Academic Profile

Statistics

Similar Authors

Papers on arXiv

Combining model-based and model-free reinforcement learning approaches, this paper proposes and analyzes an $\epsilon$-policy gradient algorithm for the online pricing learning task. The algorithm e...

The emergence of price comparison websites (PCWs) has presented insurers with unique challenges in formulating effective pricing strategies. Operating on PCWs requires insurers to strike a delicate ...

This work uses the entropy-regularised relaxed stochastic control perspective as a principled framework for designing reinforcement learning (RL) algorithms. Herein agent interacts with the environm...

We develop a probabilistic framework for analysing model-based reinforcement learning in the episodic setting. We then apply it to study finite-time horizon stochastic control problems with linear d...

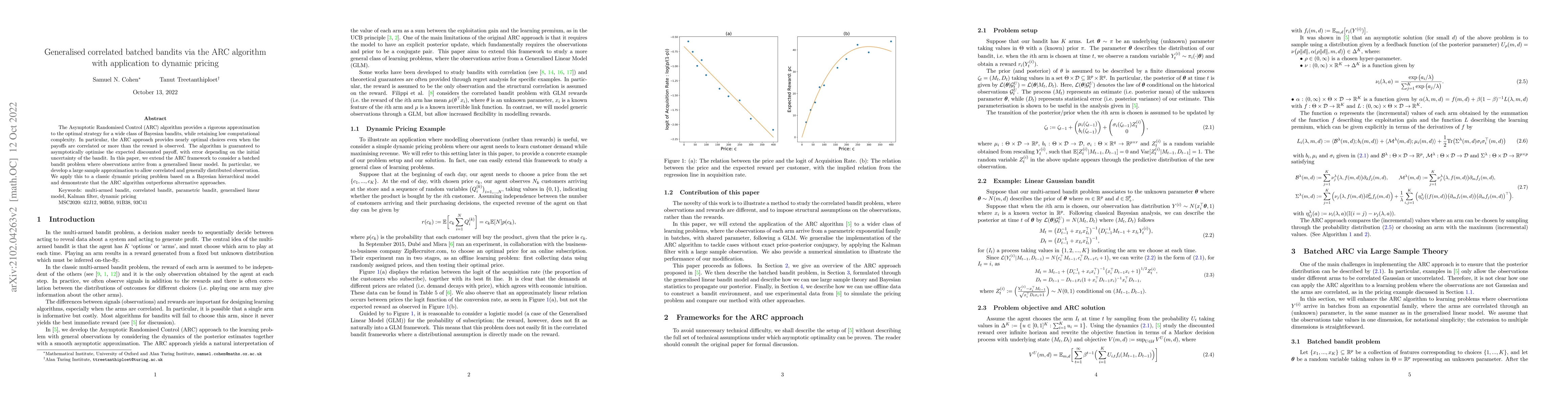

The Asymptotic Randomised Control (ARC) algorithm provides a rigorous approximation to the optimal strategy for a wide class of Bayesian bandits, while retaining low computational complexity. In par...

We consider a general multi-armed bandit problem with correlated (and simple contextual and restless) elements, as a relaxed control problem. By introducing an entropy regularisation, we obtain a sm...

We study dynamic allocation problems for discrete time multi-armed bandits under uncertainty, based on the the theory of nonlinear expectations. We show that, under strong independence of the bandit...

We study the loan contracts offered by decentralised loan protocols (DLPs) through the lens of financial derivatives. DLPs, which effectively are clearinghouses, facilitate transactions between option...

We analyse the regret arising from learning the price sensitivity parameter $\kappa$ of liquidity takers in the ergodic version of the Avellaneda-Stoikov market making model. We show that a learning a...