Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper analyzes the stability of optimal policies in the long-run stochastic control framework with an averaged risk-sensitive criterion for discrete-time MDPs on finite state-action space. In p...

The assessment of risk based on historical data faces many challenges, in particular due to the limited amount of available data, lack of stationarity, and heavy tails. While estimation on a short-t...

In this paper we study the problem of Multiplicative Poisson Equation (MPE) bounded solution existence in the generic discrete-time setting. Assuming mixing and boundedness of the risk-reward functi...

In this paper, we investigate the effects of applying generalised (non-exponential) discounting on a long-run impulse control problem for a Feller-Markov process. We show that the optimal value of t...

Controlled discrete time Markov processes are studied first with long run general discounting functional. It is shown that optimal strategies for average reward per unit time problem are also optima...

In the paper adapting Krein Rutman theory we show the existence of solutions to the long run risk sensitive control problem for controlled discrete time Markov processes over locally compact separab...

We consider a long-run impulse control problem for a generic Markov process with a multiplicative reward functional. We construct a solution to the associated Bellman equation and provide a verifica...

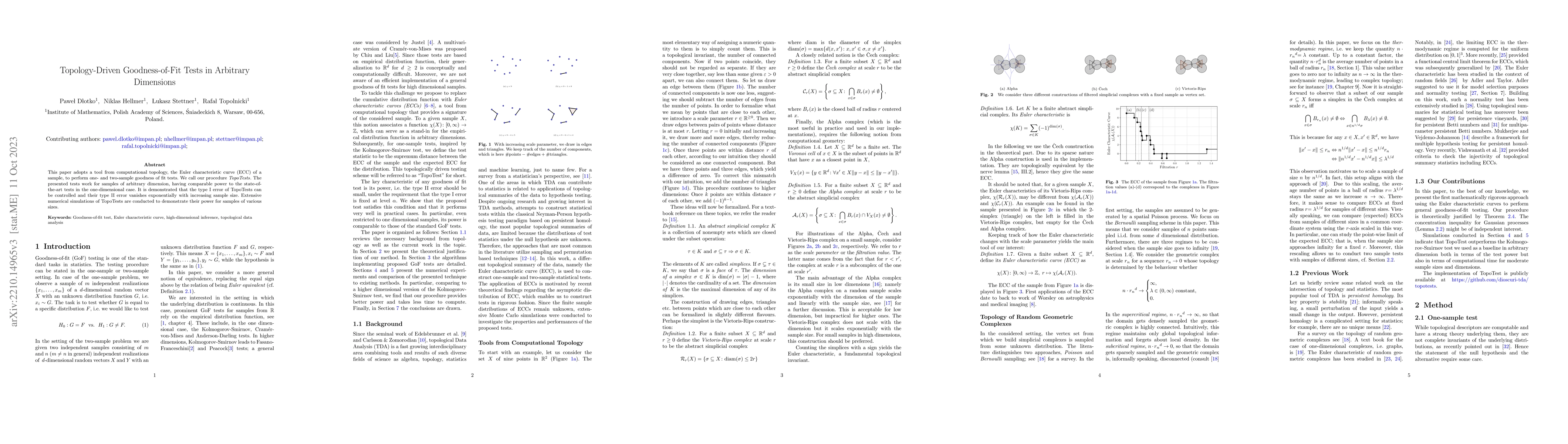

This paper adopts a tool from computational topology, the Euler characteristic curve (ECC) of a sample, to perform one- and two-sample goodness of fit tests. We call our procedure TopoTests. The pre...

In this paper we consider a discrete-time risk sensitive portfolio optimization over a long time horizon with proportional transaction costs. We show that within the log-return i.i.d. framework the ...

In this paper we consider an infinite time horizon risk-sensitive optimal stopping problem for a Feller--Markov process with an unbounded terminal cost function. We show that in the unbounded case a...

In this paper we consider long-run risk sensitive average cost impulse control applied to a continuous-time Feller-Markov process. Using the probabilistic approach, we show how to get a solution to ...

In this paper we consider discrete and continuous time risk sensitive optimal stopping problem. Using suitable properties of the underlying Feller-Markov process we prove continuity of the optimal s...

In this paper long-run risk sensitive optimisation problem is studied with dyadic impulse control applied to continuous-time Feller-Markov process. In contrast to the existing literature, focus is p...

In the paper average reward per unit time and average risk sensitive reward functionals are considered for controlled nonhomogeneous Markov processes. Existence of solutions to suitable Bellman equati...

In the paper discrete time shadow price is constructed for the market with several assets with given bid and ask prices. Shadow price is the price such that the problem of optimal utility from termina...

We study discrete-time Markov Decision Processes (MDPs) on finite state-action spaces and analyze the stability of optimal policies and value functions in the long-run discounted risk-sensitive object...

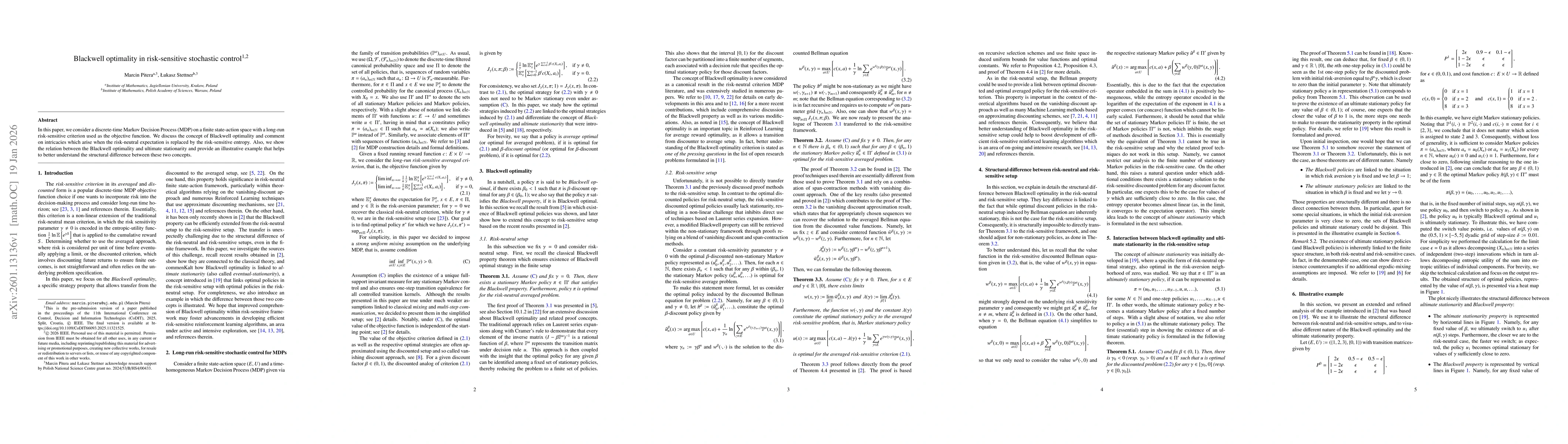

In this paper, we consider a discrete-time Markov Decision Process (MDP) on a finite state-action space with a long-run risk-sensitive criterion used as the objective function. We discuss the concept ...