Academic Profile

Statistics

Similar Authors

Papers on arXiv

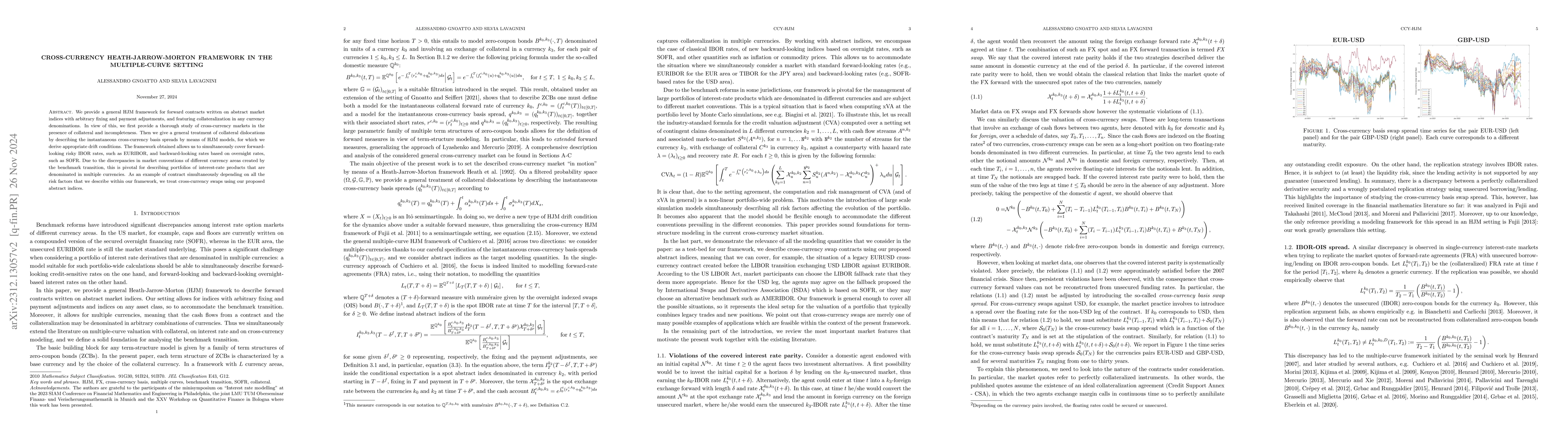

We provide a general HJM framework for forward contracts written on abstract market indices with arbitrary fixing and payment adjustments. We allow for indices on any asset class, featuring collater...

We present a novel computational approach for quadratic hedging in a high-dimensional incomplete market. This covers both mean-variance hedging and local risk minimization. In the first case, the so...

We derive a series expansion by Hermite polynomials for the price of an arithmetic Asian option. This series requires the computation of moments and correlators of the underlying price process, but ...

We price European-style options written on forward contracts in a commodity market, which we model with an infinite-dimensional Heath-Jarrow-Morton (HJM) approach. For this purpose we introduce a ne...

In the setting of polynomial jump-diffusion dynamics, we provide an explicit formula for computing correlators, namely, cross-moments of the process at different time points along its path. The form...

We present a dynamic model for forward curves within the Heath-Jarrow-Morton framework under the Musiela parametrization. The forward curves take values in a function space H, and their dynamics follo...