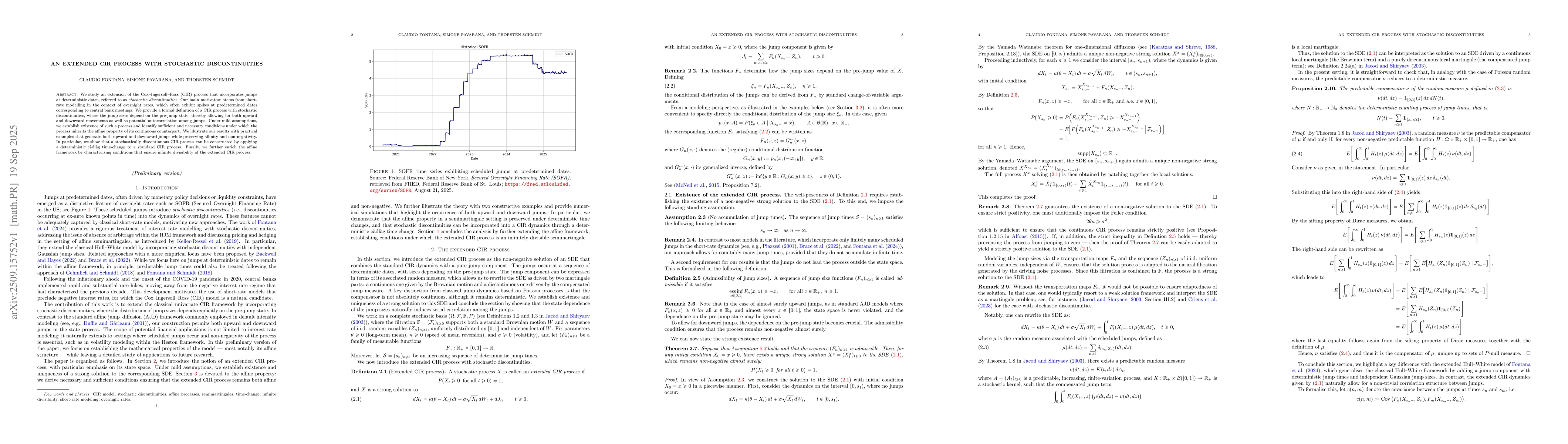

We study an extension of the Cox-Ingersoll-Ross (CIR) process that

incorporates jumps at deterministic dates, referred to as stochastic

discontinuities. Our main motivation stems from short-rate modelling in the

context of overnight rates, which often exhibit jumps at predetermined dates

corresponding to central bank meetings. We provide a formal definition of a CIR

process with stochastic discontinuities, where the jump sizes depend on the

pre-jump state, thereby allowing for both upwarrd and downward movements as

well as potential autocorrelation among jumps. Under mild assumptions, we

establish existence of such a process and identify sufficient and necessary

conditions under which the process inherits the affine property of its

continuous counterpart. We illustrate our results with practical examples that

generate both upward and downward jumps while preserving the affine property

and non-negativity. In particular, we show that a stochastically discontinuous

CIR process can be constructed by applying a determinisitic cadlag time-change

of a classical CIR process. Finally, we further enrich the affine framework by

characterizing conditions that ensure infinite divisibility of the extended CIR

process.

Discussion 0