Academic Profile

Statistics

Similar Authors

Papers on arXiv

In optimal stopping problems, a Markov structure guarantees Markovian optimal stopping times (first exit times). Surprisingly, there is no analogous result for Markovian stopping games once randomiz...

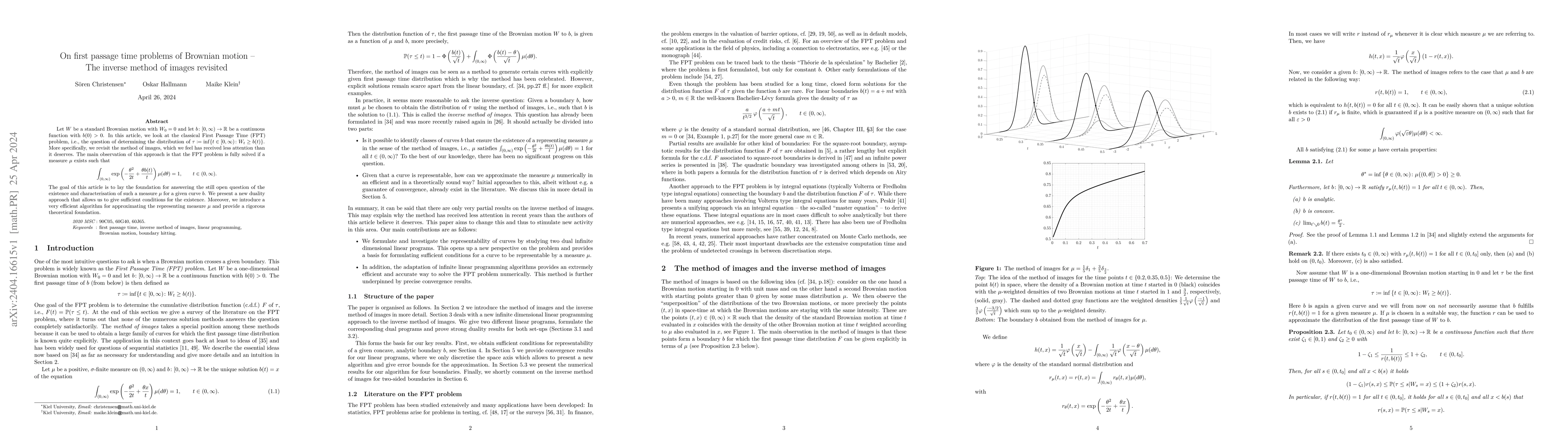

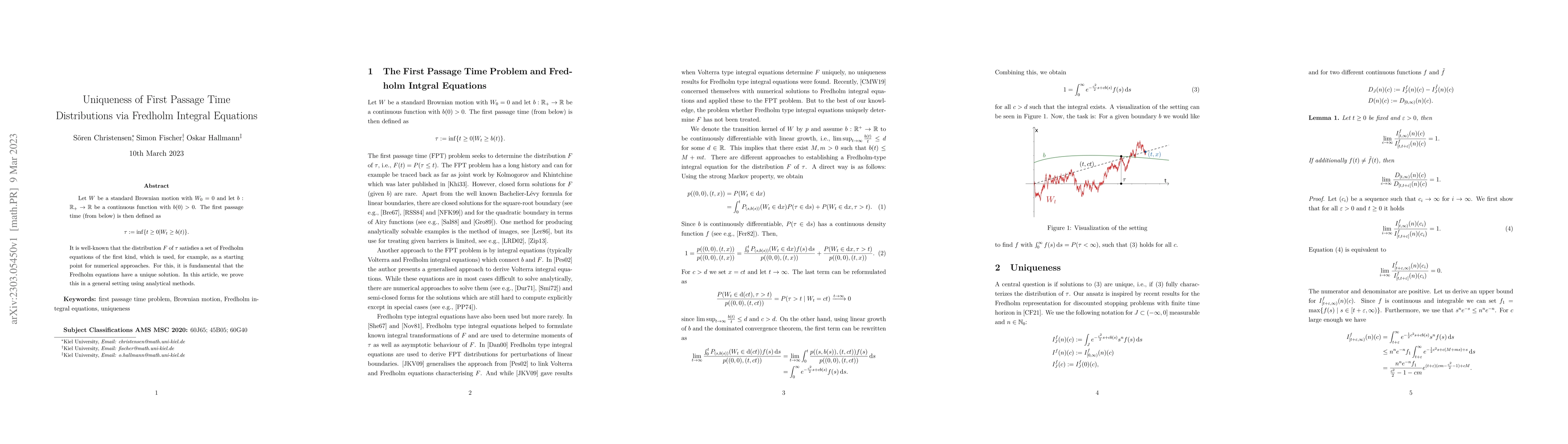

Let $W$ be a standard Brownian motion with $W_0 = 0$ and let $b\colon[0,\infty) \to \mathbb{R}$ be a continuous function with $b(0) > 0$. In this article, we look at the classical First Passage Time...

The standard theory of optimal stopping is based on the idealised assumption that the underlying process is essentially known. In this paper, we drop this restriction and study data-driven optimal s...

Over the recent past data-driven algorithms for solving stochastic optimal control problems in face of model uncertainty have become an increasingly active area of research. However, for singular co...

We study the (weak) equilibrium problem arising from the problem of optimally stopping a one-dimensional diffusion subject to an expectation constraint on the time until stopping. The weak equilibri...

In recent years, there has been an intense debate about how learning in biological neural networks (BNNs) differs from learning in artificial neural networks. It is often argued that the updating of...

