Academic Profile

Statistics

Similar Authors

Papers on arXiv

In multivariate time series analysis, spectral coherence measures the linear dependency between two time series at different frequencies. However, real data applications often exhibit nonlinear depe...

A nonparametric method is proposed for estimating the quantile spectra and cross-spectra introduced in Li (2012; 2014) as bivariate functions of frequency and quantile level. The method is based on ...

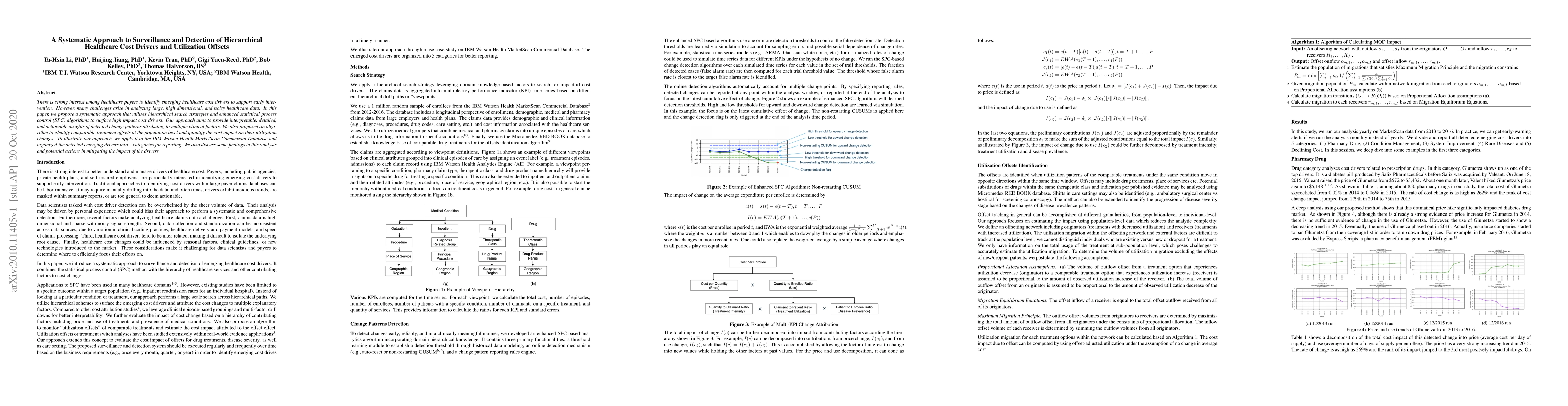

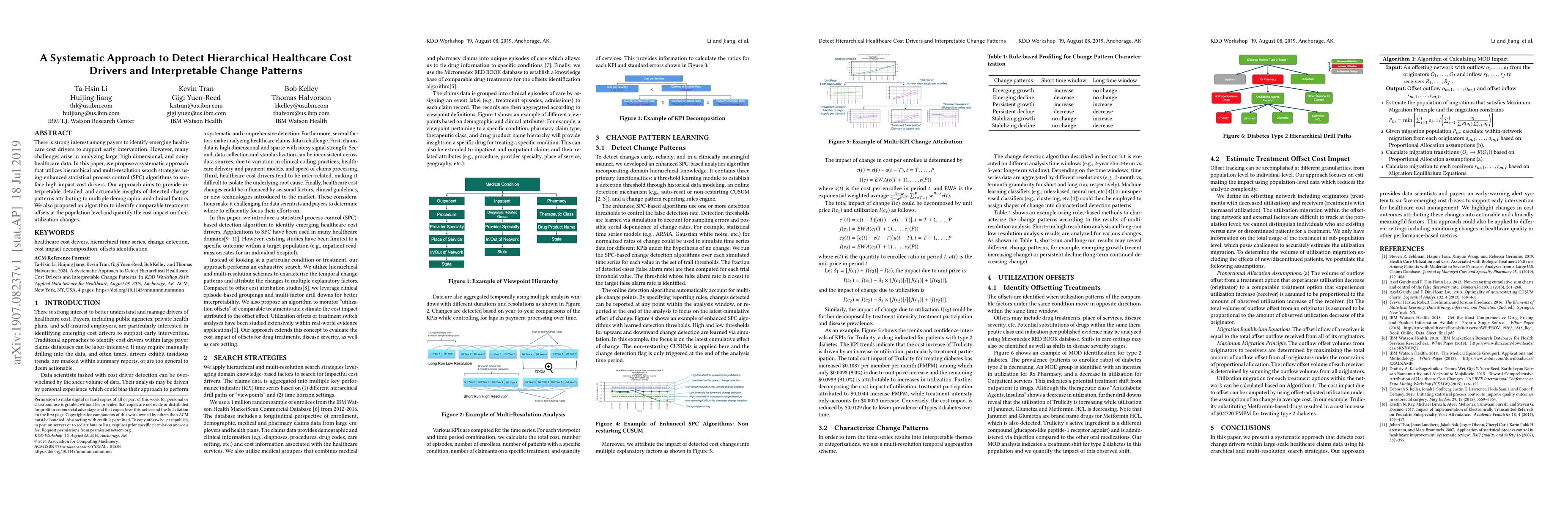

There is strong interest among healthcare payers to identify emerging healthcare cost drivers to support early intervention. However, many challenges arise in analyzing large, high dimensional, and ...

In this paper, a new estimation method is introduced for the quantile spectrum, which uses a parametric form of the autoregressive (AR) spectrum coupled with nonparametric smoothing. The method begi...

There is strong interest among payers to identify emerging healthcare cost drivers to support early intervention. However, many challenges arise in analyzing large, high dimensional, and noisy healt...

The quantile-crossing spectrum is the spectrum of quantile-crossing processes created from a time series by the indicator function that shows whether or not the time series lies above or below a given...

The quantile spectrum was introduced in Li (2012; 2014) as an alternative tool for spectral analysis of time series. It has the capability of providing a richer view of time series data than that offe...

Quantile regression is a powerful tool capable of offering a richer view of the data as compared to linear-squares regression. Quantile regression is typically performed individually on a few quantile...

Spline quantile regression (SQR) is a method introduced recently by Li and Megiddo (2026) for linear quantile regression where the regression coefficients are treated as smooth functions of the quanti...