1

arXiv Papers

1

Total Publications

Profile

Academic Profile

Metrics

Statistics

1

arXiv Papers

1

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

STORM: A Spatio-Temporal Factor Model Based on Dual Vector Quantized

Variational Autoencoders for Financial Trading

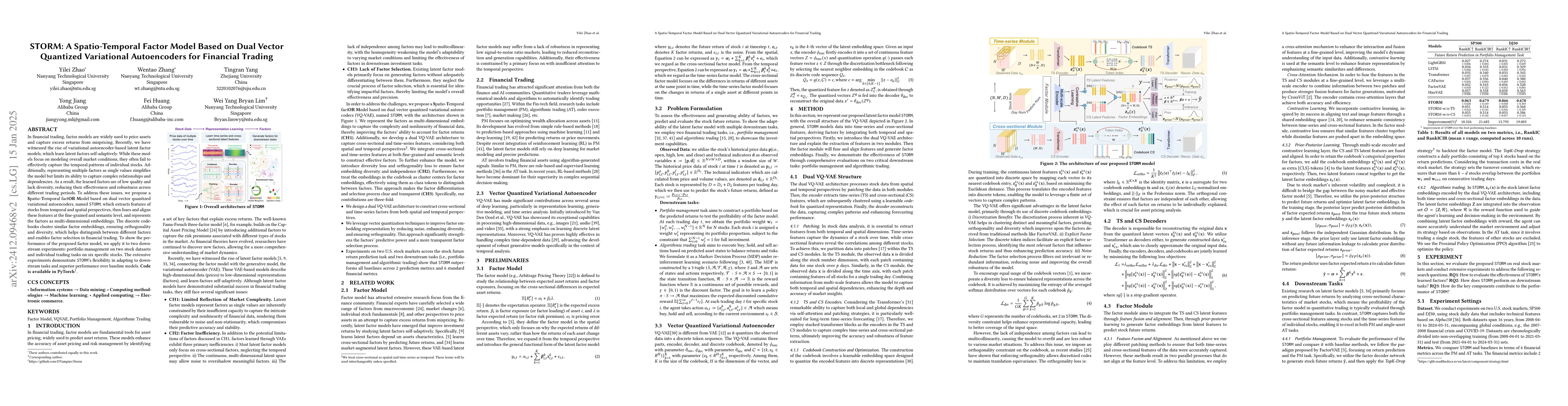

In financial trading, factor models are widely used to price assets and capture excess returns from mispricing. Recently, we have witnessed the rise of variational autoencoder-based latent factor mode...