Academic Profile

Statistics

Similar Authors

Papers on arXiv

Fairness in decision-making processes is often quantified using probabilistic metrics. However, these metrics may not fully capture the real-world consequences of unfairness. In this article, we adopt...

The assessment of risk based on historical data faces many challenges, in particular due to the limited amount of available data, lack of stationarity, and heavy tails. While estimation on a short-t...

In most cases, insurance contracts are linked to the financial markets, such as through interest rates or equity-linked insurance products. To motivate an evaluation rule in these hybrid markets, Ar...

In this work we consider one-dimensional generalized affine processes under the paradigm of Knightian uncertainty (so-called non-linear generalized affine models). This extends and generalizes previ...

Estimating value-at-risk on time series data with possibly heteroscedastic dynamics is a highly challenging task. Typically, we face a small data problem in combination with a high degree of non-lin...

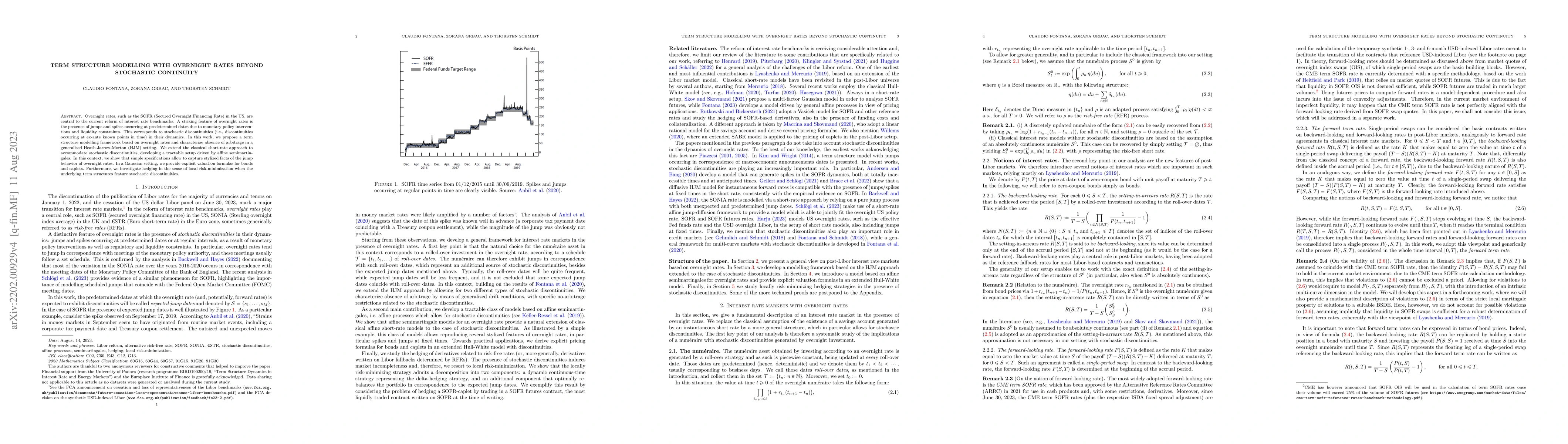

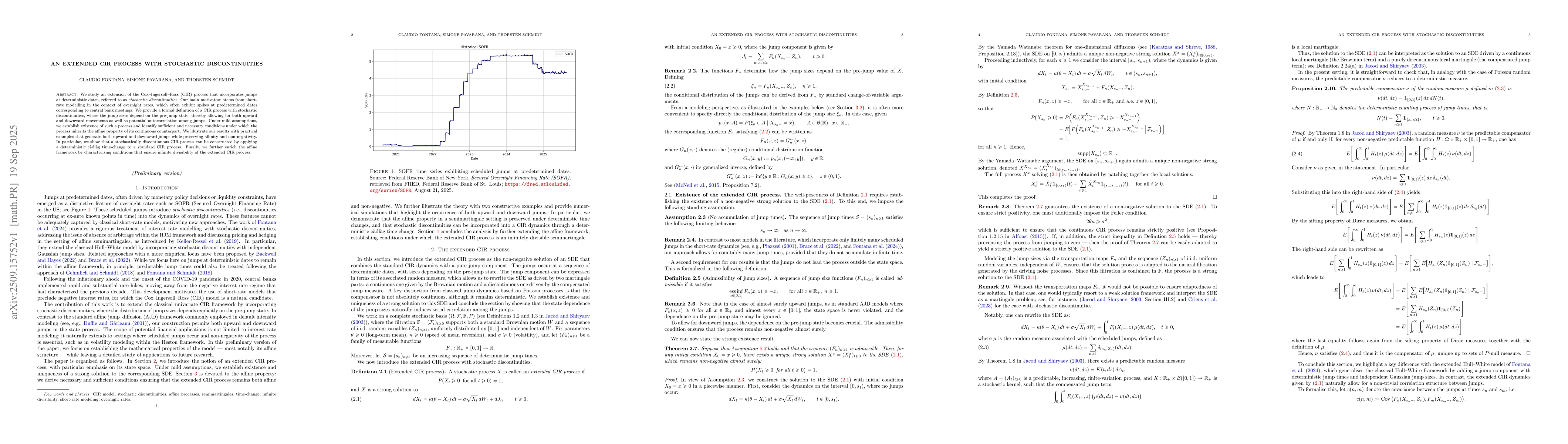

Overnight rates, such as the SOFR (Secured Overnight Financing Rate) in the US, are central to the current reform of interest rate benchmarks. A striking feature of overnight rates is the presence o...

While the estimation of risk is an important question in the daily business of banking and insurance, many existing plug-in estimation procedures suffer from an unnecessary bias. This often leads to...

We use the abstract method of (local) martingale problems in order to give criteria for convergence of stochastic processes. Extending previous notions, the formulation we use is neither restricted ...

We study pricing and hedging under parameter uncertainty for a class of Markov processes which we call generalized affine processes and which includes the Black-Scholes model as well as the constant...

We consider a market with a term structure of credit risky bonds in the single-name case. We aim at minimal assumptions extending existing results in this direction: first, the random field of forwa...

We consider a financial market in discrete time and study pricing and hedging conditional on the information available up to an arbitrary point in time. In this conditional framework, we determine t...

We study a Sparre Andersen model in which the business activity of the company is described by a compound renewal process with drift assuming that the capital reserves are invested in a risky asset....

