Academic Profile

Statistics

Similar Authors

Papers on arXiv

The COVID19 pandemic highlighted the importance of non-traditional data sources, such as mobile phone data, to inform effective public health interventions and monitor adherence to such measures. Pr...

This is a review about financial dependencies which merges efforts in econophysics and financial economics during the last few years. We focus on the most relevant contributions to the analysis of a...

Pricing derivatives goes back to the acclaimed Black and Scholes model. However, such a modeling approach is known not to be able to reproduce some of the financial stylized facts, including the dyn...

Multilayer networks proved to be suitable in extracting and providing dependency information of different complex systems. The construction of these networks is difficult and is mostly done with a s...

The analysis of multidimensional data is becoming a more and more relevant topic in statistical and machine learning research. Given their complexity, such data objects are usually reshaped into mat...

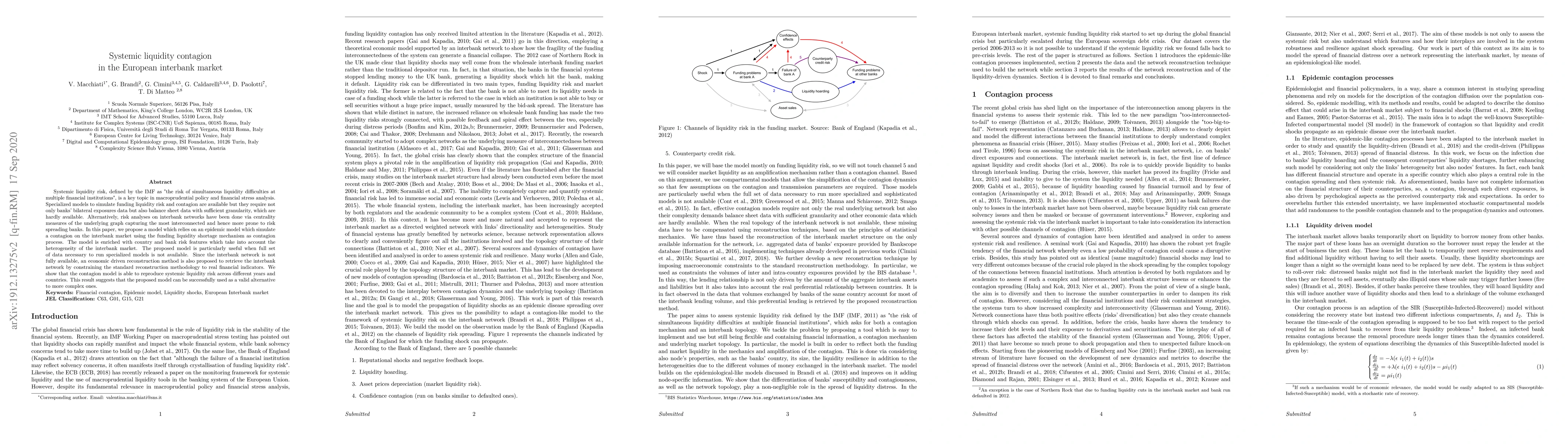

Systemic liquidity risk, defined by the IMF as "the risk of simultaneous liquidity difficulties at multiple financial institutions", is a key topic in macroprudential policy and financial stress ana...

