Academic Profile

Statistics

Similar Authors

Papers on arXiv

The Minimum Covariance Determinant (MCD) approach robustly estimates the location and scatter matrix using the subset of given size with lowest sample covariance determinant. Its main drawback is th...

We employ scoring functions, used in statistics for eliciting risk functionals, as cost functions in the Monge-Kantorovich (MK) optimal transport problem. This gives raise to a rich variety of novel...

We study the impact of dependence uncertainty on the expectation of the product of $d$ random variables, $\mathbb{E}(X_1X_2\cdots X_d)$ when $X_i \sim F_i$ for all~$i$. Under some conditions on the ...

Dybvig (1988a,b) solves in a complete market setting the problem of finding a payoff that is cheapest possible in reaching a given target distribution ("cost-efficient payoff"). In the presence of a...

The robustness of risk measures to changes in underlying loss distributions (distributional uncertainty) is of crucial importance in making well-informed decisions. In this paper, we quantify, for t...

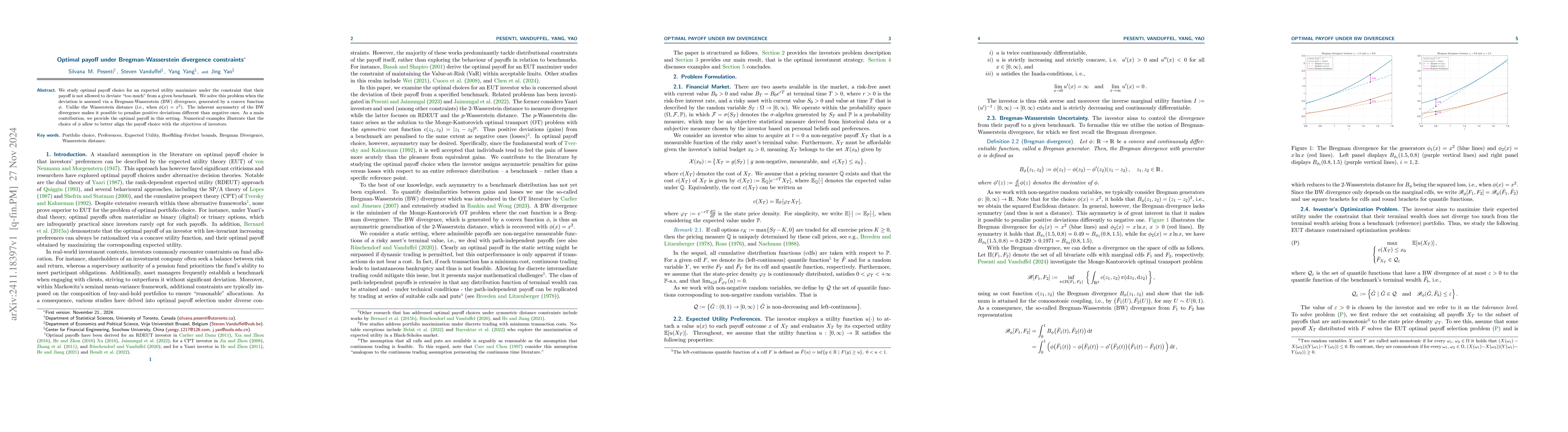

We study optimal payoff choice for an expected utility maximizer under the constraint that their payoff is not allowed to deviate ``too much'' from a given benchmark. We solve this problem when the de...

This paper shows that one needs to be careful when making statements on potential links between correlation and coskewness. Specifically, we first show that, on the one hand, it is possible to observe...

Recent studies have highlighted the significance of higher-order moments - such as coskewness - in portfolio optimization within the financial domain. This paper extends that focus to the field of act...

We establish sharp upper and lower bounds for distortion risk metrics under distributional uncertainty. The uncertainty sets are characterized by four key features of the underlying distribution: mean...

We study risk aggregation problems for arbitrary non-decreasing aggregation functions and tail risk measures under dependence uncertainty in a distributionally robust setting. To this end, we introduc...