Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider the computation of model-free bounds for multi-asset options in a setting that combines dependence uncertainty with additional information on the dependence structure. More specifically,...

Market making plays a crucial role in providing liquidity and maintaining stability in financial markets, making it an essential component of well-functioning capital markets. Despite its importance...

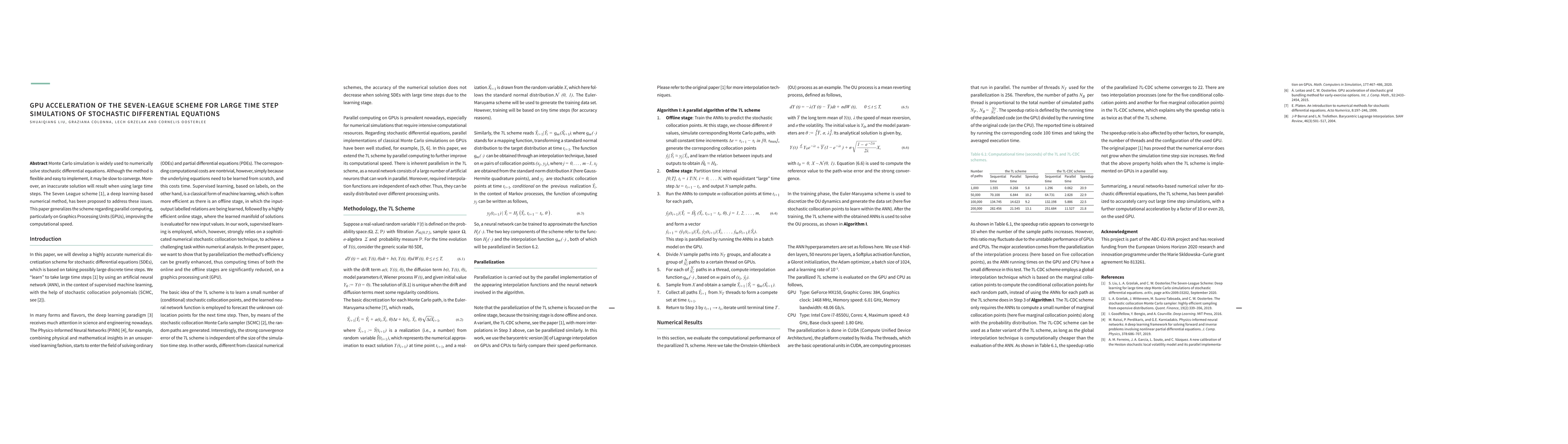

Monte Carlo simulation is widely used to numerically solve stochastic differential equations. Although the method is flexible and easy to implement, it may be slow to converge. Moreover, an inaccura...

In this paper, we will evaluate integrals that define the conditional expectation, variance and characteristic function of stochastic processes with respect to fractional Brownian motion (fBm) for a...

Generative adversarial networks (GANs) have shown promising results when applied on partial differential equations and financial time series generation. We investigate if GANs can also be used to ap...

Extracting implied information, like volatility and/or dividend, from observed option prices is a challenging task when dealing with American options, because of the computational costs needed to so...

A data-driven approach called CaNN (Calibration Neural Network) is proposed to calibrate financial asset price models using an Artificial Neural Network (ANN). Determining optimal values of the mode...

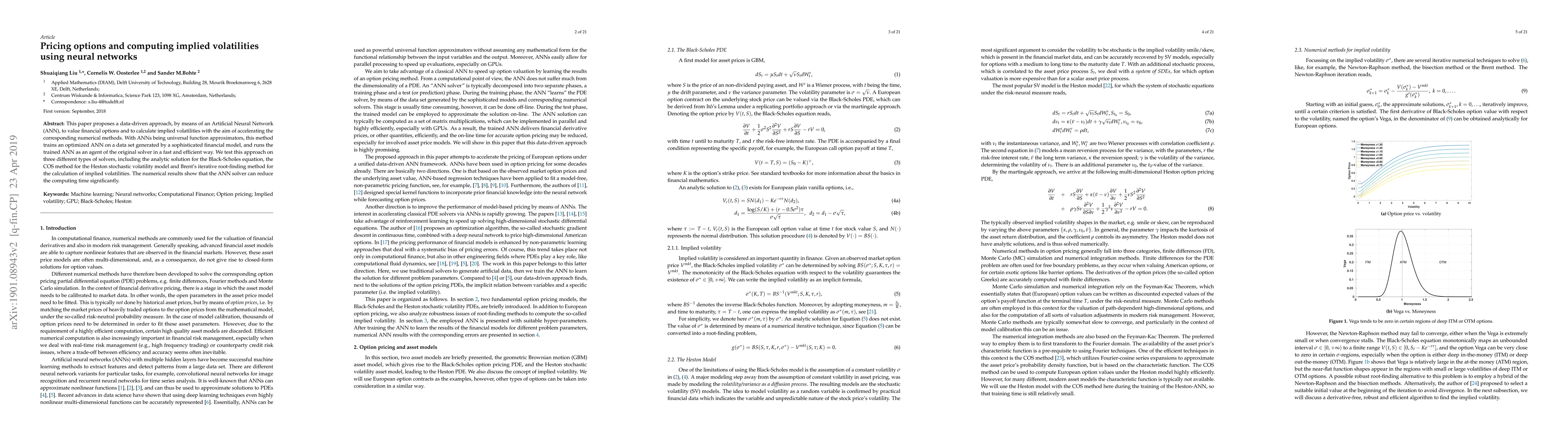

This paper proposes a data-driven approach, by means of an Artificial Neural Network (ANN), to value financial options and to calculate implied volatilities with the aim of accelerating the correspo...

A critical factor in adopting machine learning for time-sensitive financial tasks is computational speed, including model training and inference. This paper demonstrates that a broad class of such pro...

This paper presents a deep generative modeling framework for controllably synthesizing implied volatility surfaces (IVSs) using a variational autoencoder (VAE). Unlike conventional data-driven models,...