We study a general formulation of the classical two-player Dynkin game in a Markovian discrete time setting. We show that an appropriate class of mixed, i.e., randomized, strategies in this context ...

In a probabilistic mean-field game driven by a linear diffusion an individual player aims to minimize an ergodic long-run cost by controlling the diffusion through a pair of -- increasing and decrea...

Let $W$ be a standard Brownian motion with $W_0 = 0$ and let $b: \mathbb{R}_+ \to \mathbb{R}$ be a continuous function with $b(0) > 0$. The first passage time (from below) is then defined as \begin{...

We consider the game-theoretic approach to time-inconsistent stopping of a one-dimensional diffusion where the time-inconsistency is due to the presence of a non-exponential (weighted) discount func...

In this paper, we propose an extension of the forward improvement iteration algorithm, originally introduced in Irle (2006) and recently reconsidered in Miclo and Villeneuve (2021). The main new ing...

For classical finite time horizon stopping problems driven by a Brownian motion \[V(t,x) = \sup_{t\leq\tau\leq0}E_{(t,x)}[g(\tau,W_{\tau})],\] we derive a new class of Fredholm type integral equat...

Stochastic optimal control problems have a long tradition in applied probability, with the questions addressed being of high relevance in a multitude of fields. Even though theoretical solutions are...

We call a given American option representable if there exists a European claim which dominates the American payoff at any time and such that the values of the two options coincide in the continuatio...

This article treats both discrete time and continuous time stopping problems for general Markov processes on the real line with general linear costs. Using an auxiliary function of maximum represent...

We consider the discrete time stopping problem \[ V(t,x) = \sup_{\tau}E_{(t,x)}[g(\tau, X_\tau)],\] where $X$ is a random walk. It is well known that the value function $V$ is in general not smooth ...

A moment constraint that limits the number of dividends in the optimal dividend problem is suggested. This leads to a new type of time-inconsistent stochastic impulse control problem. First, the opt...

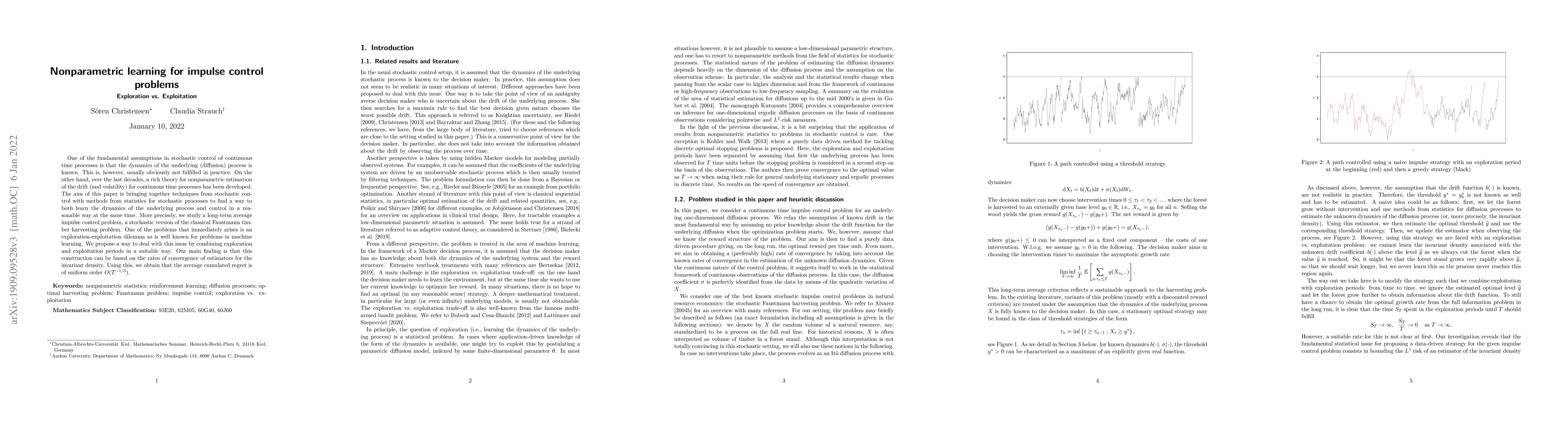

One of the fundamental assumptions in stochastic control of continuous time processes is that the dynamics of the underlying (diffusion) process is known. This is, however, usually obviously not ful...

The Chow-Robbins game is a classical still partly unsolved stopping problem introduced by Chow and Robbins in 1965. You repeatedly toss a fair coin. After each toss, you decide if you take the fract...

We investigate the impact of Knightian uncertainty on the optimal timing policy of an ambiguity averse decision maker in the case where the underlying factor dynamics follow a multidimensional Brown...

We consider the impact of ambiguity on the optimal timing of a class of two-dimensional integral option contracts when the exercise payoff is a positively homogeneous measurable function. Hence, the...

A game-theoretic framework for time-inconsistent stopping problems where the time-inconsistency is due to the consideration of a non-linear function of an expected reward is developed. A class of mi...

This paper considers an ergodic version of the bounded velocity follower problem, assuming that the decision maker lacks knowledge of the underlying system parameters and must learn them while simulta...

One of the most classical games for stochastic processes is the zero-sum Dynkin (stopping) game. We present a complete equilibrium solution to a general formulation of this game with an underlying one...

We introduce a new class of generative diffusion models that, unlike conventional denoising diffusion models, achieve a time-homogeneous structure for both the noising and denoising processes, allowin...

We consider the problem of recovering a latent signal $X$ from its noisy observation $Y$. The unknown law $\mathbb{P}^X$ of $X$, and in particular its support $\mathscr{M}$, are accessible only throug...