Academic Profile

Statistics

Similar Authors

Papers on arXiv

The experience of unknown events such as financial crises and infectious disease crises has revealed the limitations of measuring risk under a fixed probability measure. In order to solve this probl...

Signatures, one of the key concepts of rough path theory, have recently gained prominence as a means to find appropriate feature sets in machine learning systems. In this paper, in order to compute ...

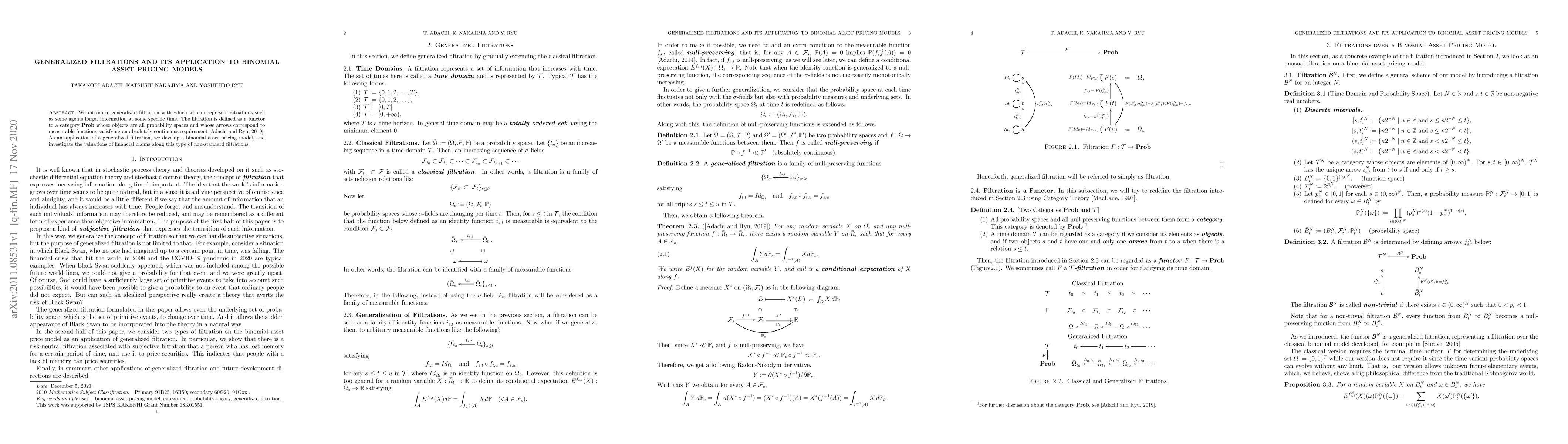

We introduce generalized filtration with which we can represent situations such as some agents forget information at some specific time. The filtration is defined as a functor to a category Prob who...

Adachi and Ryu introduced a category Prob of probability spaces whose objects are all probability spaces and whose arrows correspond to measurable functions satisfying an absolutely continuous requi...

This letter investigates the dynamic relationship between market efficiency, liquidity, and multifractality of Bitcoin. We find that before 2013 liquidity is low and the Hurst exponent is less than ...

Classical filtrations in probability theory formalize the accumulation of information along a linear time axis: the past is unique and the present evolves into an uncertain future. In many contexts, h...

We introduce a new notion of arbitrage based on global loop effects in filtered market systems. Given a filtration modeled as a contravariant functor $F : \mathcal{T}^{op} \to \mathrm{Prob}$, we consi...

We develop a cohomological framework for martingale theory based on categorical filtrations, where time is modeled by a small category and a filtration is defined as a contravariant functor to the cat...