Academic Profile

Statistics

Similar Authors

Papers on arXiv

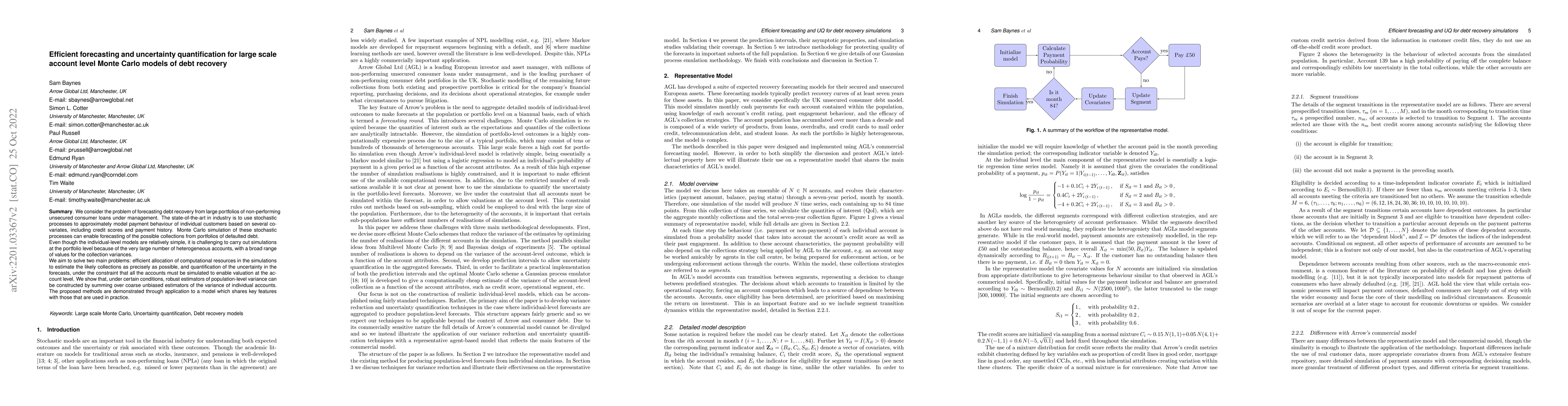

We consider the problem of forecasting debt recovery from large portfolios of non-performing unsecured consumer loans under management. The state of the art in industry is to use stochastic processe...

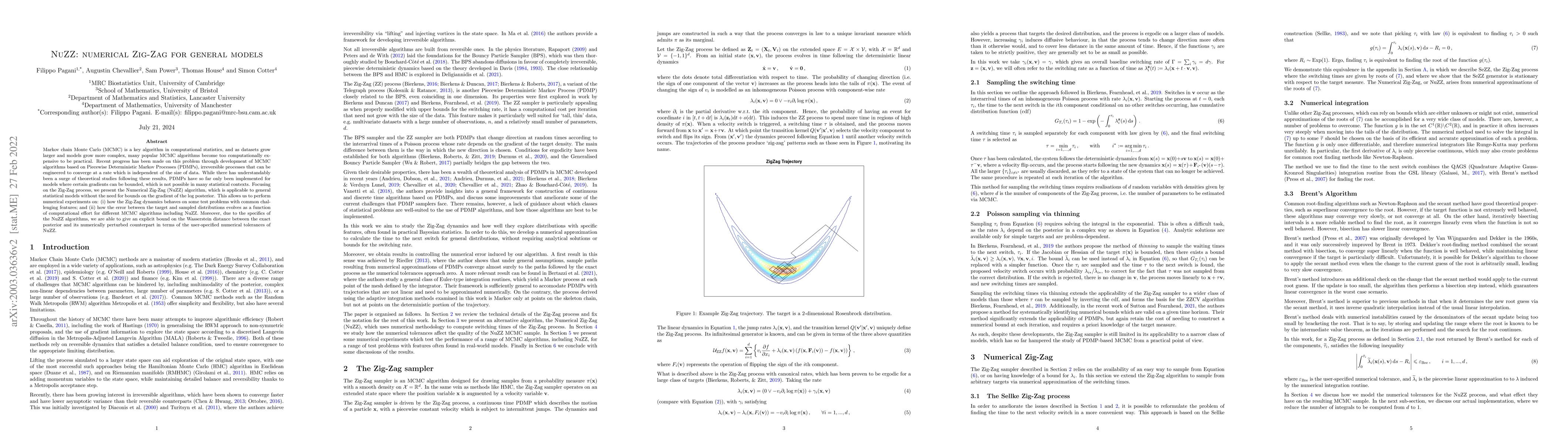

Markov chain Monte Carlo (MCMC) is a key algorithm in computational statistics, and as datasets grow larger and models grow more complex, many popular MCMC algorithms become too computationally expe...

