Authors

Summary

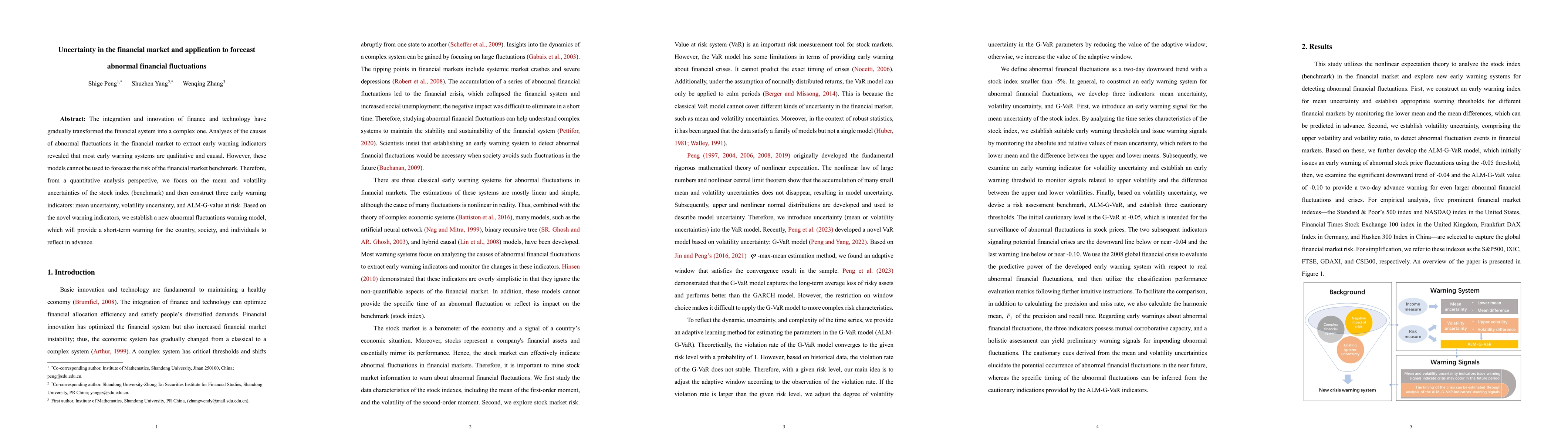

The integration and innovation of finance and technology have gradually transformed the financial system into a complex one. Analyses of the causesd of abnormal fluctuations in the financial market to extract early warning indicators revealed that most early warning systems are qualitative and causal. However, these models cannot be used to forecast the risk of the financial market benchmark. Therefore, from a quantitative analysis perspective, we focus on the mean and volatility uncertainties of the stock index (benchmark) and then construct three early warning indicators: mean uncertainty, volatility uncertainty, and ALM-G-value at risk. Based on the novel warning indicators, we establish a new abnormal fluctuations warning model, which will provide a short-term warning for the country, society, and individuals to reflect in advance.

AI Key Findings

Generated Sep 03, 2025

Methodology

The research methodology involves analyzing the time series of stock indexes using nonlinear expectation theory. It constructs three early warning indicators: mean uncertainty, volatility uncertainty, and ALM-G-VaR value at risk, to forecast abnormal financial fluctuations.

Key Results

- Three early warning indicators (mean uncertainty, volatility uncertainty, and ALM-G-VaR) were developed for forecasting abnormal financial fluctuations.

- ALM-G-VaR model outperformed classical VaR models in capturing uncertainty in financial markets and predicting crisis timing.

- The ALM-G-VaR model accurately forecasted financial crises two days in advance for the S&P500, IXIC, FTSE, GDAXI, and CSI300 indexes.

- The comprehensive analysis of mean uncertainty, volatility uncertainty, and ALM-G-VaR warning indicators provided reliable and accurate early warning signals for financial crises.

Significance

This research is significant as it addresses the limitations of existing early warning systems for financial crises by focusing on quantitative analysis of mean and volatility uncertainties, and proposes a new ALM-G-VaR model that provides more accurate and timely warnings.

Technical Contribution

The paper introduces an adaptive learning method (ALM-G-VaR) to automatically adjust window length in the G-VaR model, overcoming restrictions on window length selection and improving the accuracy of financial crisis warnings.

Novelty

This work distinguishes itself by focusing on quantitative analysis of mean and volatility uncertainties, proposing a novel ALM-G-VaR model for financial crisis forecasting, and demonstrating its superior performance compared to classical VaR models.

Limitations

- The warning signals sometimes exhibit a lag, making it challenging to pinpoint the exact beginning of a crisis.

- The accuracy of crisis alerts still contains false signals, with numerous erroneous indicators present in the warnings.

- The selection of window length and establishment of warning lines remain subjective and vary across different financial markets.

Future Work

- Developing a precise and accurate warning model to minimize false signals and improve crisis timing.

- Investigating the incorporation of nonlinear expectations with the Expected Shortfall (ES) model for enhanced risk measurement.

- Exploring the application of the proposed ALM-G-VaR model to other financial markets and crises.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersThe Financial Market of Environmental Indices

Frank J. Fabozzi, Abootaleb Shirvani, Svetlozar Rachev et al.

No citations found for this paper.

Comments (0)