Academic Profile

Statistics

Similar Authors

Papers on arXiv

In many lower-and-middle income countries including South Africa, data access in health facilities is restricted due to patient privacy and confidentiality policies. Further, since clinical data is ...

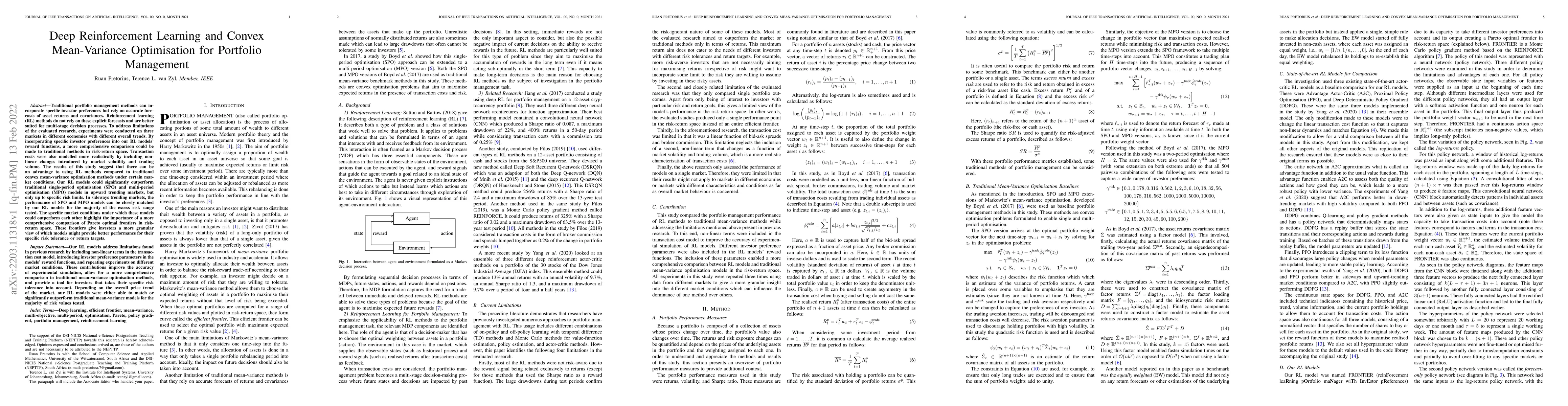

Traditional portfolio management methods can incorporate specific investor preferences but rely on accurate forecasts of asset returns and covariances. Reinforcement learning (RL) methods do not rel...

