Academic Profile

Statistics

Similar Authors

Papers on arXiv

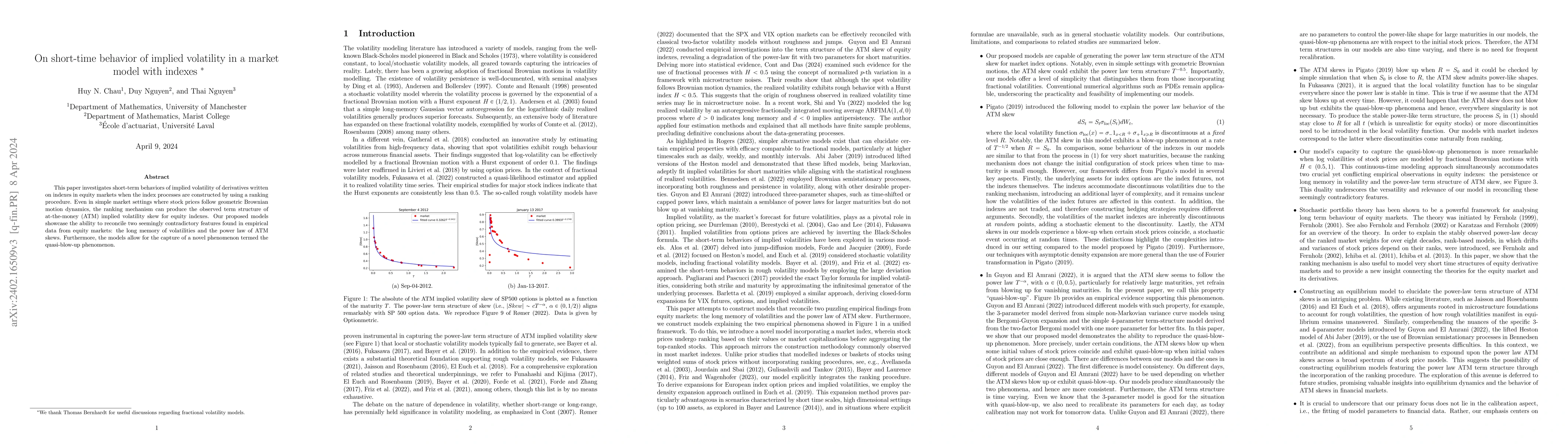

This paper investigates short-term behaviors of implied volatility of derivatives written on indexes in equity markets when the index processes are constructed by using a ranking procedure. Even in ...

This paper presents the first industry-standard open-source machine learning (ML) benchmark to allow perfor mance and accuracy evaluation of mobile devices with different AI chips and software stack...

We consider an expected utility maximization problem where the utility function is not necessarily concave and the time horizon is uncertain. We establish a necessary and sufficient condition for th...

We study the expected utility maximization problem of a large investor who is allowed to make transactions on tradable assets in an incomplete financial market with endogenous permanent market impac...

In a reinforcement learning (RL) framework, we study the exploratory version of the continuous time expected utility (EU) maximization problem with a portfolio constraint that includes widely-used fin...

Large language models (LLMs) generate fluent text yet often default to safe, generic phrasing, raising doubts about their ability to handle creativity. We formalize this tendency as a Galton-style reg...

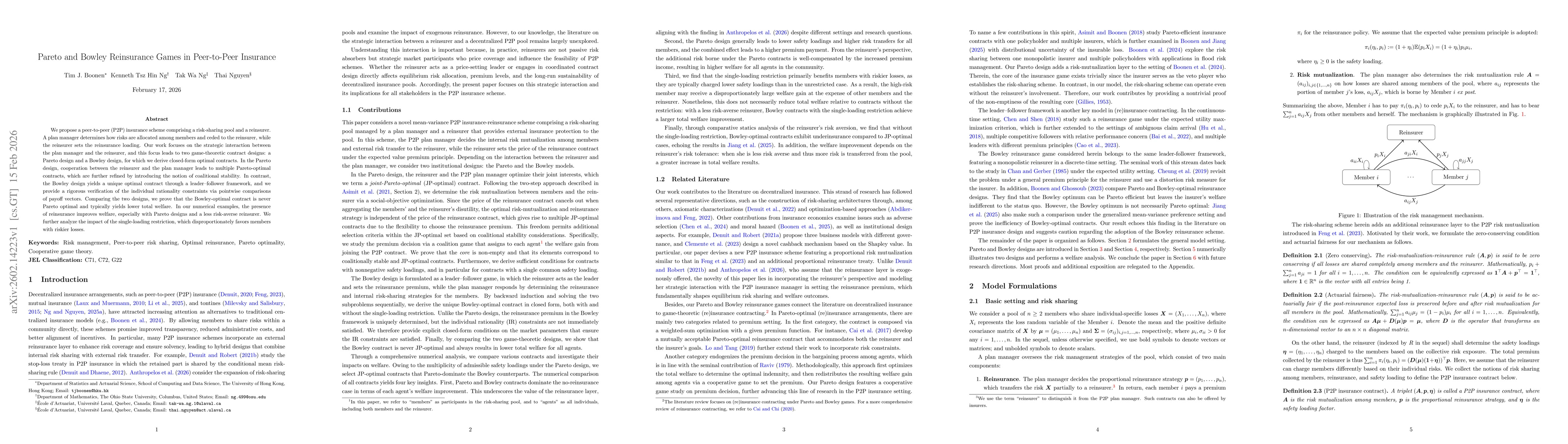

We propose a peer-to-peer (P2P) insurance scheme comprising a risk-sharing pool and a reinsurer. A plan manager determines how risks are allocated among members and ceded to the reinsurer, while the r...

We consider the problem of active portfolio management, where an investor seeks the portfolio with maximal expected utility of the difference between the terminal wealth of their strategy and a propor...

We study the problem of optimal portfolio selection under stochastic volatility within a continuous time reinforcement learning framework with portfolio constraints. Exploration is modeled through ent...