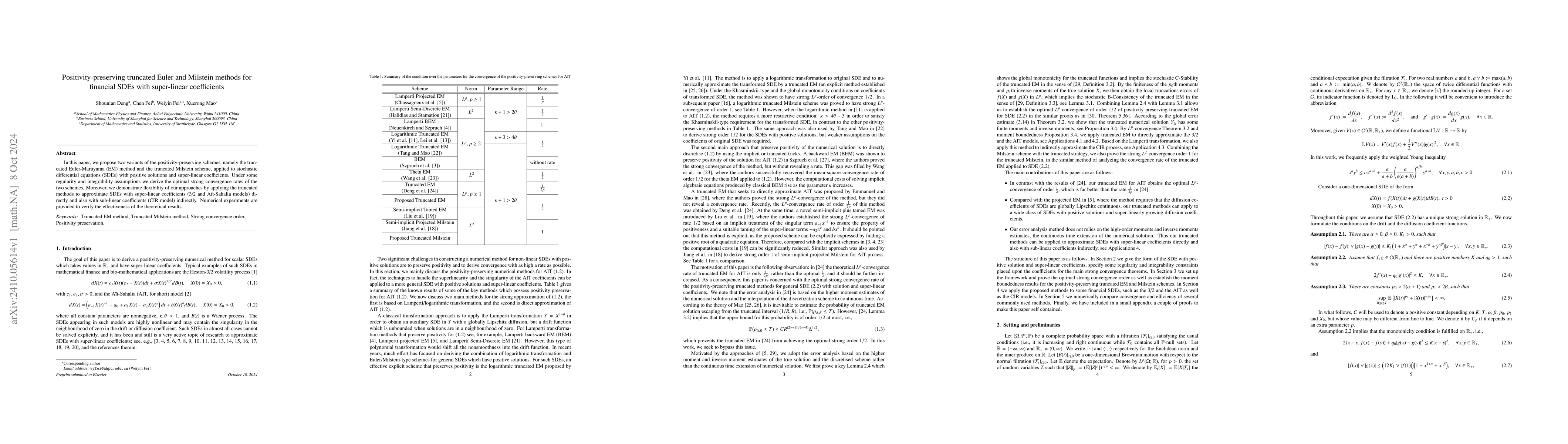

In this paper, we propose two variants of the positivity-preserving schemes, namely the truncated Euler-Maruyama (EM) method and the truncated Milstein scheme, applied to stochastic differential equat...

In this paper, we introduce a linear stochastic volatility model driven by $\alpha$-stable processes, which admits a unique positive solution. To preserve positivity, we modify the classical forward E...

This paper focuses on explicit numerical approximations for nonlinear hybrid stochastic functional differential equations with infinite delay. Precisely, explicit truncated Euler-Maruyama schemes are ...

This paper is to investigate if the solution of a hybrid stochastic functional differential equation (SFDE) with infinite delay can be approximated by the solution of the corresponding hybrid SFDE wit...

This paper studies explicit numerical approximations of the invariant probability measures (IPMs) for stochastic functional differential equations (SFDEs) with infinite delay under one-sided Lipschitz...