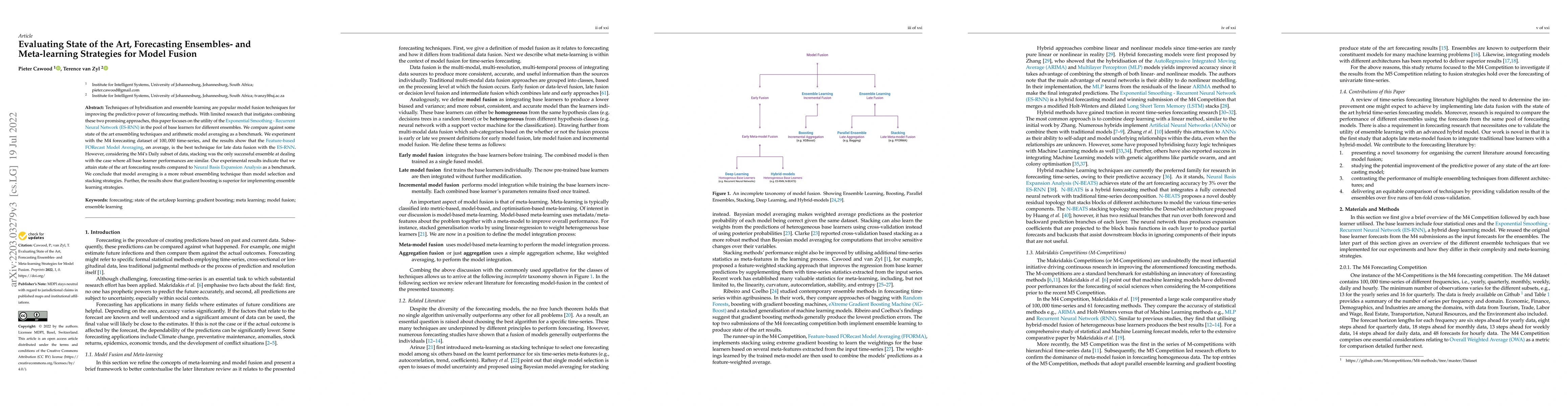

Techniques of hybridisation and ensemble learning are popular model fusion techniques for improving the predictive power of forecasting methods. With limited research that instigates combining these...

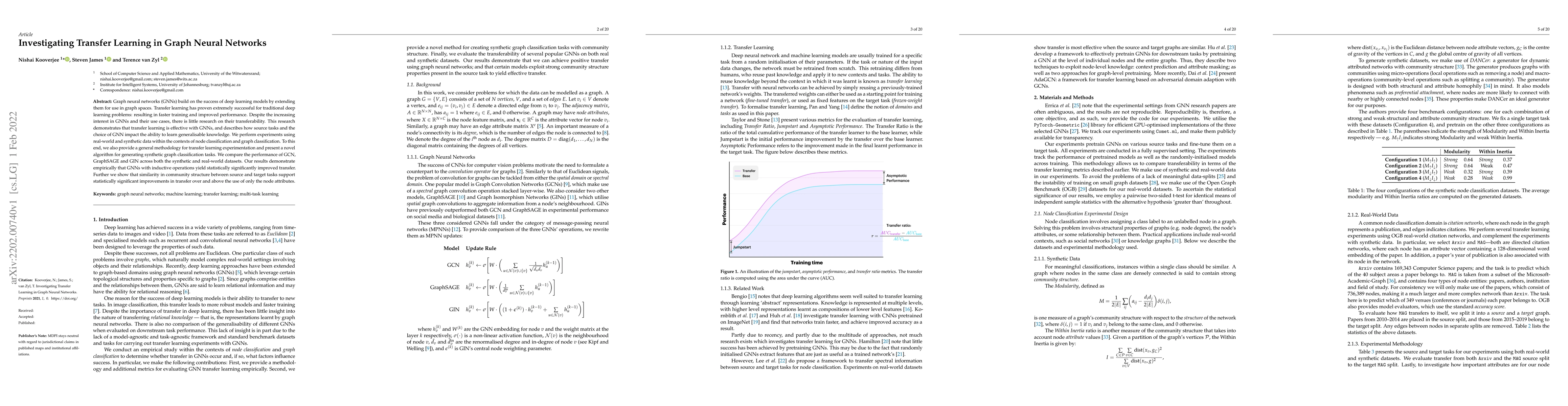

Graph neural networks (GNNs) build on the success of deep learning models by extending them for use in graph spaces. Transfer learning has proven extremely successful for traditional deep learning p...