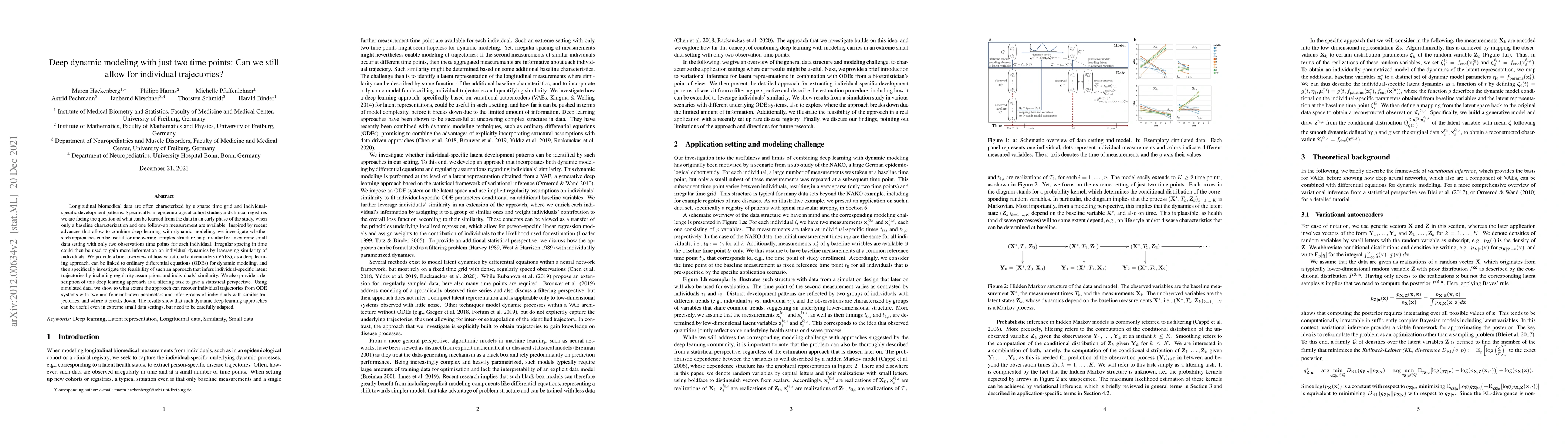

Longitudinal biomedical data are often characterized by a sparse time grid and individual-specific development patterns. Specifically, in epidemiological cohort studies and clinical registries we ar...

Most insurance contracts are inherently linked to financial markets, be it via interest rates, or -- as hybrid products like equity-linked life insurance and variable annuities -- directly to stocks...

The goal of this article is to investigate infinite dimensional affine diffusion processes on the canonical state space. This includes a derivation of the corresponding system of Riccati differentia...

Generalized statistical arbitrage concepts are introduced corresponding to trading strategies which yield positive gains on average in a class of scenarios rather than almost surely. The relevant sc...

This paper proposes a market consistent valuation framework for variable annuities with guaranteed minimum accumulation benefit, death benefit and surrender benefit features. The setup is based on a...

In this paper we develop a novel methodology for estimation of risk capital allocation. The methodology is rooted in the theory of risk measures. We work within a general, but tractable class of law...

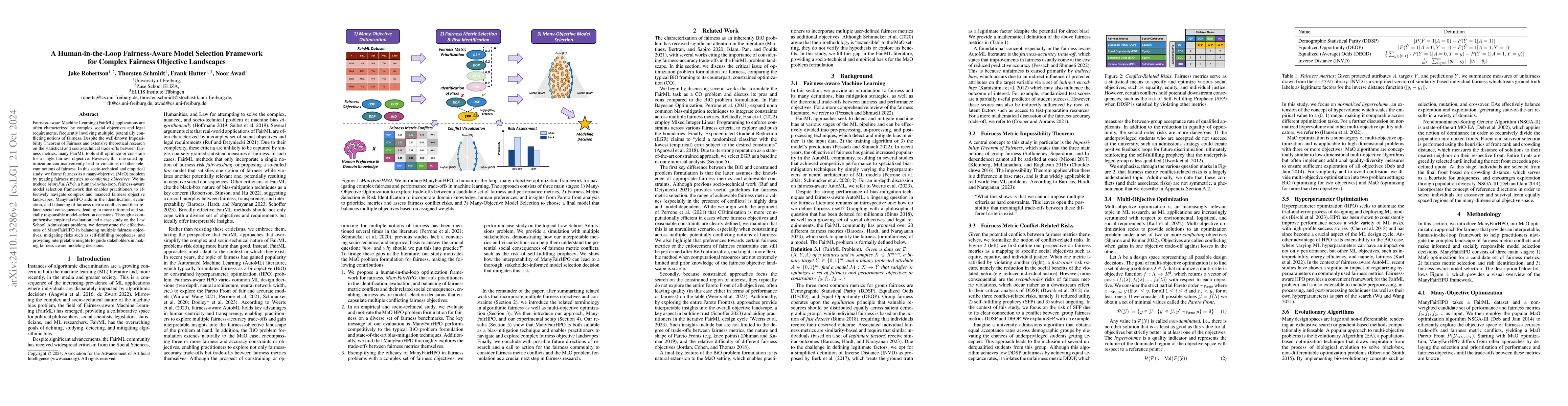

Fairness-aware Machine Learning (FairML) applications are often characterized by complex social objectives and legal requirements, frequently involving multiple, potentially conflicting notions of fai...

