Academic Profile

Statistics

Similar Authors

Papers on arXiv

The integration and innovation of finance and technology have gradually transformed the financial system into a complex one. Analyses of the causesd of abnormal fluctuations in the financial market ...

In this study, we propose the sublinear expectation structure under finite states space. To describe an interesting "nonlinear randomized" trial, based on a convex closed domain, we introduce a fami...

In this study, we develop a stochastic optimal control approach with reinforcement learning structure to learn the unknown parameters appeared in the drift and diffusion terms of the stochastic diff...

This paper introduces a new recursive stochastic optimal control problem driven by a forward-backward stochastic differential equations (FBSDEs), where the ter?minal time varies according to the con...

The stochastic volatility inspired (SVI) model is widely used to fit the implied variance smile. Presently, most optimizer algorithms for the SVI model have a strong dependence on the input starting...

We characterize optimal consumption policies in a recursive intertemporal utility framework with local substitution. We establish existence and uniqueness and a version of the Kuhn-Tucker theorem ch...

This paper investigates the dynamic programming principle for a general stochastic control problem in which the state processes are described by a forward-backward stochastic differential equation (...

In contrast to the usual procedure of estimating the distribution of a time series and then obtaining the quantile from the distribution, we develop a compensatory model to improve the quantile esti...

In this study, for any given terminal time $T$, we establish an $L^p$ ($P>2$) estimations of fully coupled FBSDEs based on the $L^2$ estimations. Yong [24] proposed that a natural question is whethe...

We reexamine the classical linear regression model when the model is subject to two types of uncertainty: (i) some of covariates are either missing or completely inaccessible, and (ii) the variance ...

In this paper, we attempt to introduce the Bellman principle for a discrete time multi-period mean-variance model. Based on this new take on the Bellman principle, we obtain a dynamic time-consisten...

To investigate a time-consistent optimal strategy for the continuous time mean-variance model, we develop a new method to establish the Bellman principle. Based on this new method, we obtain a time-...

In the continuous time mean-variance model, we want to minimize the variance (risk) of the investment portfolio with a given mean at terminal time. However, the investor can stop the investment plan...

To improve the efficient frontier of the classical mean-variance model in continuous time, we propose a varying terminal time mean-variance model with a constraint on the mean value of the portfolio...

Several well-established benchmark predictors exist for Value-at-Risk (VaR), a major instrument for financial risk management. Hybrid methods combining AR-GARCH filtering with skewed-$t$ residuals a...

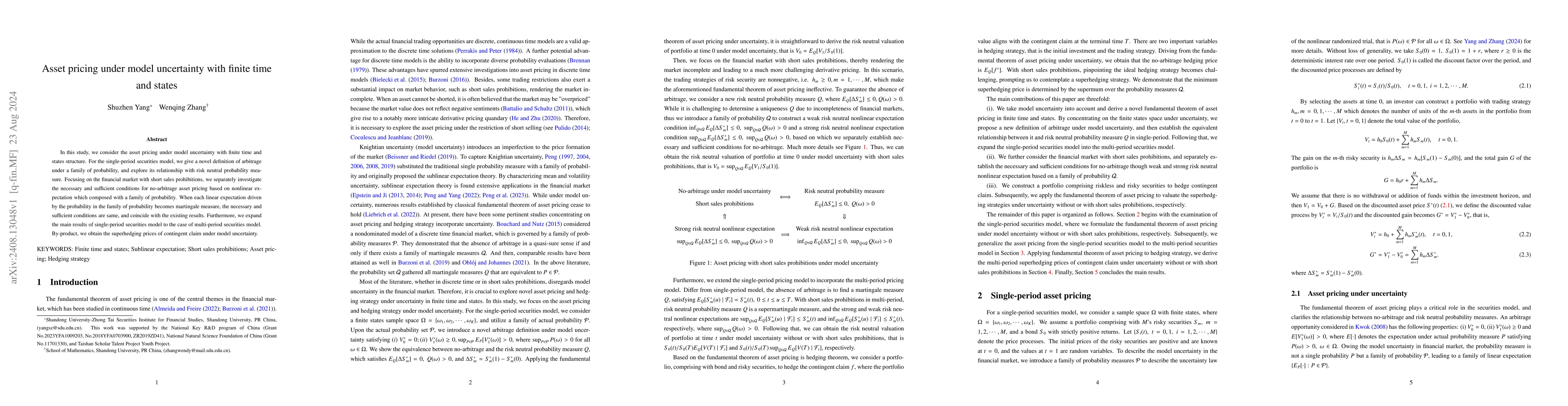

In this study, we consider the asset pricing under model uncertainty with finite time and under a family of probability, and explore its relationship with risk neutral probability meastates structure....

In this paper, we consider a varying terminal time structure for the stochastic optimal control problem under state constraints, in which the terminal time varies with the mean value of the state. In ...

P-hacking poses challenges to traditional hypothesis testing. In this paper, we propose a robust method for the one-sample significance test that can protect against p-hacking from sample manipulation...

In this paper, we propose a unified stochastic optimal control framework that bridges time-optimal control problems and classical stochastic optimal control problems. Unlike traditional deterministic ...

This work introduces a novel theoretical framework grounded in Random Matrix Theory (RMT) for analyzing Transformer training dynamics. We focus on the underlying mechanisms that drive performance impr...

In this paper, we introduce a new type of backward stochastic differential equations (BSDEs) with infinite anticipation, where the generator depends on the entire future values of the solution in infi...

Uncertainty is ubiquitous in real-world data, and the assumptions underlying classical linear regression models are often violated in practice. Inspired by the theory of sublinear expectation, we cons...

In this paper, we investigate a portfolio investment problem under volatility uncertainty and short-sale constraints market via sublinear expectation which is used to model volatility uncertainty. We ...