Academic Profile

Statistics

Similar Authors

Papers on arXiv

Bootstrap percolation is a process that is used to model the spread of an infection on a given graph. In the model considered here each vertex is equipped with an individual threshold. As soon as th...

The aim of this paper is to quantify and manage systemic risk caused by default contagion in the interbank market. We model the market as a random directed network, where the vertices represent fina...

We extend the notion of mean-field SDEs to SDEs driven by $G$-Brownian motion. More precisely, we consider a $G$-SDE where the coefficients depend not only on time and the current state but also on ...

This is a supplement to the paper "Liquidity based modeling of asset price bubbles via random matching". The supplement is organized as follows. First, we prove Theorem 3.13 in [1] which provides th...

We introduce the notions of Collective Arbitrage and of Collective Super-replication in a discrete-time setting where agents are investing in their markets and are allowed to cooperate through excha...

In this paper we study the evolution of asset price bubbles driven by contagion effects spreading among investors via a random matching mechanism in a discrete-time version of the liquidity based mo...

In this paper we employ deep learning techniques to detect financial asset bubbles by using observed call option prices. The proposed algorithm is widely applicable and model-independent. We test th...

We deduce stability and pathwise uniqueness for a McKean-Vlasov equation with random coefficients and a multidimensional Brownian motion as driver. Our analysis focuses on a non-Lipschitz drift coef...

The objective is to develop a general stochastic approach to delays on financial markets. We suggest such a concept in the context of large platonic markets, which allow infinitely many assets and i...

We establish stability and pathwise uniqueness of solutions to Wiener noise driven McKean-Vlasov equations with random non-Lipschitz continuous coefficients. In the deterministic case, we also obtai...

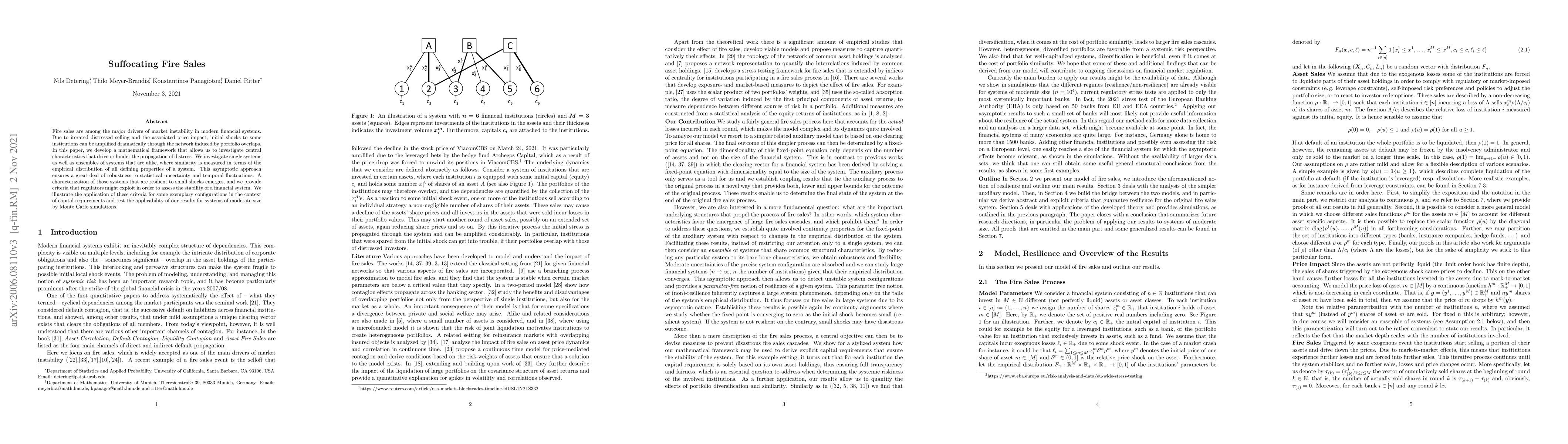

Fire sales are among the major drivers of market instability in modern financial systems. Due to iterated distressed selling and the associated price impact, initial shocks to some institutions can ...

This paper establishes results on the existence and uniqueness of solutions to McKean-Vlasov equations, also called mean-field stochastic differential equations, in an infinite-dimensional Hilbert s...

We analyze multi-dimensional mean-field stochastic differential equations where the drift depends on the law in form of a Lebesgue integral with respect to the pushforward measure of the solution. W...

We examine existence and uniqueness of strong solutions of multi-dimensional mean-field stochastic differential equations with irregular drift coefficients. Furthermore, we establish Malliavin diffe...

We propose a novel concept of a Systemic Optimal Risk Transfer Equilibrium (SORTE), which is inspired by the B\"uhlmann's classical notion of an Equilibrium Risk Exchange. We provide sufficient gene...

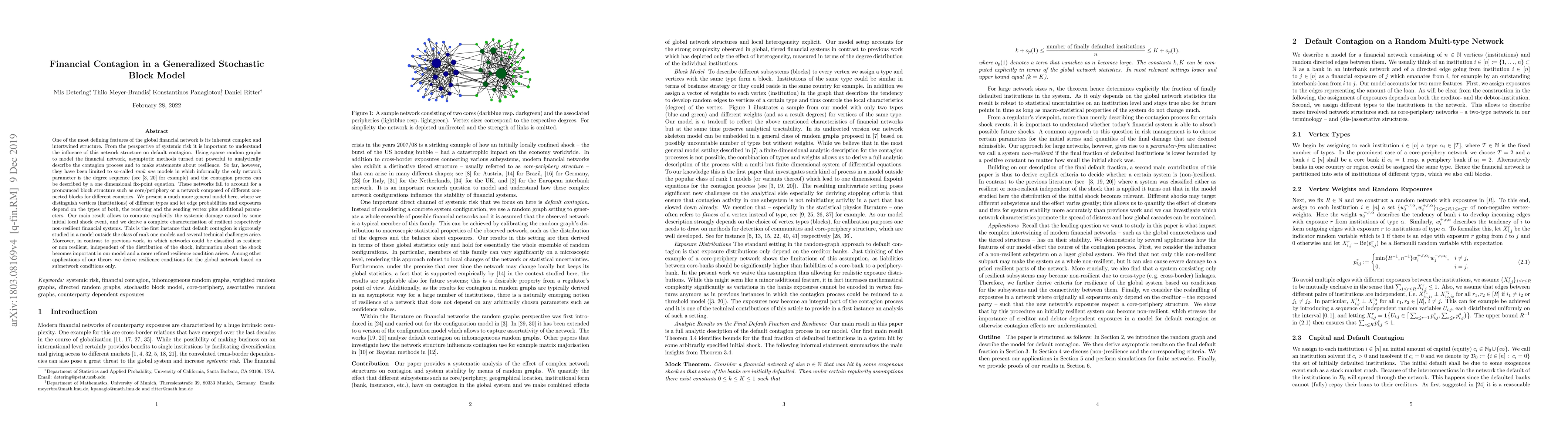

One of the most defining features of the global financial network is its inherent complex and intertwined structure. From the perspective of systemic risk it is important to understand the influence...

This paper investigates systemic risk measures for stochastic financial networks of explicitly modelled bilateral liabilities. We extend the notion of systemic risk measures from Biagini, Fouque, Frit...

We study regularity properties of the unique solution of a mean-field $G$-SDE. More precisely, we consider a mean-field $G$-SDE with square-integrable random initial condition and establish its first ...

We present a tractable class of one-dimensional McKean-Vlasov equations that allow for unique strong solutions and extend the dynamics of various SIS epidemic models that are well-established in the l...