Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the problems of consistency and of the existence of finite-dimensional realizations for multi-curve interest rate models of Heath-Jarrow-Morton type, generalizing the geometric approach dev...

In this work, we study statistical arbitrage strategies in international crude oil futures markets. We analyse strategies that extend classical pairs trading strategies, considering the two benchmar...

In this paper, we consider a generic interest rate market in the presence of roll-over risk, which generates spreads in spot/forward term rates. We do not require classical absence of arbitrage and ...

Variable annuities with Guaranteed Minimum Withdrawal Benefits (GMWB) entitle the policy holder to periodic withdrawals together with a terminal payoff linked to the performance of an equity fund. I...

Alternative risk-free rates (RFRs) play a central role in the reform of interest rate benchmarks. We study a model for RFRs driven by a general affine process. Under minimal assumptions, we derive e...

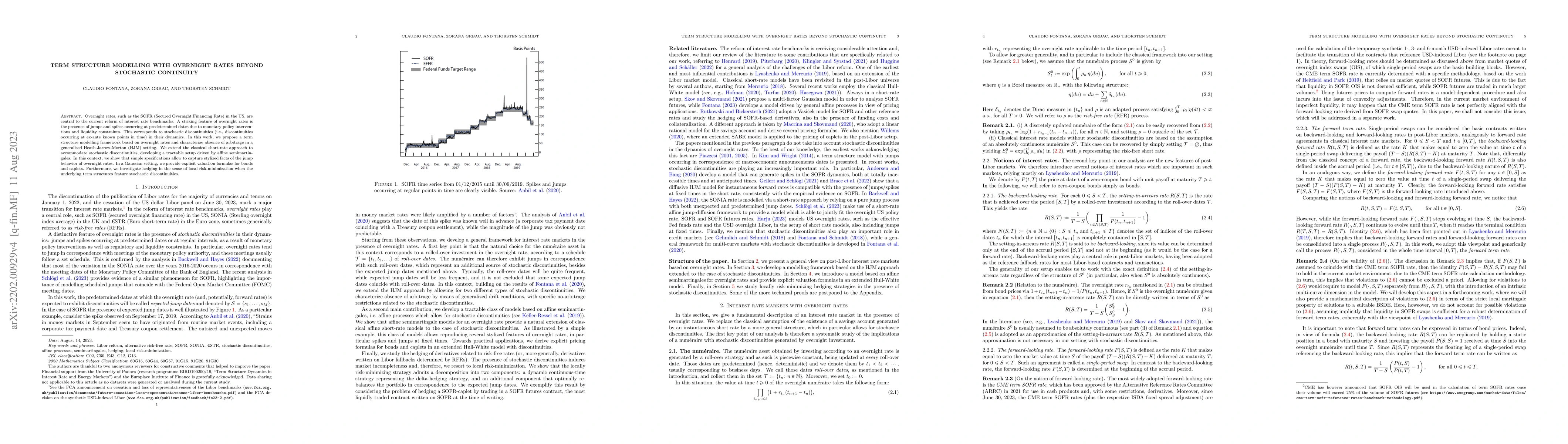

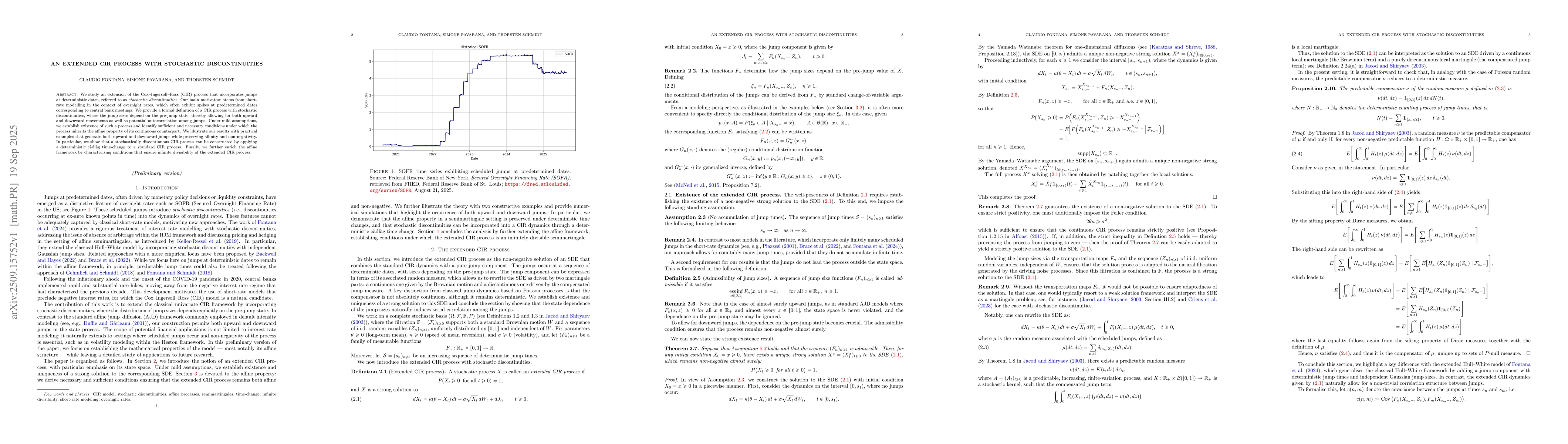

Overnight rates, such as the SOFR (Secured Overnight Financing Rate) in the US, are central to the current reform of interest rate benchmarks. A striking feature of overnight rates is the presence o...