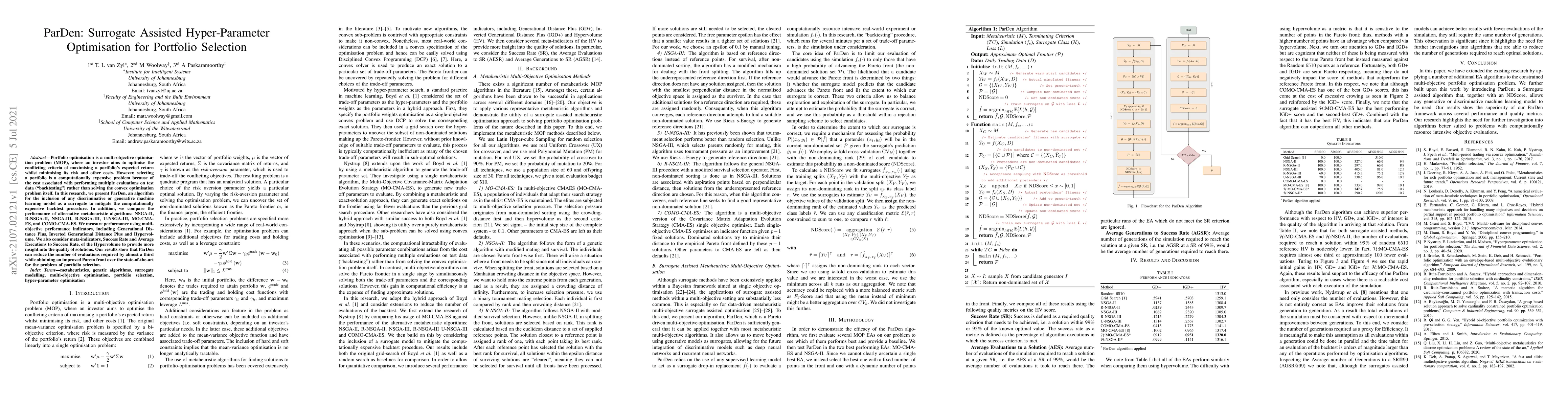

Portfolio optimisation is a multi-objective optimisation problem (MOP), where an investor aims to optimise the conflicting criteria of maximising a portfolio's expected return whilst minimising its ...

Mean-variance portfolio decisions that combine prediction and optimisation have been shown to have poor empirical performance. Here, we consider the performance of various shrinkage methods by their...

The artificial segmentation of an investment management process into a workflow with silos of offline human operators can restrict silos from collectively and adaptively pursuing a unified optimal i...

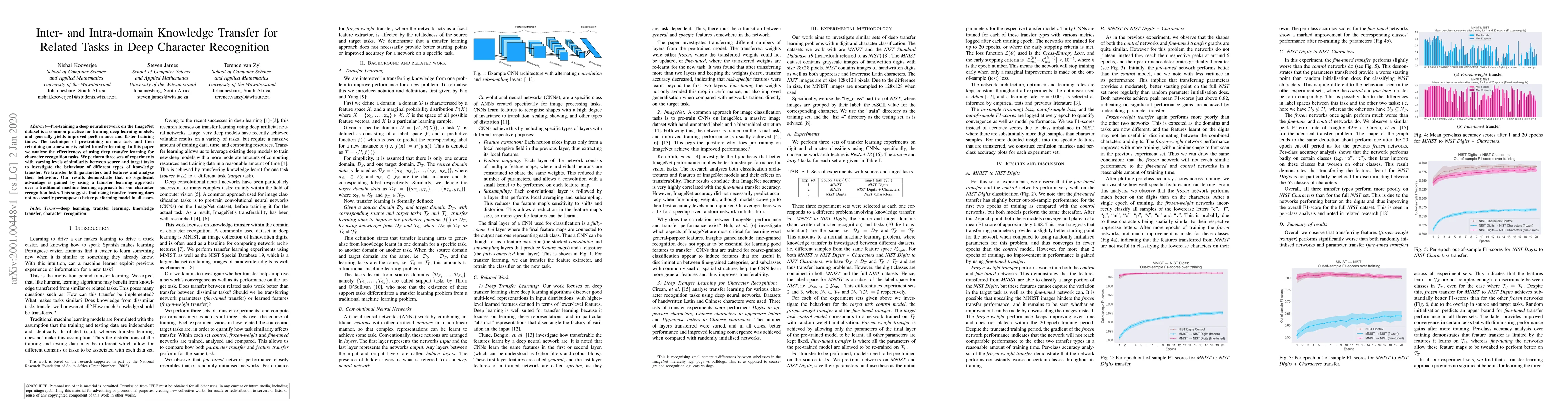

Pre-training a deep neural network on the ImageNet dataset is a common practice for training deep learning models, and generally yields improved performance and faster training times. The technique ...

Backtests on historical data are the basis for practical evaluations of portfolio selection rules, but their reliability is often limited by reliance on a single sample path. This can lead to high est...