Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, a new way to integrate volatility information for estimating value at risk (VaR) and conditional value at risk (CVaR) of a portfolio is suggested. The new method is developed from the...

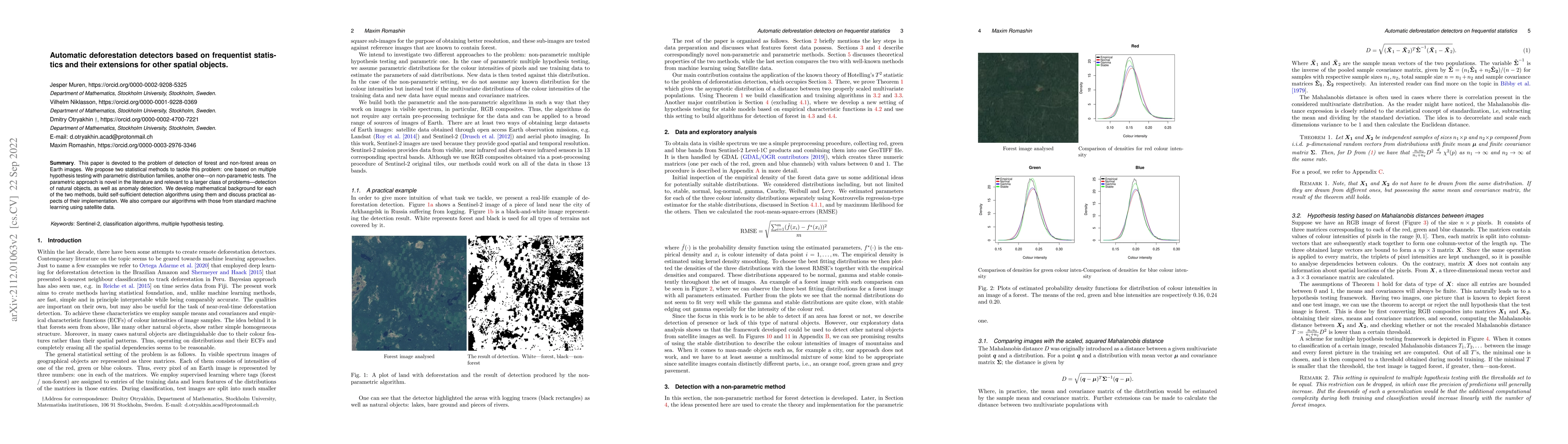

This paper is devoted to the problem of detection of forest and non-forest areas on Earth images. We propose two statistical methods to tackle this problem: one based on multiple hypothesis testing ...

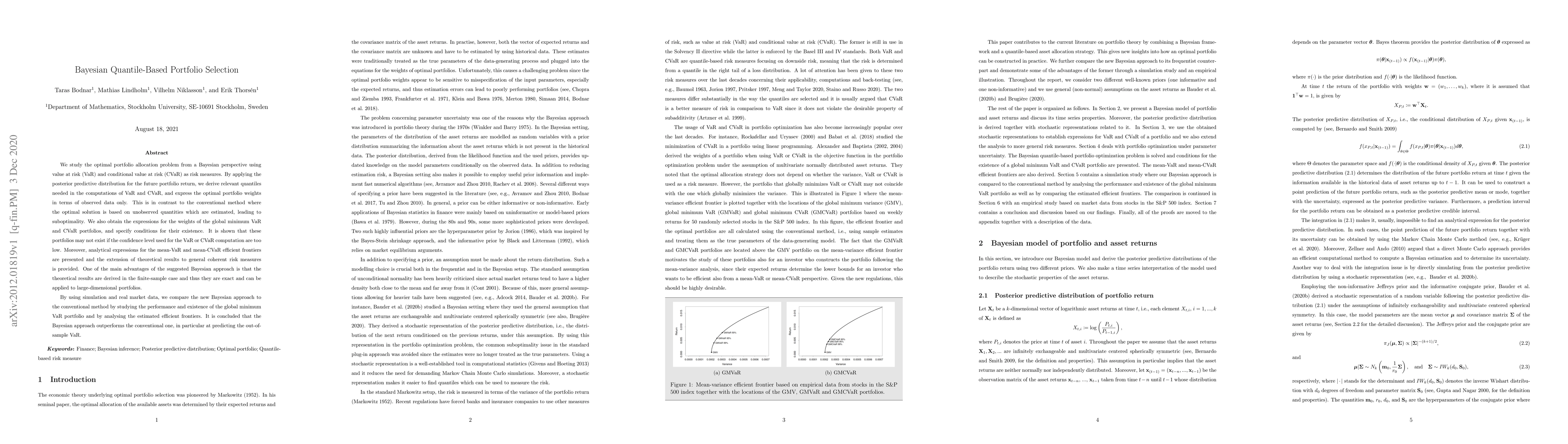

We study the optimal portfolio allocation problem from a Bayesian perspective using value at risk (VaR) and conditional value at risk (CVaR) as risk measures. By applying the posterior predictive di...