The P behind Q: Empirical Evidence from Physical Drift in Put-Call Parity

Publication

Metrics

AI Quick Summary

The paper shows that drift in the underlying asset's dynamics, captured by a drift term (μ) estimated from a rolling trend, helps explain the gap between option and OIS-implied discounting (carry gap) for SPX and RUT options. By extending the usual GBM risk term with an extra (rμτ) component, the drift improves model fit and supports the idea that margin and carry constraints—not a breakdown of no-arbitrage—drive parity enforcement.

Paper Preview

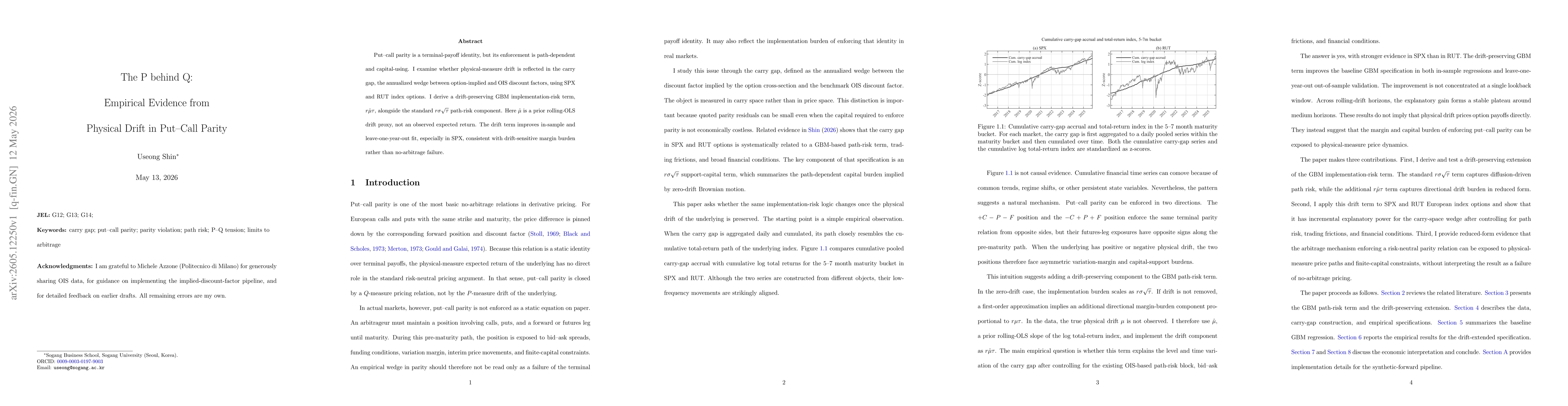

Abstract

Put-call parity is exact as a terminal-payoff identity, yet its market enforcement is path-dependent and capital-using. This paper examines whether physical-measure drift is reflected in the carry gap, defined as the annualized wedge between option-implied and OIS-implied discounting, using SPX and RUT European index options. I derive a drift-preserving extension of the GBM implementation-risk term that adds an (rμτ) component to the standard (rσ\sqrtτ) path-risk component. The drift input (μ) is measured by a lagged rolling-OLS trend proxy and should not be interpreted as an observed expected return. Empirically, the drift term improves both in-sample and leave-one-year-out fit, especially for SPX, consistent with drift-sensitive margin burden in parity enforcement rather than a failure of no-arbitrage.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0