Academic Profile

Statistics

Similar Authors

Papers on arXiv

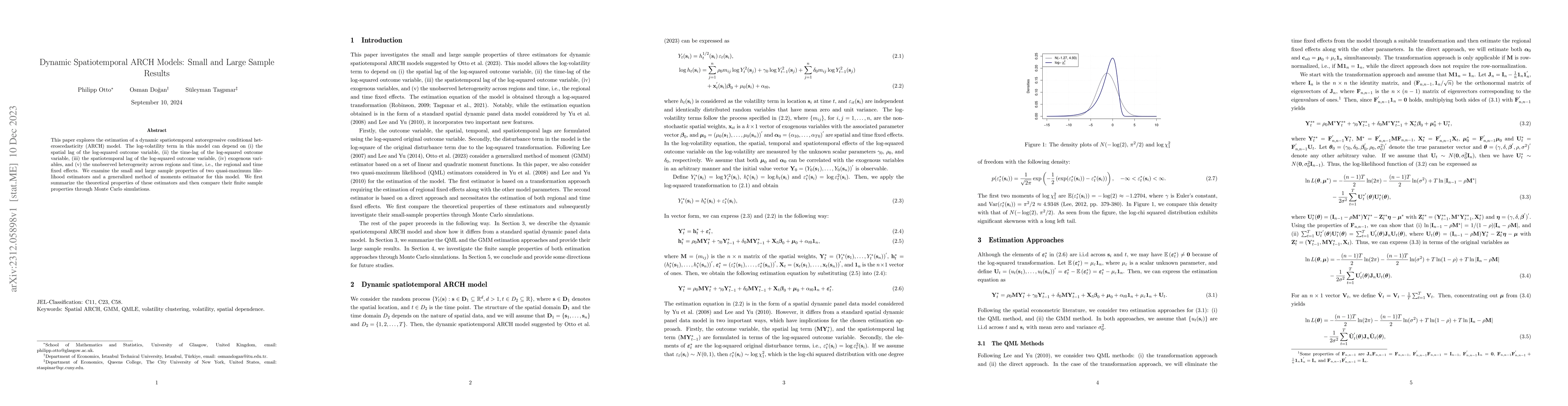

This paper explores the estimation of a dynamic spatiotemporal autoregressive conditional heteroscedasticity (ARCH) model. The log-volatility term in this model can depend on (i) the spatial lag of ...

Spatial and spatiotemporal volatility models are a class of models designed to capture spatial dependence in the volatility of spatial and spatiotemporal data. Spatial dependence in the volatility m...

This article introduces a dynamic spatiotemporal stochastic volatility (SV) model with explicit terms for the spatial, temporal, and spatiotemporal spillover effects. Moreover, the model includes ti...

Geo-referenced data are characterized by an inherent spatial dependence due to the geographical proximity. In this paper, we introduce a dynamic spatiotemporal autoregressive conditional heterosceda...

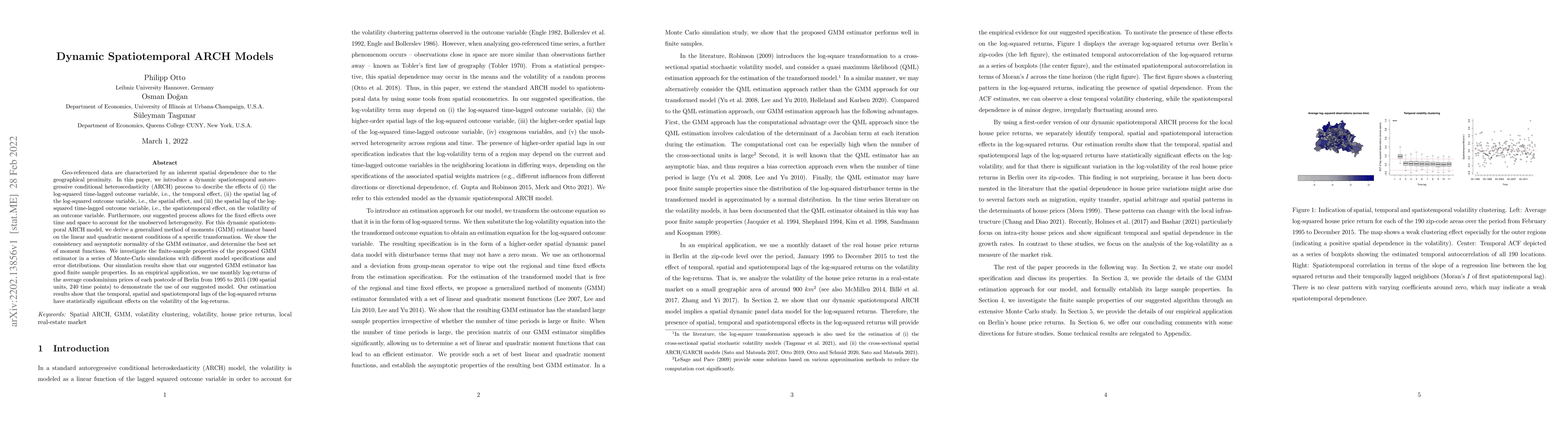

We introduce a dynamic spatiotemporal volatility model that extends traditional approaches by incorporating spatial, temporal, and spatiotemporal spillover effects, along with volatility-specific obse...