Neural Jump ODEs model the conditional expectation between observations by neural ODEs and jump at arrival of new observations. They have demonstrated effectiveness for fully data-driven online foreca...

While the {estimation} of risk is an important question in the daily business of banking and insurance, many existing plug-in estimation procedures suffer from an unnecessary bias. This often leads to...

We establish a quantitative version of the classical Halmos-Savage theorem for convex sets of probability measures and its dual counterpart, generalizing previous quantitative versions. These results ...

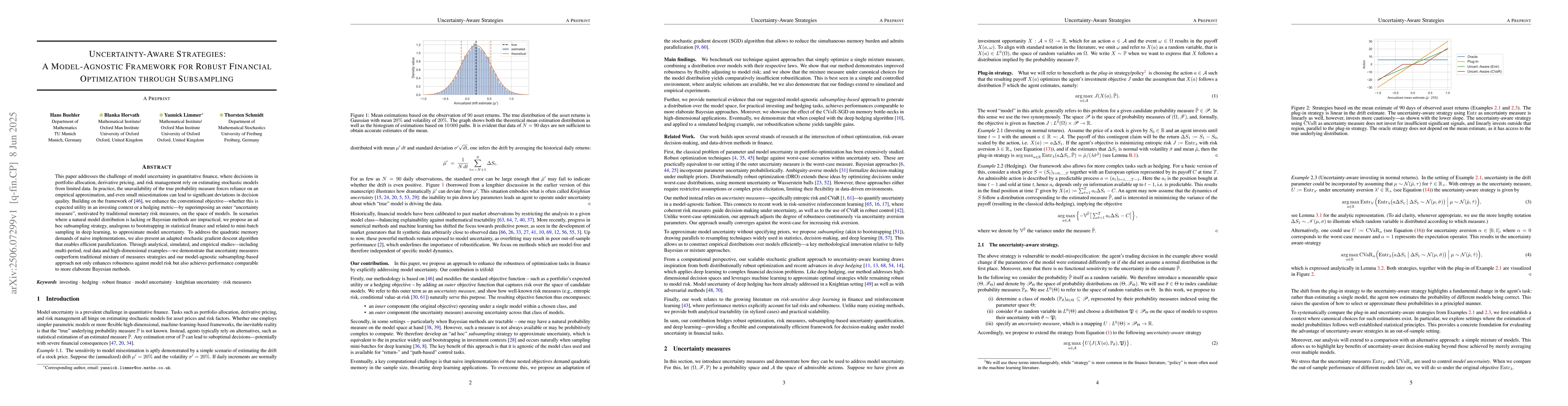

This paper addresses the challenge of model uncertainty in quantitative finance, where decisions in portfolio allocation, derivative pricing, and risk management rely on estimating stochastic models f...

In this paper we study the pricing and hedging of nonreplicable contingent claims, such as long-term insurance contracts like variable annuities. Our approach is based on the benchmark-neutral pricing...

We introduce a new mean-field game framework to analyze the impact of carbon pricing in a multi-sector economy with defaultable firms. Each sector produces a homogeneous good, with its price endogenou...

We study an extension of the Cox-Ingersoll-Ross (CIR) process that incorporates jumps at deterministic dates, referred to as stochastic discontinuities. Our main motivation stems from short-rate model...

To make medium- and long-term insurance products attractive, it is essential to enable participation in stock market returns. However, to eliminate downside risk, guarantees must be included, which na...

Many rare diseases offer limited established treatment options, leading patients to switch therapies when new medications emerge. To analyze the impact of such treatment switches within the low sample...

Filtering problems with jumps in both the signal and the observation have been extensively studied, typically under the assumption that jump times are totally inaccessible. In many applications, howev...

We extend the classical theory of affine processes to a path-dependent setting by introducing path-dependent coefficients and provide analytic formulas for their Fourier--Laplace transform in terms of...