2

arXiv Papers

5

Total Publications

Profile

Academic Profile

Metrics

Statistics

2

arXiv Papers

5

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Rate-optimal estimation of mixed semimartingales

Consider the sum $Y=B+B(H)$ of a Brownian motion $B$ and an independent fractional Brownian motion $B(H)$ with Hurst parameter $H\in(0,1)$. Surprisingly, even though $B(H)$ is not a semimartingale, ...

arXiv

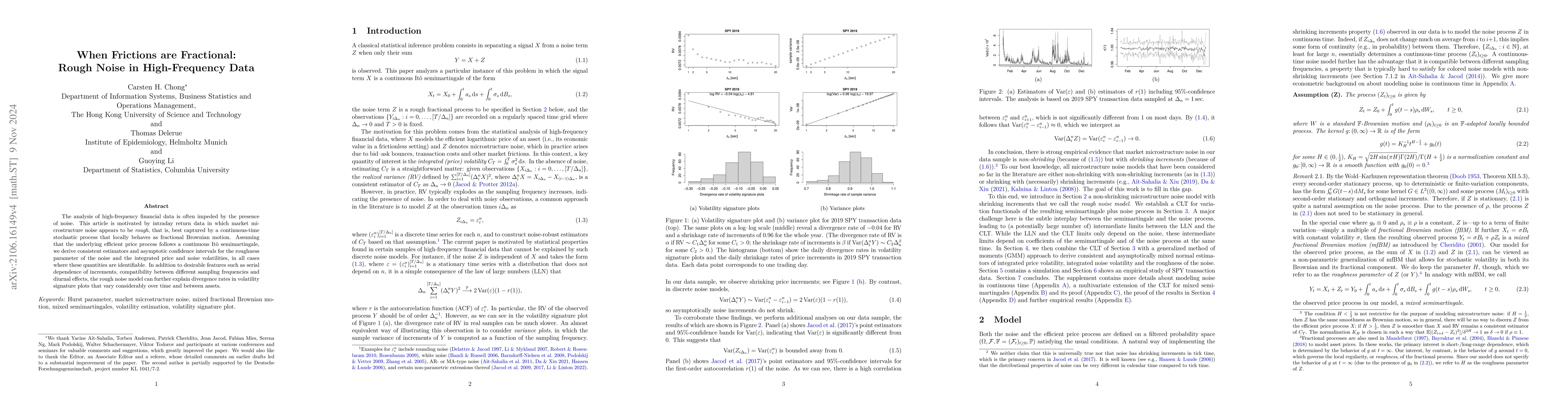

When Frictions are Fractional: Rough Noise in High-Frequency Data

The analysis of high-frequency financial data is often impeded by the presence of noise. This article is motivated by intraday transactions data in which market microstructure noise appears to be ro...