Academic Profile

Statistics

Similar Authors

Papers on arXiv

Put-call parity holds under risk-neutral pricing, yet enforcement exposes arbitrageurs to path-dependent capital costs. The carry gap-the annualized wedge between option-implied and OIS discount facto...

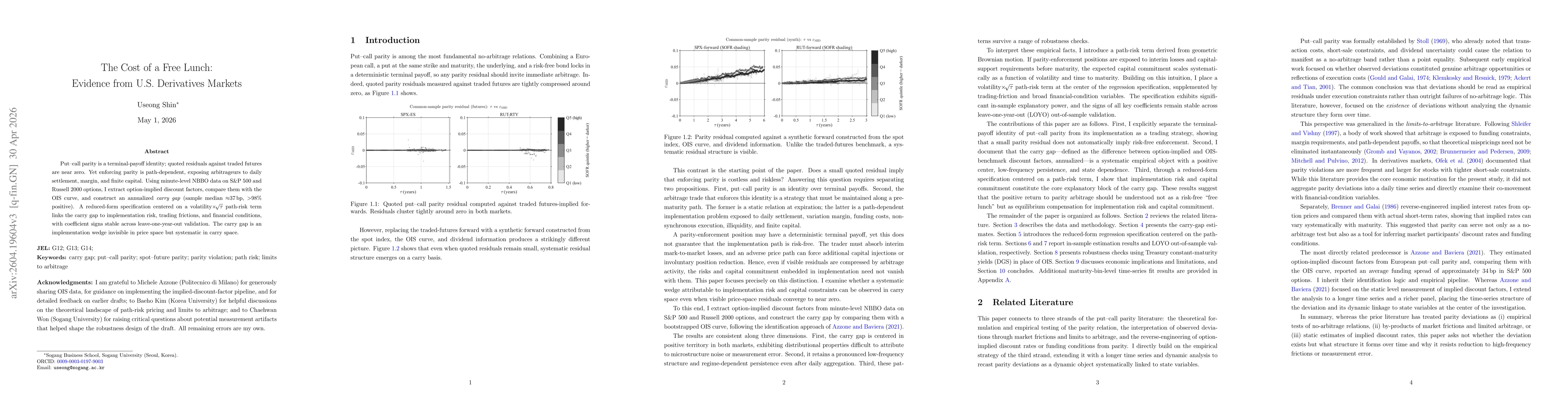

Put-call parity is a terminal-payoff identity; quoted residuals against traded futures are near zero. Yet enforcing parity is path-dependent, exposing arbitrageurs to daily settlement, margin, and fin...

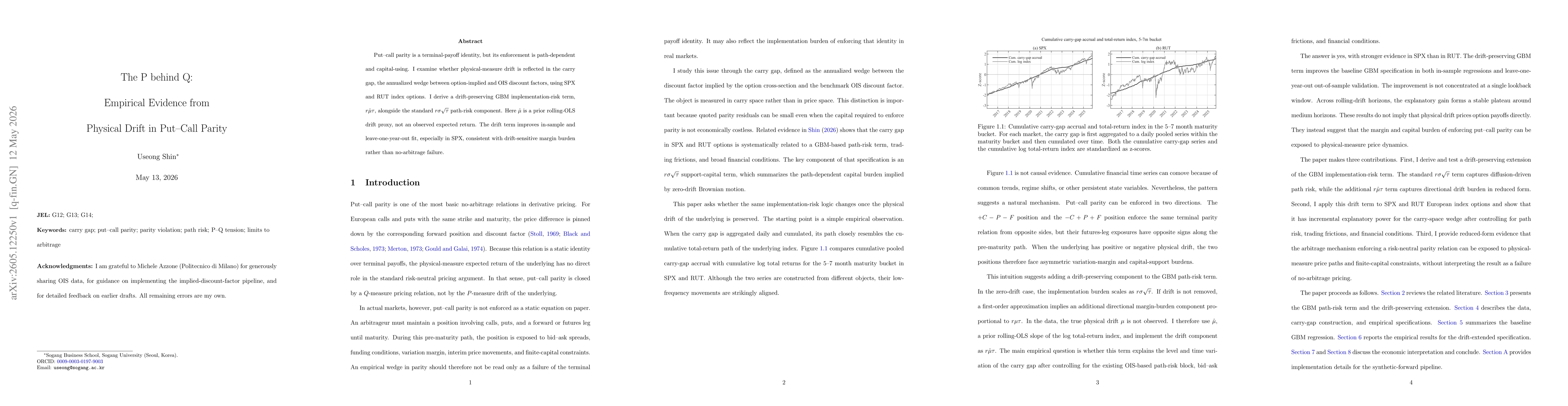

Put-call parity is exact as a terminal-payoff identity, yet its market enforcement is path-dependent and capital-using. This paper examines whether physical-measure drift is reflected in the carry gap...

This paper proposes a public daily-frequency benchmark for post-GFC government-bond CIP deviations. Although CIP deviations are observed daily, the literature lacks a canonical benchmark for daily reg...

Factor-model performance depends not only on the model but also on how test assets are constructed. We form characteristic-unsorted random portfolios from a broad CRSP universe and vary stock selectio...

I ask whether a factor model that prices the aggregate market also prices the market's internal components. I construct a CRSP investible market portfolio and split it into size-ranked body and tail l...

I propose a cap-axis integral diagnostic for factor-model evaluation. Low-dimensional factor models can improve the maximum-Sharpe frontier while leaving zero-alpha violations on economically fixed su...

This paper extends the cap-axis integral diagnostic to general characteristic axes and measures factor-model pricing errors as bridge-alpha curves. A predetermined characteristic order generates prefi...