Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this article, we present a method for approximating affine processes on the cone of positive Hilbert-Schmidt operators using matrix-valued affine processes. By leveraging results from the theory ...

In this article we study multivariate continuous-time autoregressive moving-average (MCARMA) processes with values in convex cones. More specifically, we introduce matrix-valued MCARMA processes wit...

We study the long-time behavior of affine processes on positive self-adjoiont Hilbert-Schmidt operators which are of pure-jump type, conservative and have finite second moment. For subcritical proce...

We introduce a flexible and tractable infinite-dimensional stochastic volatility model. More specifically, we consider a Hilbert space valued Ornstein-Uhlenbeck-type process, whose instantaneous cov...

We show the existence of a broad class of affine Markov processes in the cone of positive self-adjoint Hilbert-Schmidt operators. Such processes are well-suited as infinite dimensional stochastic vo...

We present a function-valued stochastic volatility model designed to capture the continuous-time evolution of forward curves in fixed-income or commodity markets. The dynamics of the (logarithmic) for...

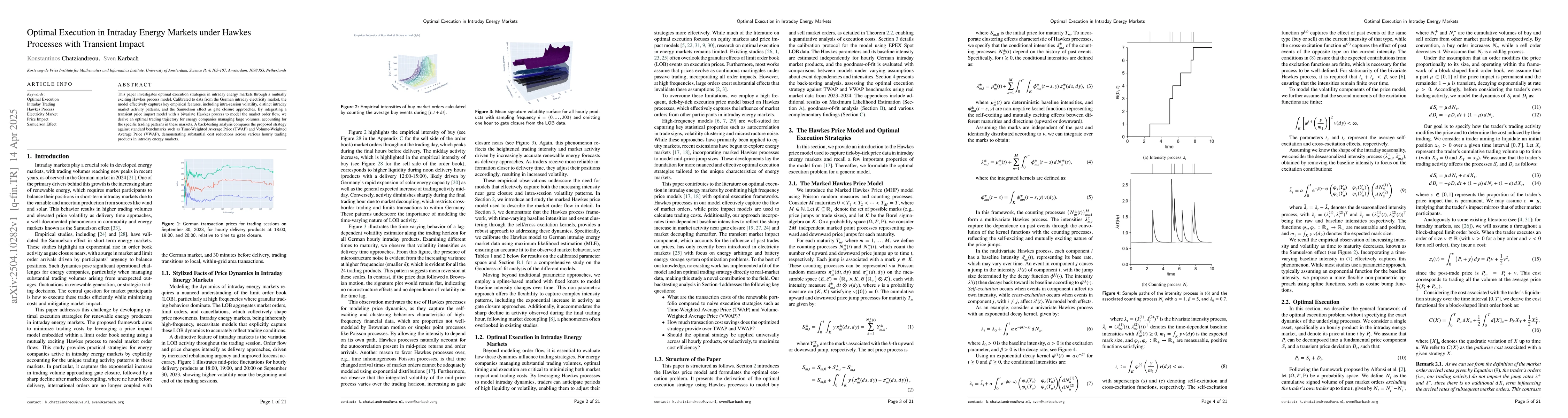

This paper investigates optimal execution strategies in intraday energy markets through a mutually exciting Hawkes process model. Calibrated to data from the German intraday electricity market, the mo...

In this paper, we examine continuous-time autoregressive moving-average (CARMA) processes on Banach spaces driven by L\'evy subordinators. We show their existence and cone-invariance, investigate thei...

We study the pricing of European-style options written on forward contracts within function-valued infinite-dimensional affine stochastic volatility models. The dynamics of the underlying forward pric...

We develop a semi-static framework for the variance-optimal hedging of multi-asset derivatives exposed to correlation and covariance risk. The approach combines continuous-time dynamic trading in the ...

We study the variance-optimal hedging of European contingent claims written on forwards. We assume that the dynamics of the underlying forward curves follow a Heath--Jarrow--Morton--Musiela stochastic...

We develop a signature-based framework for optimal execution in statistical arbitrage strategies with path-dependent predictive signals. Both the alpha process and the trading speed are modelled as li...