Academic Profile

Statistics

Similar Authors

Papers on arXiv

Modern financial electronic exchanges are an exciting and fast-paced marketplace where billions of dollars change hands every day. They are also rife with manipulation and fraud. Detecting such acti...

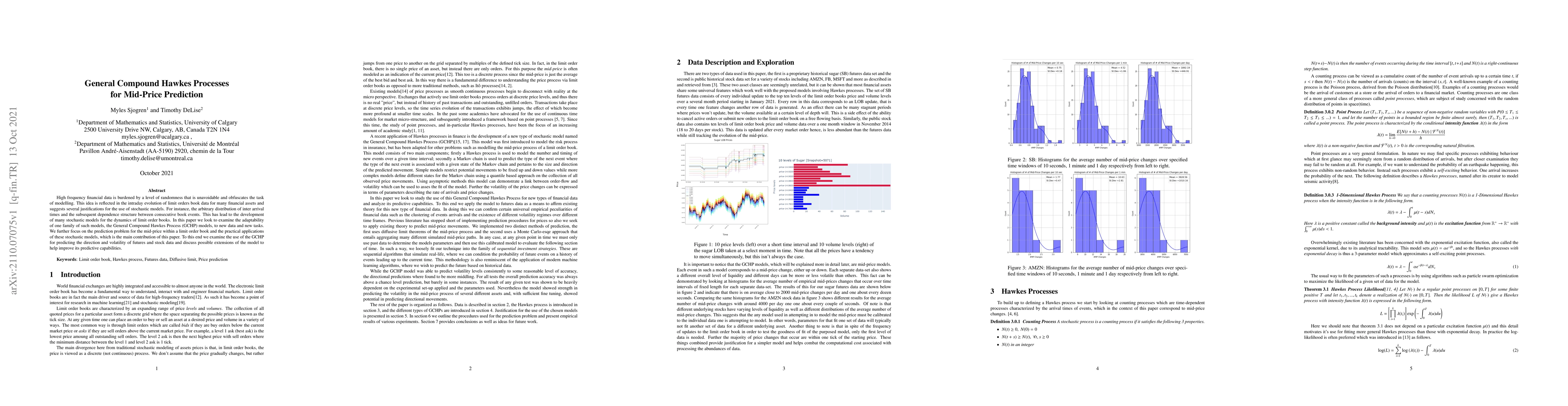

High frequency financial data is burdened by a level of randomness that is unavoidable and obfuscates the task of modelling. This idea is reflected in the intraday evolution of limit orders book dat...

This research investigates pricing financial options based on the traditional martingale theory of arbitrage pricing applied to neural SDEs. We treat neural SDEs as universal It\^o process approxima...

This research proposes a data segmentation algorithm which combines t-SNE, DBSCAN, and Random Forest classifier to form an end-to-end pipeline that separates data into natural clusters and produces ...

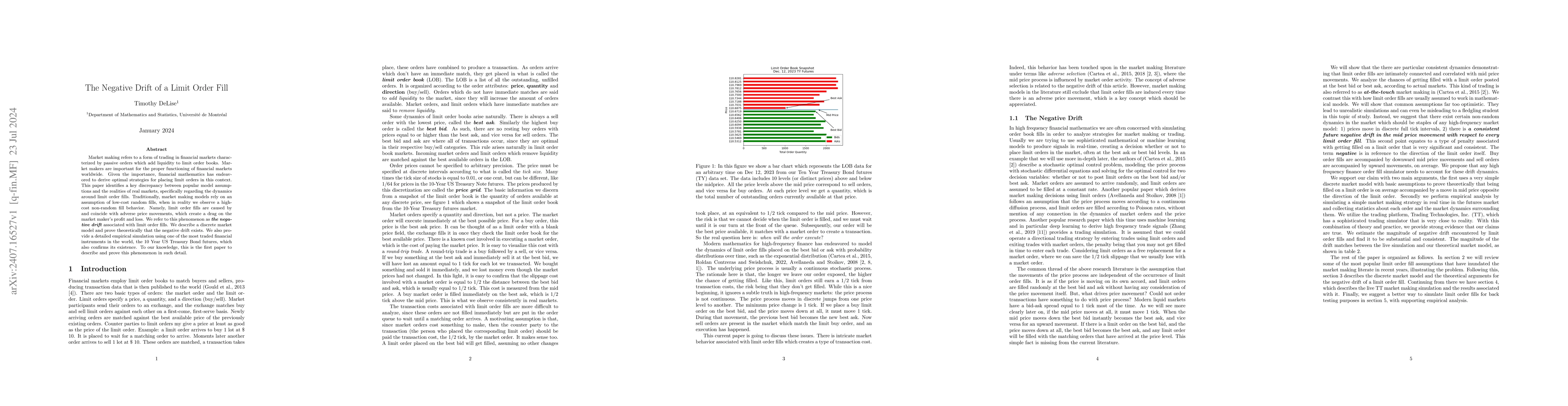

Market making refers to a form of trading in financial markets characterized by passive orders which add liquidity to limit order books. Market makers are important for the proper functioning of finan...