Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we consider a generic interest rate market in the presence of roll-over risk, which generates spreads in spot/forward term rates. We do not require classical absence of arbitrage and ...

We introduce a new mean-field game framework to analyze the impact of carbon pricing in a multi-sector economy with defaultable firms. Each sector produces a homogeneous good, with its price endogenou...

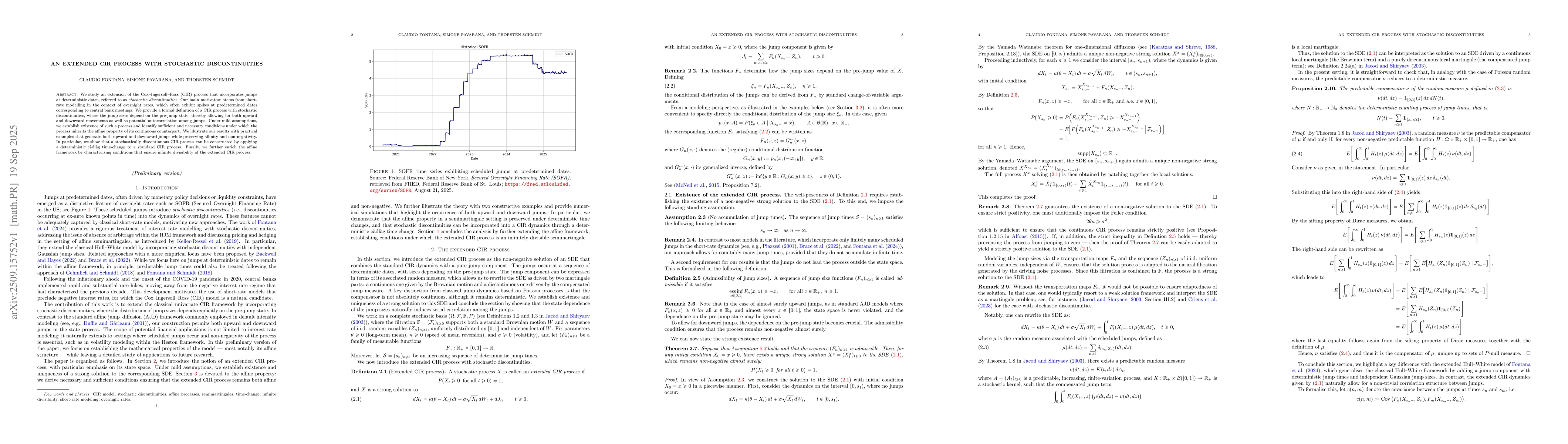

We study an extension of the Cox-Ingersoll-Ross (CIR) process that incorporates jumps at deterministic dates, referred to as stochastic discontinuities. Our main motivation stems from short-rate model...