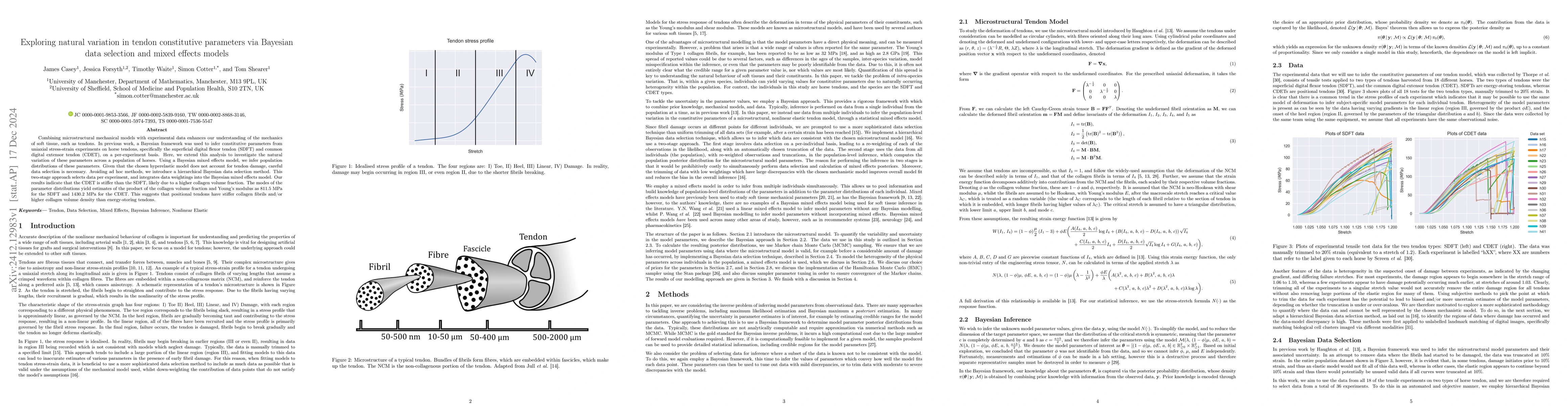

Combining microstructural mechanical models with experimental data enhances our understanding of the mechanics of soft tissue, such as tendons. In previous work, a Bayesian framework was used to infer...

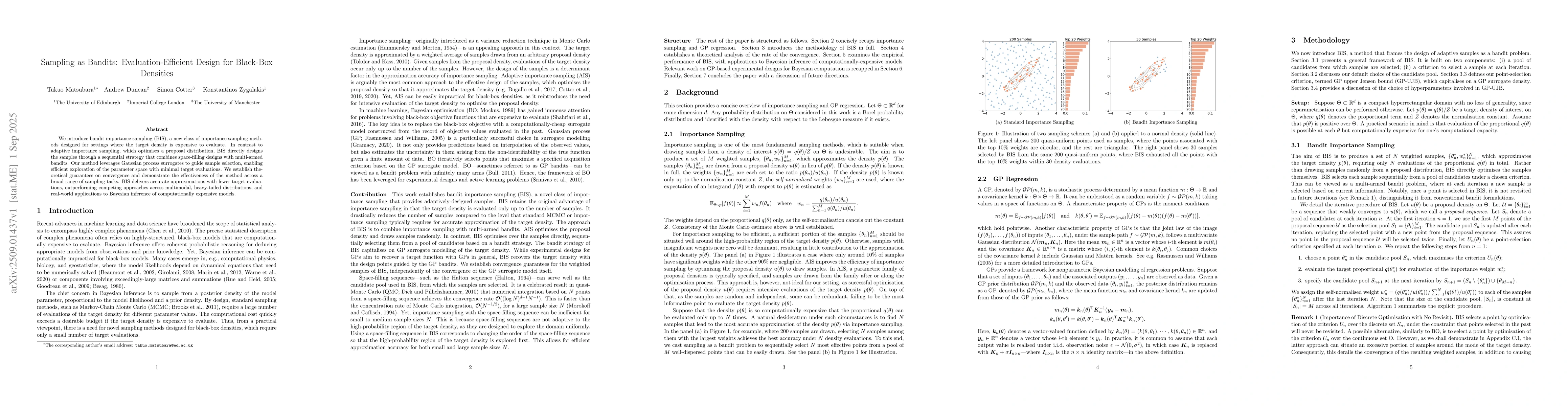

We introduce bandit importance sampling (BIS), a new class of importance sampling methods designed for settings where the target density is expensive to evaluate. In contrast to adaptive importance sa...