Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a new Langevin dynamics based algorithm, called e-TH$\varepsilon$O POULA, to solve optimization problems with discontinuous stochastic gradients which naturally appear in real-world appli...

In this paper, we are concerned with the valuation of Catastrophic Mortality Bonds and, in particular, we examine the case of the Swiss Re Mortality Bond 2003 as a primary example of this class of a...

Recent advances in stochastic optimization have yielded the interactive particle Langevin algorithm (IPLA), which leverages the notion of interacting particle systems (IPS) to efficiently sample fro...

We demonstrate that for strongly log-convex densities whose potentials are discontinuous on manifolds, the ULA algorithm converges with stepsize bias of order $1/2$ in Wasserstein-p distance. Our re...

We provide full theoretical guarantees for the convergence behaviour of diffusion-based generative models under the assumption of strongly log-concave data distributions while our approximating clas...

In this article we propose a novel taming Langevin-based scheme called $\mathbf{sTULA}$ to sample from distributions with superlinearly growing log-gradient which also satisfy a Log-Sobolev inequali...

We develop a class of interacting particle systems for implementing a maximum marginal likelihood estimation (MMLE) procedure to estimate the parameters of a latent variable model. We achieve this b...

In this article we consider sampling from log concave distributions in Hamiltonian setting, without assuming that the objective gradient is globally Lipschitz. We propose two algorithms based on mon...

Existence, uniqueness, and $L_p$-approximation results are presented for scalar stochastic differential equations (SDEs) by considering the case where, the drift coefficient has finitely many spatia...

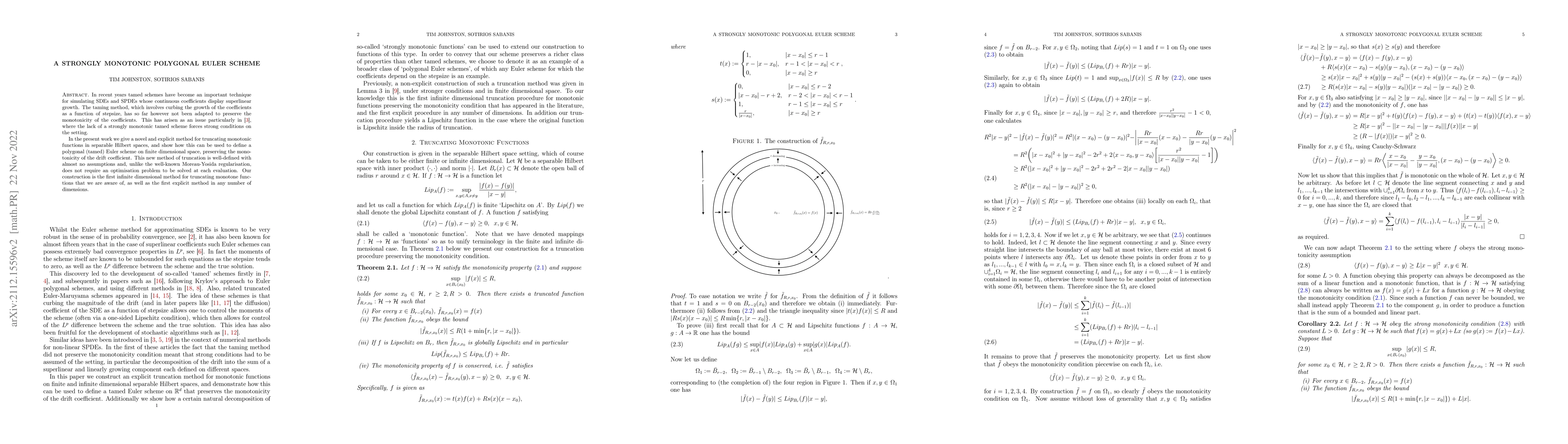

In recent years tamed schemes have become an important technique for simulating SDEs and SPDEs whose continuous coefficients display superlinear growth. The taming method, which involves curbing the...

The recent statistical finite element method (statFEM) provides a coherent statistical framework to synthesise finite element models with observed data. Through embedding uncertainty inside of the g...

We consider non-convex stochastic optimization problems where the objective functions have super-linearly growing and discontinuous stochastic gradients. In such a setting, we provide a non-asymptot...

We present a new class of Langevin based algorithms, which overcomes many of the known shortcomings of popular adaptive optimizers that are currently used for the fine tuning of deep learning models...

A new approach in stochastic optimization via the use of stochastic gradient Langevin dynamics (SGLD) algorithms, which is a variant of stochastic gradient decent (SGD) methods, allows us to efficie...

