Academic Profile

Statistics

Similar Authors

Papers on arXiv

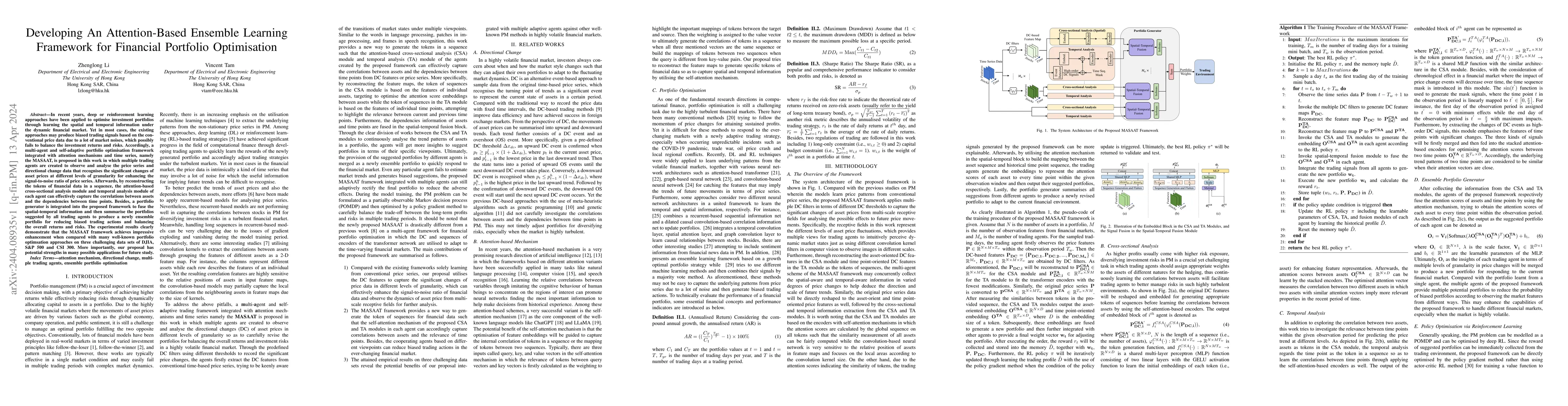

In recent years, deep or reinforcement learning approaches have been applied to optimise investment portfolios through learning the spatial and temporal information under the dynamic financial marke...

Deep or reinforcement learning (RL) approaches have been adapted as reactive agents to quickly learn and respond with new investment strategies for portfolio management under the highly turbulent fi...

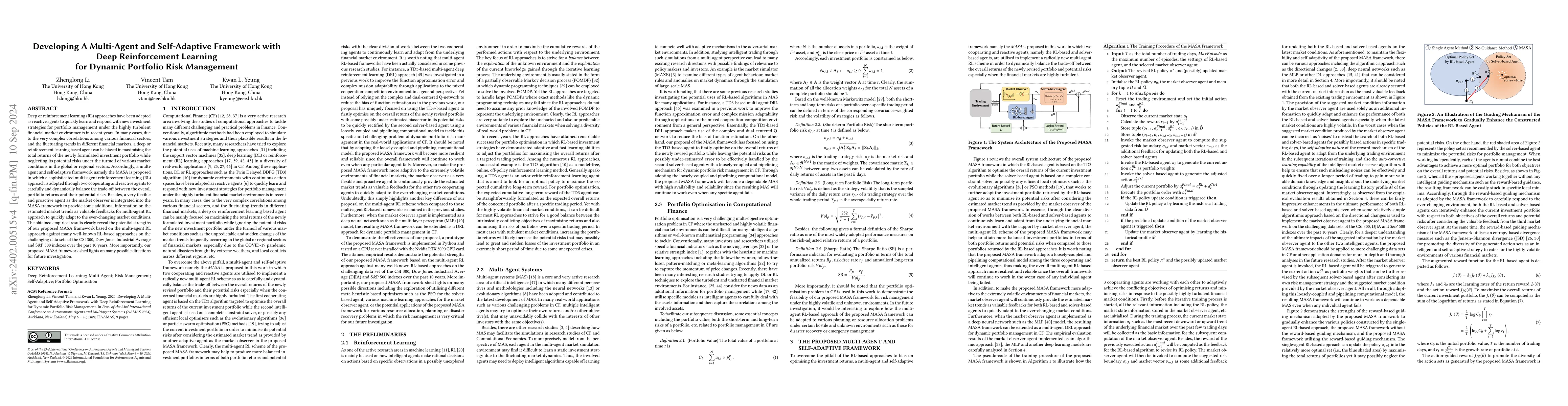

Reinforcement learning (RL) based investment strategies have been widely adopted in portfolio management (PM) in recent years. Nevertheless, most RL-based approaches may often emphasize on pursuing ...

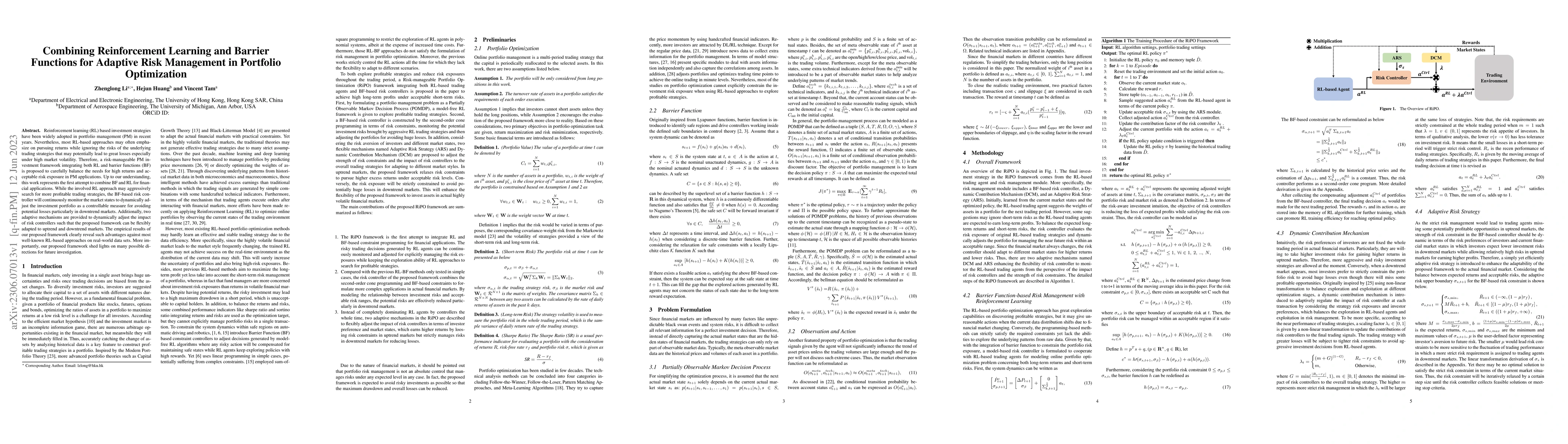

According to the no-free-lunch theorem, there is no single meta-heuristic algorithm that can optimally solve all optimization problems. This motivates many researchers to continuously develop new op...