Academic Profile

Statistics

Similar Authors

Papers on arXiv

We develop a Bayesian framework for cointegrated structural VAR models identified by two-state Markovian breaks in conditional covariances. The resulting structural VEC specification with Markov-swi...

We design a novel, nonlinear single-source-of-error model for analysis of multiple business cycles. The model's specification is intended to capture key empirical characteristics of business cycle d...

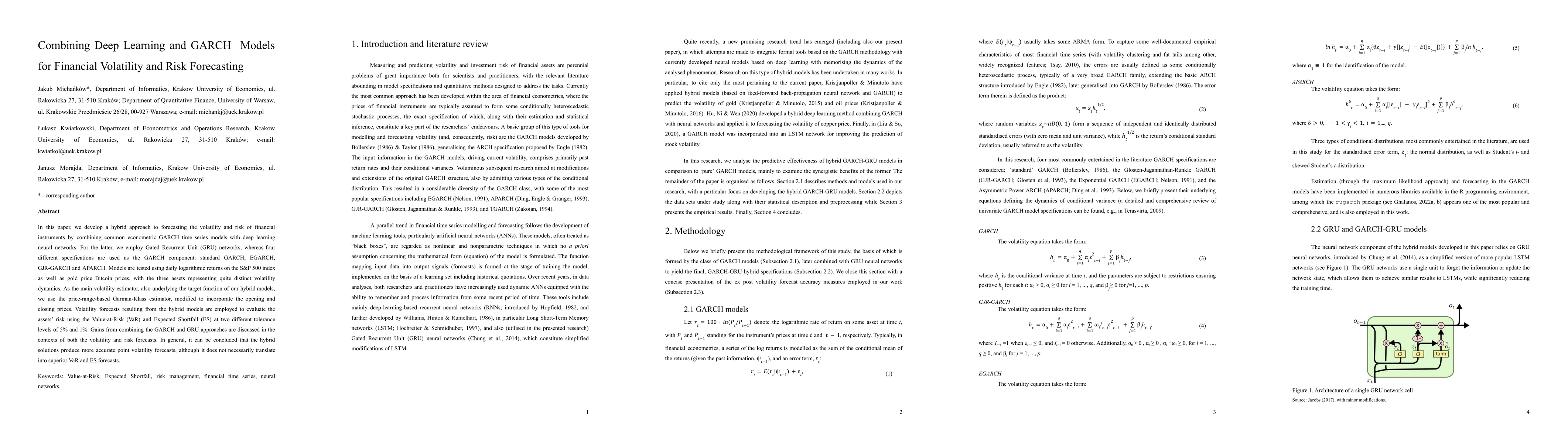

In this paper, we develop a hybrid approach to forecasting the volatility and risk of financial instruments by combining common econometric GARCH time series models with deep learning neural network...