Artificial neural networks (ANNs) are typically highly nonlinear systems which are finely tuned via the optimization of their associated, non-convex loss functions. In many cases, the gradient of an...

We provide a nonasymptotic analysis of the convergence of the stochastic gradient Hamiltonian Monte Carlo (SGHMC) to a target measure in Wasserstein-2 distance without assuming log-concavity. Our an...

In this paper, we are concerned with a non-asymptotic analysis of sampling algorithms used in nonconvex optimization. In particular, we obtain non-asymptotic estimates in Wasserstein-1 and Wasserste...

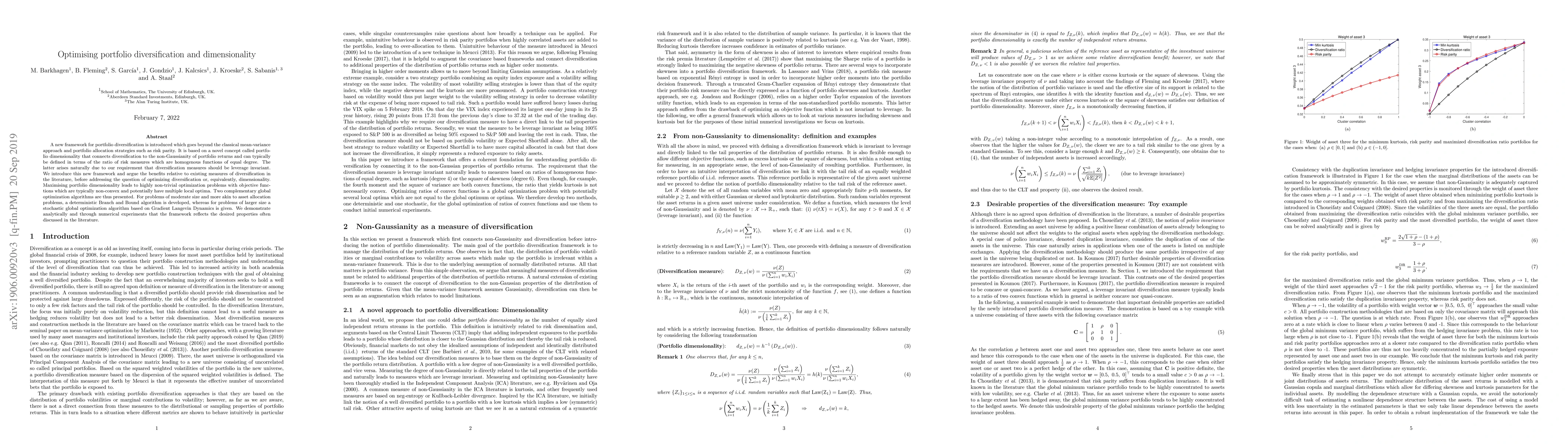

A new framework for portfolio diversification is introduced which goes beyond the classical mean-variance approach and portfolio allocation strategies such as risk parity. It is based on a novel con...

A new (unadjusted) Langevin Monte Carlo (LMC) algorithm with improved rates in total variation and in Wasserstein distance is presented. All these are obtained in the context of sampling from a targ...

In this article we show that for SDEs with a drift coefficient that is non-locally integrable, one may define a tamed Euler scheme that converges in $L^p$ at rate $1/2$ to the true solution. The tamin...

In this article, we study the problem of sampling from distributions whose densities are not necessarily smooth nor log-concave. We propose a simple Langevin-based algorithm that does not rely on popu...

Score-based Generative Models (SGMs) approximate a data distribution by perturbing it with Gaussian noise and subsequently denoising it via a learned reverse diffusion process. These models excel at m...

Motivated by applications in deep learning, where the global Lipschitz continuity condition is often not satisfied, we examine the problem of sampling from distributions with super-linearly growing lo...