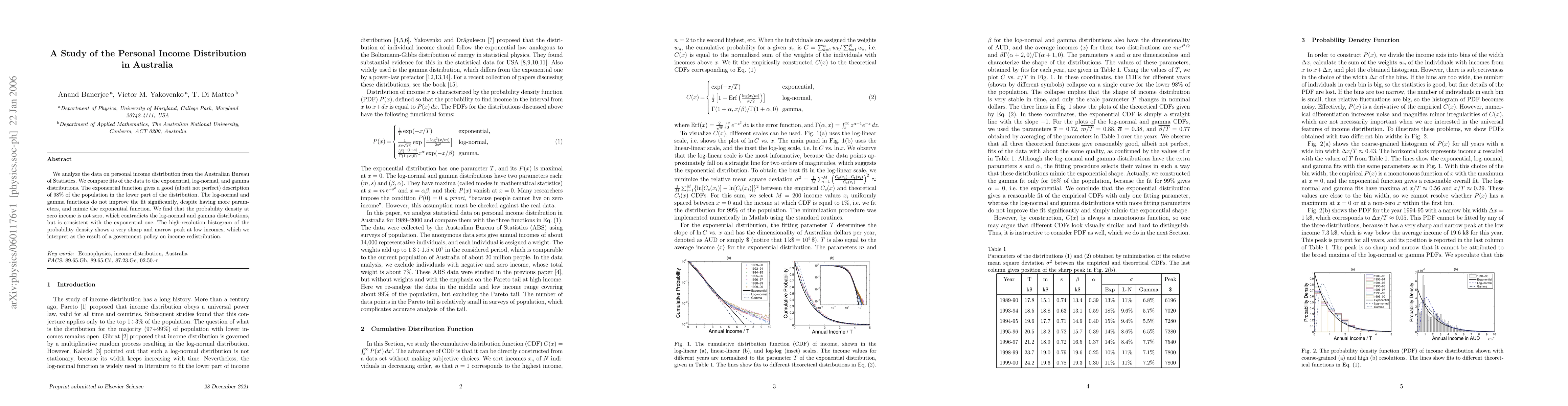

We analyze the data on personal income distribution from the Australian Bureau of Statistics. We compare fits of the data to the exponential, log-normal, and gamma distributions. The exponential funct...

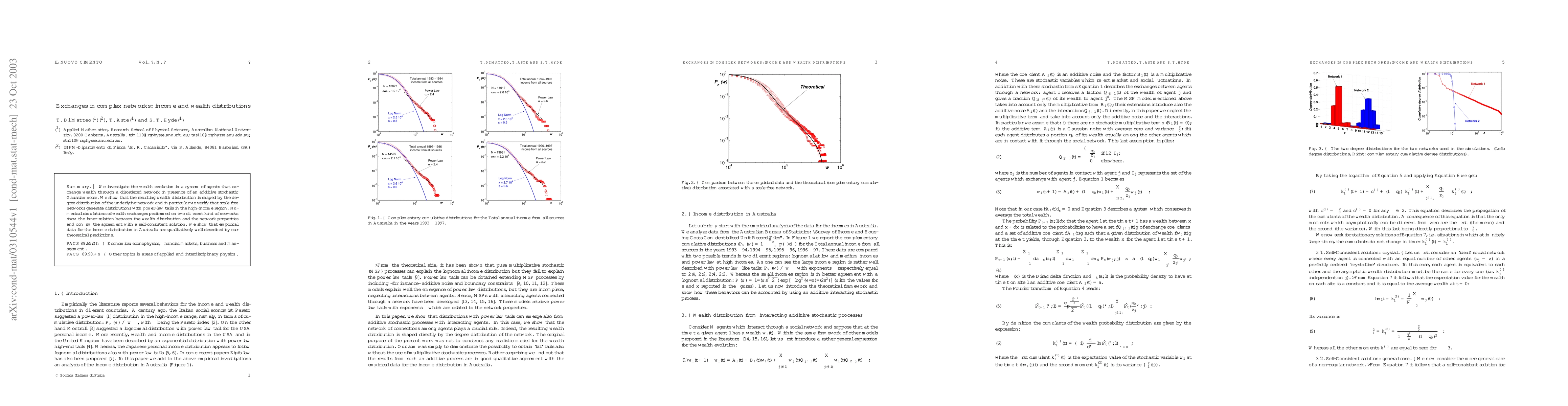

We investigate the wealth evolution in a system of agents that exchange wealth through a disordered network in presence of an additive stochastic Gaussian noise. We show that the resulting wealth dist...

We analyze the data on personal income distribution from the Australian Bureau of Statistics. We compare fits of the data to the exponential, log-normal, and gamma distributions. The exponential funct...

We investigate the wealth evolution in a system of agents that exchange wealth through a disordered network in presence of an additive stochastic Gaussian noise. We show that the resulting wealth dist...

This paper proposes a machine learning-based framework for asset selection and portfolio construction, termed the Best-Path Algorithm Sparse Graphical Model (BPASGM). The method extends the Best-Path ...