In a discrete-time setting, we study arbitrage concepts in the presence of convex trading constraints. We show that solvability of portfolio optimization problems is equivalent to absence of arbitra...

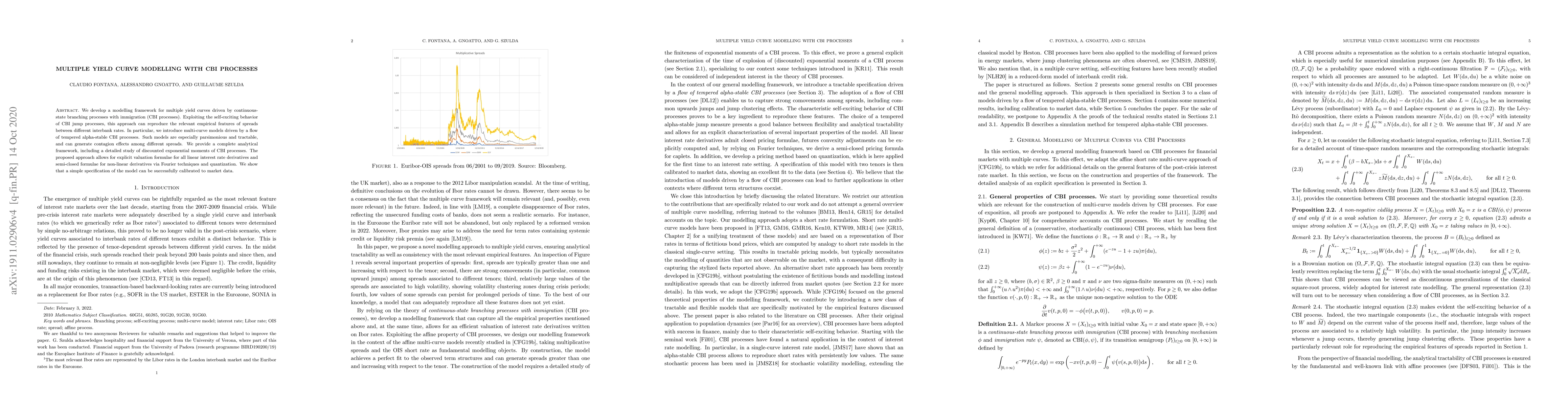

We develop a modelling framework for multiple yield curves driven by continuous-state branching processes with immigration (CBI processes). Exploiting the self-exciting behavior of CBI jump processe...

In the context of a general semimartingale model of a complete market, we aim at answering the following question: How much is an investor willing to pay for learning some inside information that al...

We introduce and study the notion of sure profit via flash strategy, consisting of a high-frequency limit of buy-and-hold trading strategies. In a fully general setting, without imposing any semimar...

We develop a unifying framework for modeling multiple term structures arising in financial, insurance, and energy markets. We adopt the Heath-Jarrow-Morton approach under the real-world probability an...

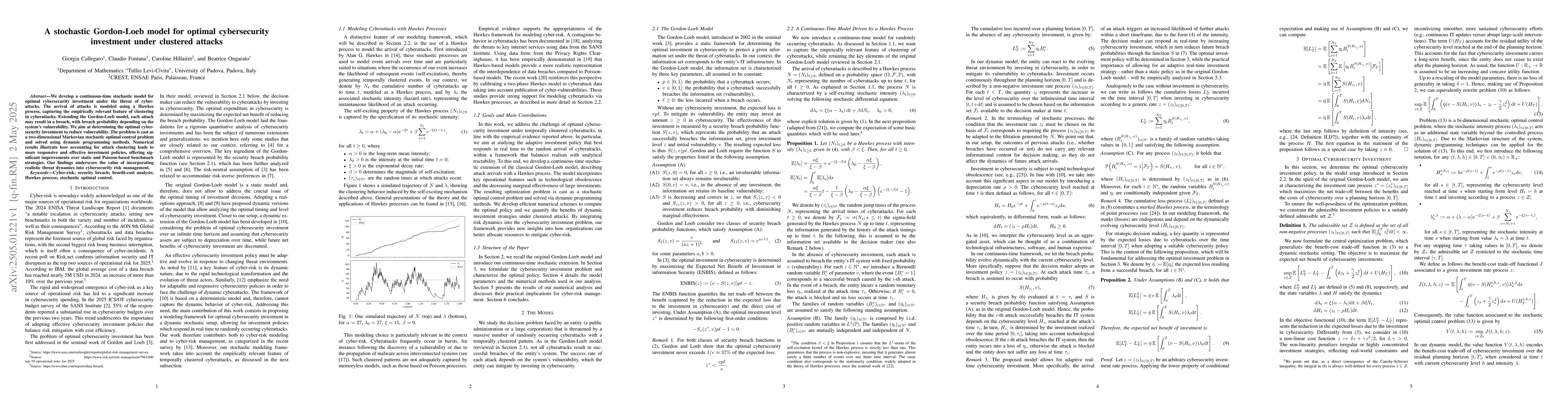

We develop a continuous-time stochastic model for optimal cybersecurity investment under the threat of cyberattacks. The arrival of attacks is modeled using a Hawkes process, capturing the empirically...

We investigate how asymmetric information affects the equilibrium dynamics in a setting where a large number of players interacts. Motivated by the analysis of the mechanism of equilibrium price forma...

We study an extension of the Cox-Ingersoll-Ross (CIR) process that incorporates jumps at deterministic dates, referred to as stochastic discontinuities. Our main motivation stems from short-rate model...