Academic Profile

Statistics

Similar Authors

Papers on arXiv

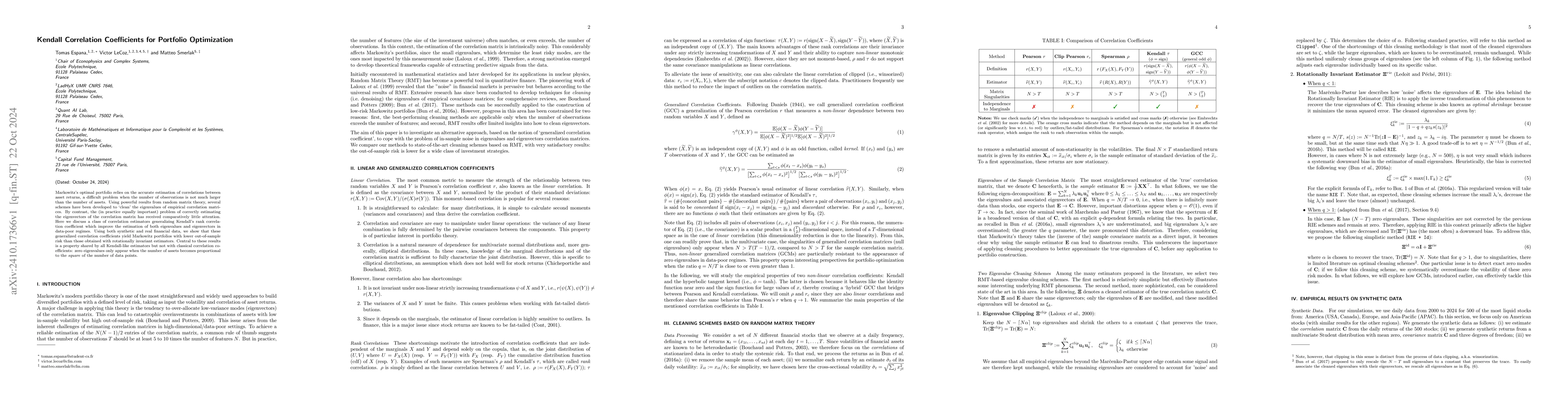

Markowitz's optimal portfolio relies on the accurate estimation of correlations between asset returns, a difficult problem when the number of observations is not much larger than the number of assets....

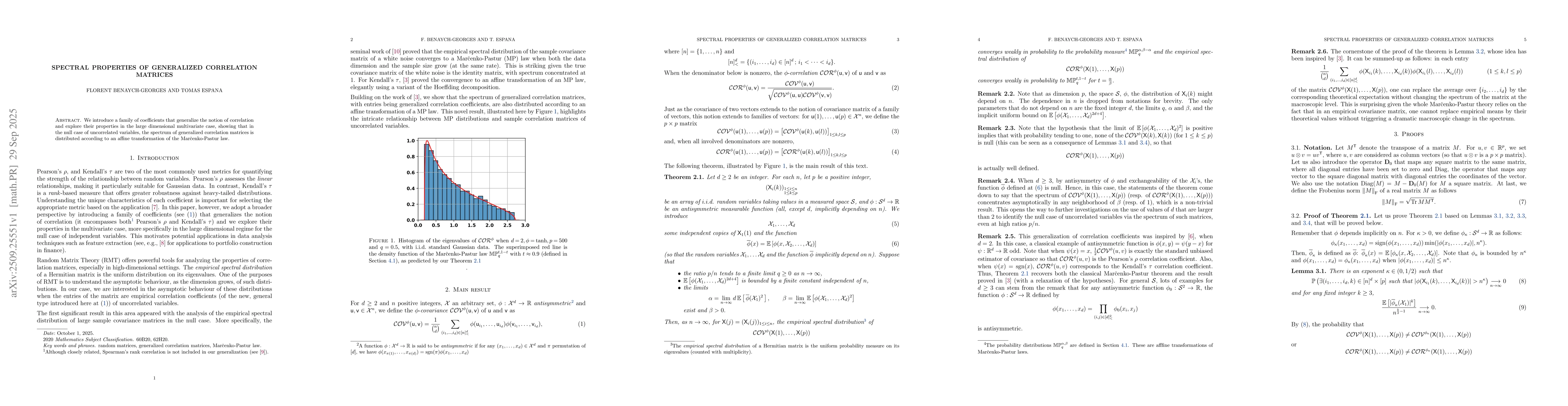

Bandeira et al. (2017) show that the eigenvalues of the Kendall correlation matrix of $n$ i.i.d. random vectors in $\mathbb{R}^p$ are asymptotically distributed like $1/3 + (2/3)Y_q$, where $Y_q$ has ...

We introduce a family of coefficients that generalize the notion of correlation and explore their properties in the large dimensional multivariate case, showing that in the null case of uncorrelated v...

We investigate the use of Reinforcement Learning for the optimal execution of meta-orders, where the objective is to execute incrementally large orders while minimizing implementation shortfall and ma...