Academic Profile

Statistics

Similar Authors

Papers on arXiv

We take into consideration generalization bounds for the problem of the estimation of the drift component for ergodic stochastic differential equations, when the estimator is a ReLU neural network and...

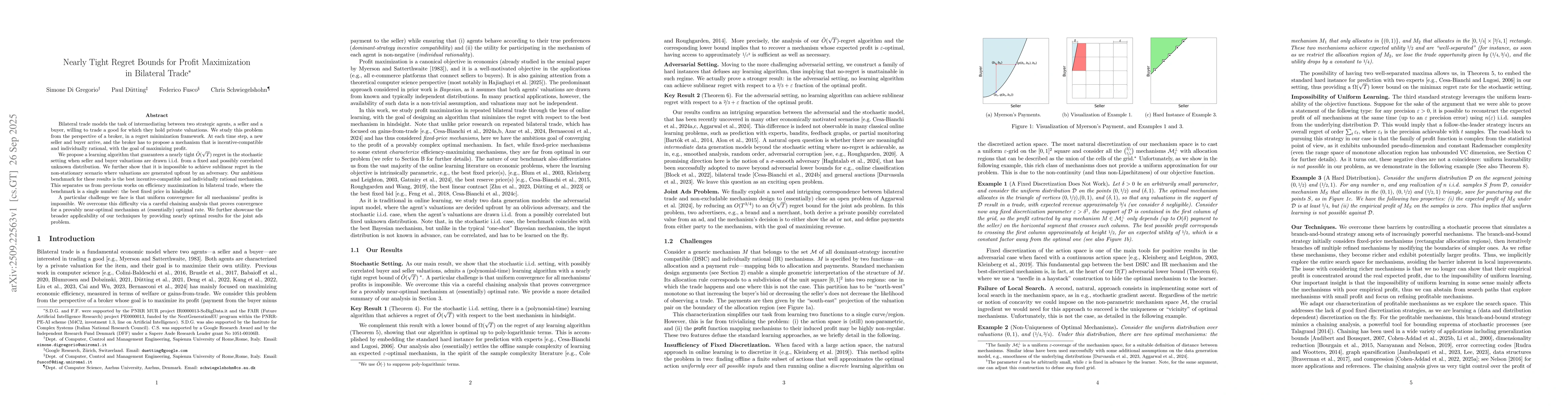

Bilateral trade models the task of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuations. We study this problem from the per...

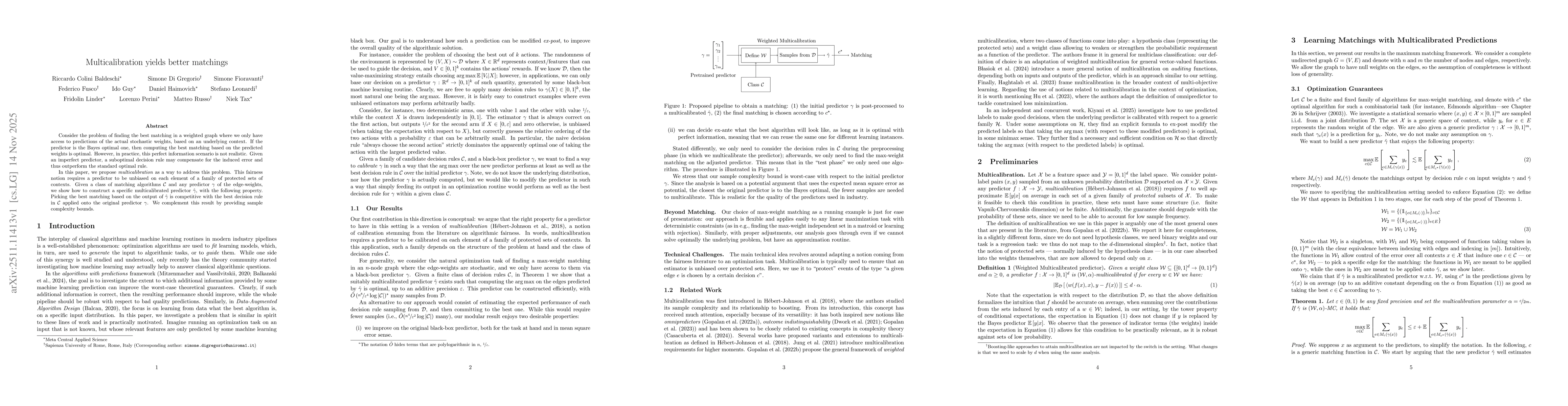

Consider the problem of finding the best matching in a weighted graph where we only have access to predictions of the actual stochastic weights, based on an underlying context. If the predictor is the...

Bilateral trade models the task of intermediating between two strategic agents, a seller and a buyer, who wish to trade a good. We study this problem from the perspective of a profit-maximizing broker...

Bilateral trade models one of the most fundamental economic interactions: the intermediation between two strategic agents, a seller and a buyer, willing to trade a good. We consider the learning versi...

We study Online Convex Optimization (OCO) over a convex set $K\subseteq \mathbb R^d$, where in each round $t$ the learner selects $x_t\in K$ and then observes a convex loss $f_t:K\to[0,1]$, with the g...