Academic Profile

Statistics

Similar Authors

Papers on arXiv

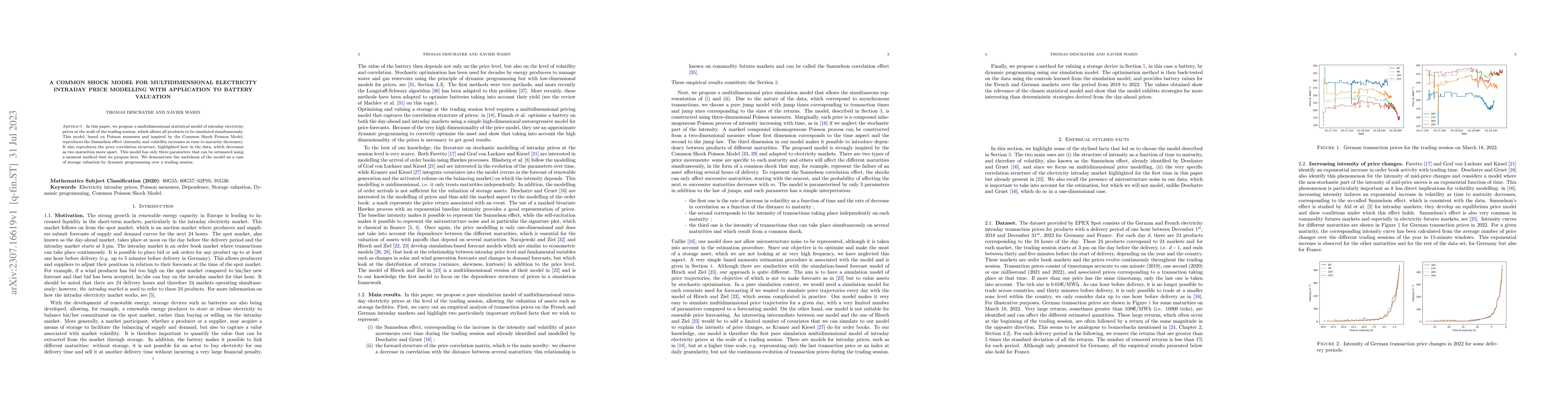

In this paper, we propose a multidimensional statistical model of intraday electricity prices at the scale of the trading session, which allows all products to be simulated simultaneously. This mode...

We consider a 2-dimensional marked Hawkes process with increasing baseline intensity in order to model prices on electricity intraday markets. This model allows to represent different empirical fact...

We derive a model based on the structure of dependence between a Brownian motion and its reflection according to a barrier. The structure of dependence presents two states of correlation: one of com...

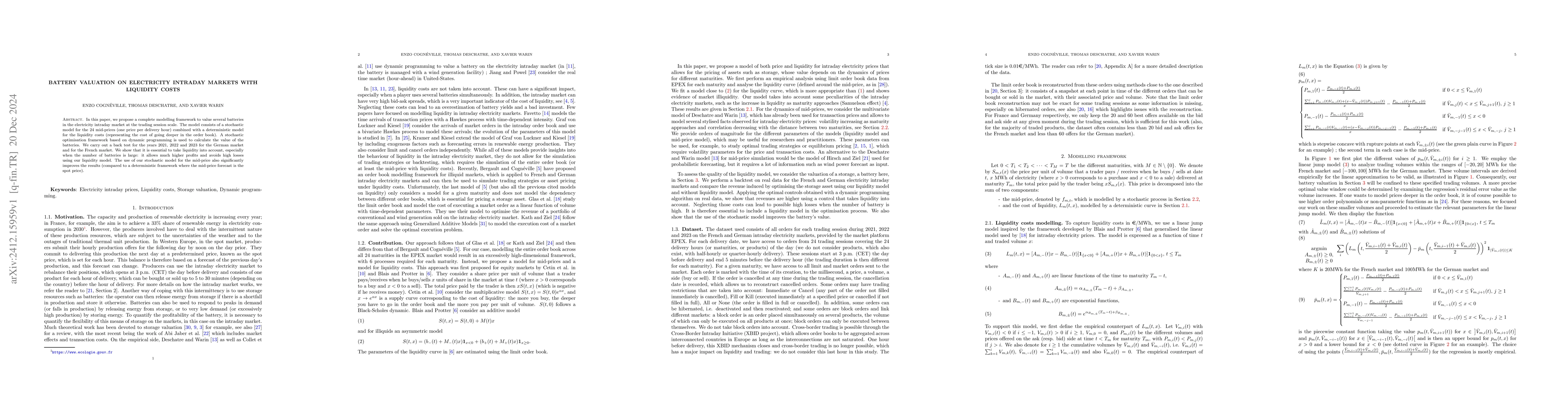

In this paper, we propose a complete modelling framework to value several batteries in the electricity intraday market at the trading session scale. The model consists of a stochastic model for the 24...

We prove a law of large numbers and functional central limit theorem for a class of multivariate Hawkes processes with time-dependent reproduction rate. We address the difficulties induced by the use ...

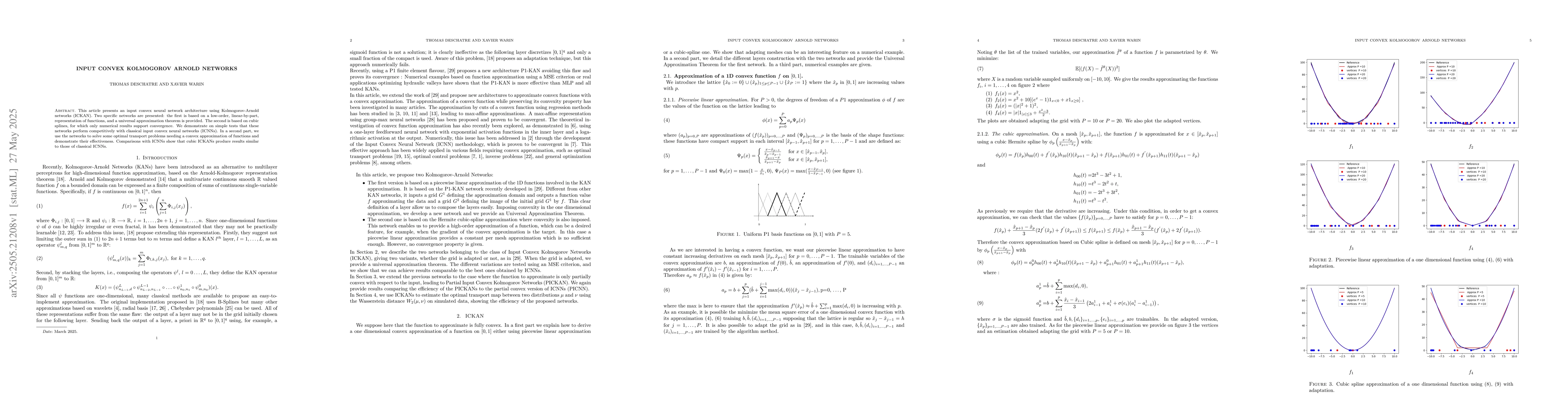

This article presents an input convex neural network architecture using Kolmogorov-Arnold networks (ICKAN). Two specific networks are presented: the first is based on a low-order, linear-by-part, repr...

We consider the problem of estimating the parameters of a non-stationary Hawkes process with time-dependent reproduction rate and baseline intensity. Our approach relies on the standard maximum likeli...