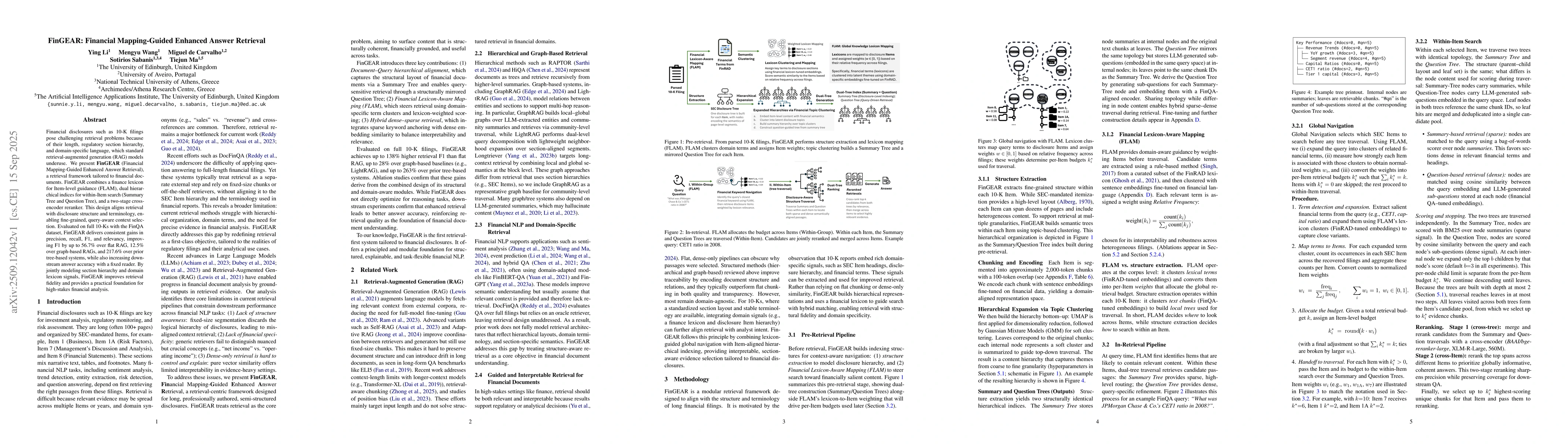

Financial disclosures such as 10-K filings present challenging retrieval problems due to their length, regulatory section hierarchy, and domain-specific language, which standard retrieval-augmented ge...

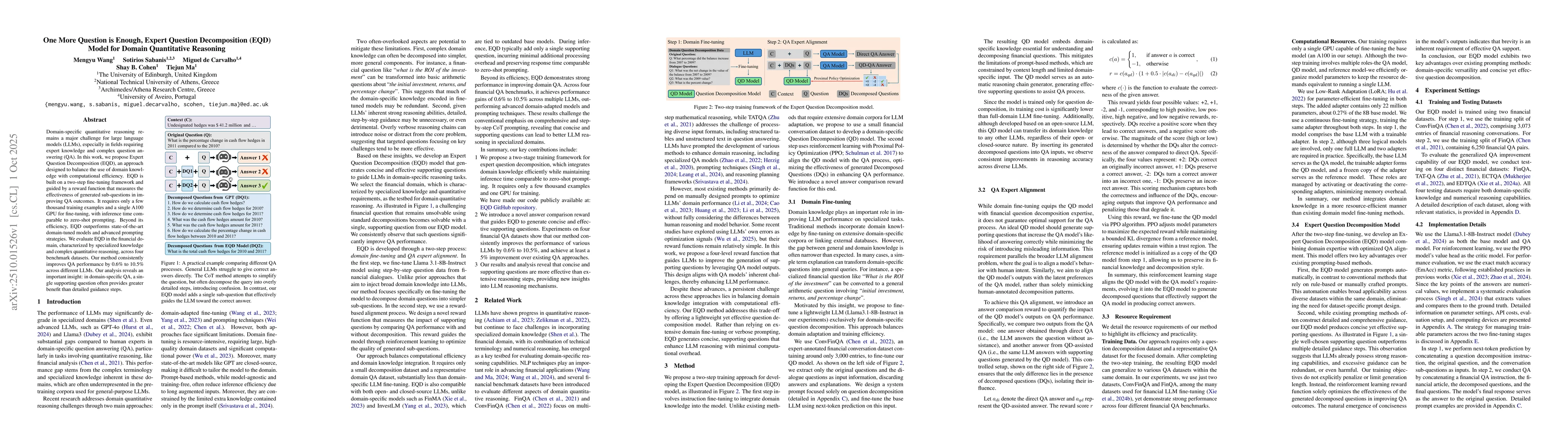

Domain-specific quantitative reasoning remains a major challenge for large language models (LLMs), especially in fields requiring expert knowledge and complex question answering (QA). In this work, we...

Generalization in deep learning is closely tied to the pursuit of flat minima in the loss landscape, yet classical Stochastic Gradient Langevin Dynamics (SGLD) offers no mechanism to bias its dynamics...

Financial decision-makers face more information than they can directly inspect, making context compression necessary. Yet when large language models (LLMs) compress financial source material, they can...