Academic Profile

Statistics

Similar Authors

Papers on arXiv

In nonseparable triangular models with a binary endogenous treatment and a binary instrumental variable, Vuong and Xu (2017) established identification results for individual treatment effects (ITEs...

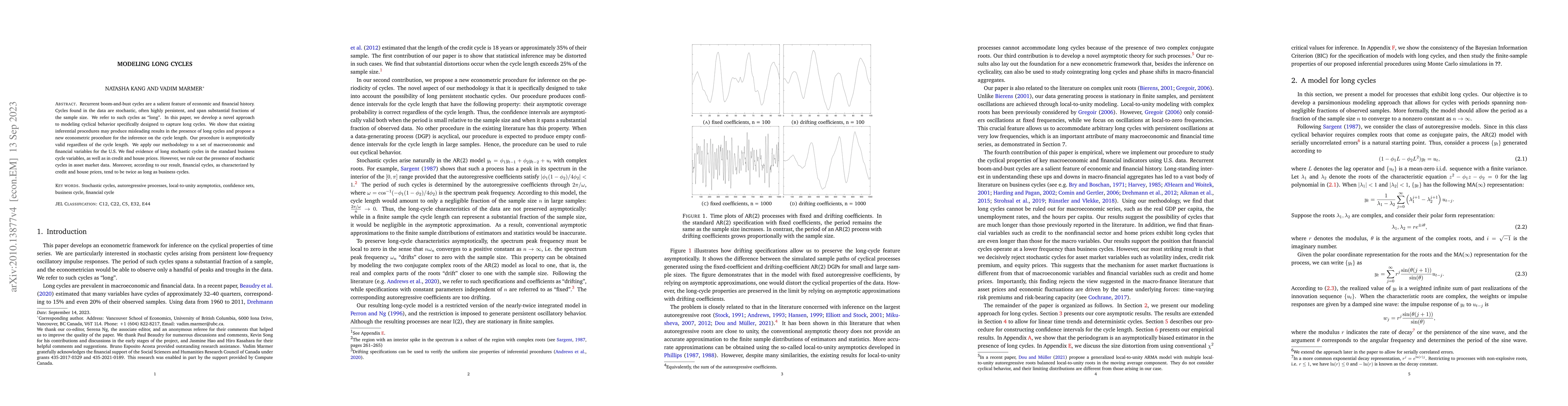

Recurrent boom-and-bust cycles are a salient feature of economic and financial history. Cycles found in the data are stochastic, often highly persistent, and span substantial fractions of the sample...

We propose a new nonparametric estimator for first-price auctions with independent private values that imposes the monotonicity constraint on the estimated inverse bidding strategy. We show that our...

We consider inference on the probability density of valuations in the first-price sealed-bid auctions model within the independent private value paradigm. We show the asymptotic normality of the two...

This paper is concerned with cross-sectional dependence arising because observations are interconnected through an observed network. Following Doukhan and Louhichi (1999), we measure the strength of...

This paper examines bid requirements, where the government may cancel a procurement contract unless two or more bids are received. Using a first-price auction model with endogenous entry, we compare t...

In this paper, we develop inference methods for the distribution of heterogeneous individual treatment effects (ITEs) in the nonseparable triangular model with a binary endogenous treatment and a bina...