Academic Profile

Statistics

Similar Authors

Papers on arXiv

Copula-based time series models implicitly assume a finite Markov order. In reality a time series may not follow the Markov property. We modify the copula-based time series models by introducing a m...

Commodity price time series possess interesting features, such as heavy-tailedness, skewness, heteroskedasticity, and non-linear dependence structures. These features pose challenges for modeling an...

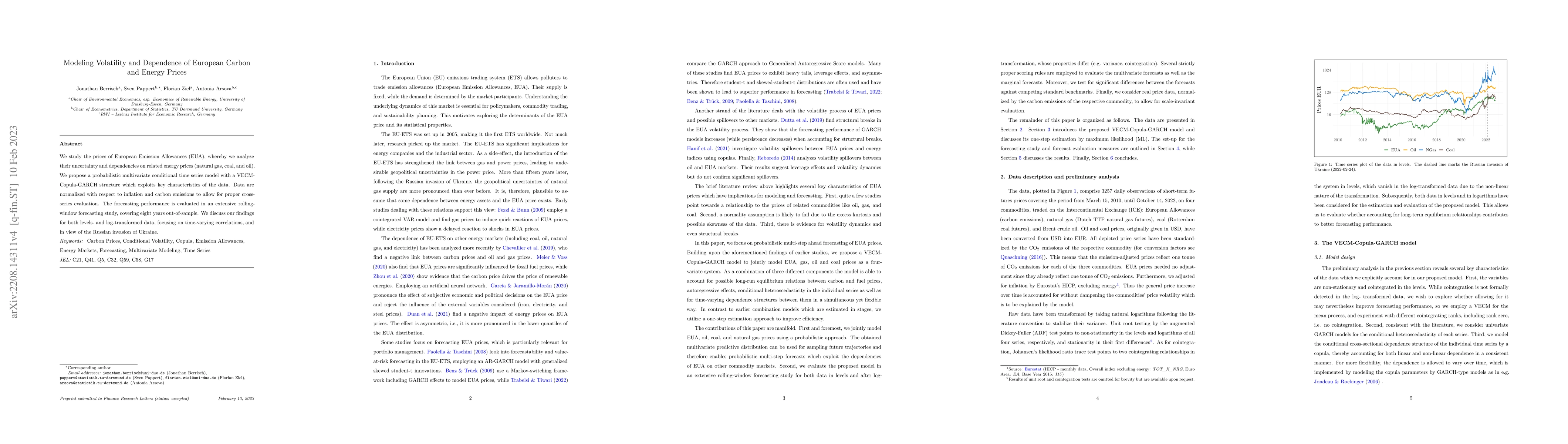

We study the prices of European Emission Allowances (EUA), whereby we analyze their uncertainty and dependencies on related energy prices (natural gas, coal, and oil). We propose a probabilistic mul...

Reliable gas price forecasts are an essential information for gas and energy traders, for risk managers and also economists. However, ahead of the war in Ukraine Europe began to suffer from substantia...

We view penalized risks through the lens of the calculus of variations. We consider risks comprised of a fitness-term (e.g. MSE) and a gradient-based penalty. After establishing the Euler-Lagrange fie...

Precise probabilistic forecasts are fundamental for energy risk management, and there is a wide range of both statistical and machine learning models for this purpose. Inherent to these probabilistic ...

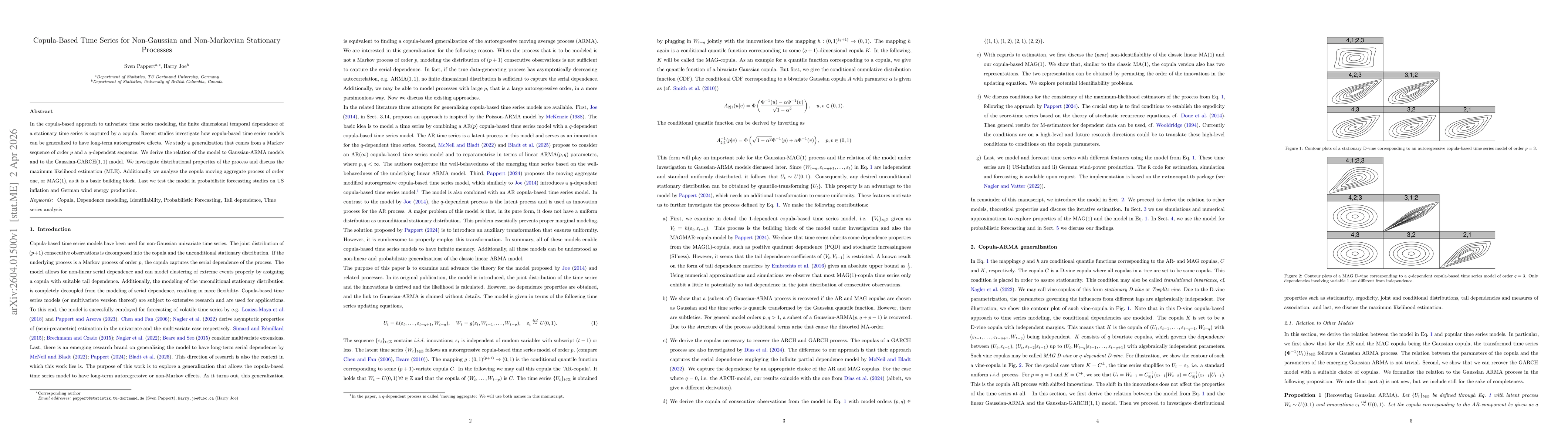

In the copula-based approach to univariate time series modeling, the finite dimensional temporal dependence of a stationary time series is captured by a copula. Recent studies investigate how copula-b...