Academic Profile

Statistics

Similar Authors

Papers on arXiv

Patients with type 2 diabetes need to closely monitor blood sugar levels as their routine diabetes self-management. Although many treatment agents aim to tightly control blood sugar, hypoglycemia of...

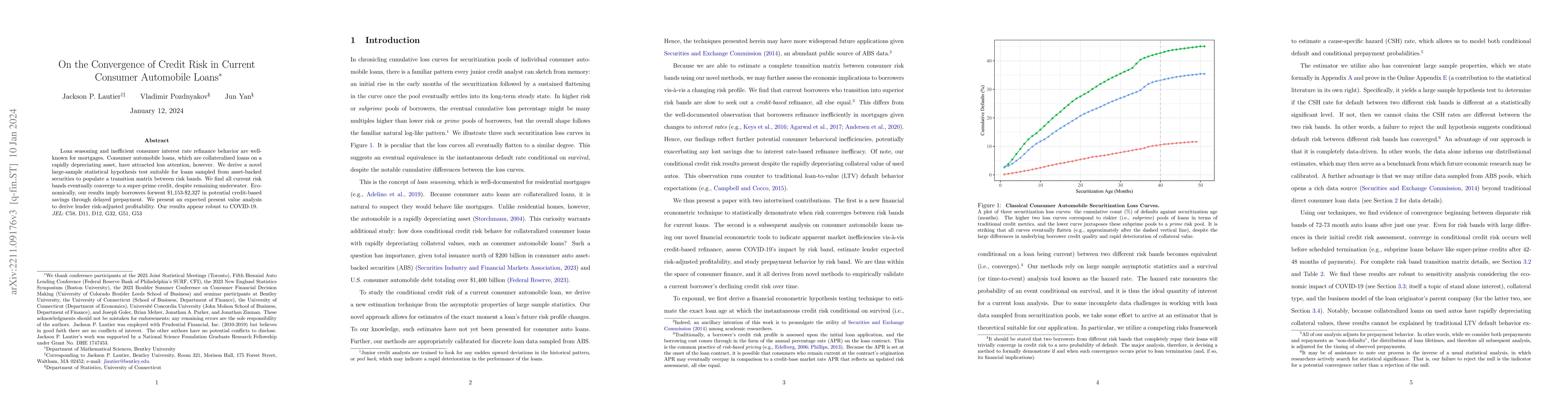

Loan seasoning and inefficient consumer interest rate refinance behavior are well-known for mortgages. Consumer automobile loans, which are collateralized loans on a rapidly depreciating asset, have...

Prudent management of insurance investment portfolios requires competent asset pricing of fixed-income assets with time-to-event contingent cash flows, such as consumer asset-backed securities (ABS)...

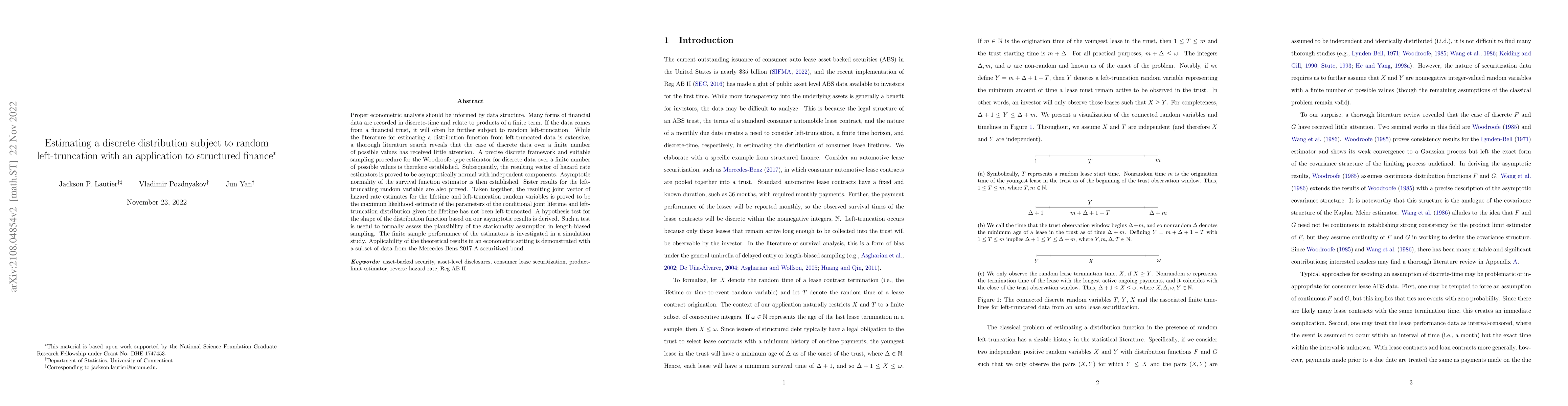

Proper econometric analysis should be informed by data structure. Many forms of financial data are recorded in discrete-time and relate to products of a finite term. If the data comes from a financi...

The need to model a Markov renewal on-off process with multiple off-states arise in many applications such as economics, physics, and engineering. Characterization of the occupation time of one spec...

Several numerical evaluations of the density and distribution of convolution of independent gamma variables are compared in their accuracy and speed. In application to renewal processes, an efficien...

Brownian motion whose infinitesimal variance changes according to a three-state continuous time Markov Chain is studied. This Markov Chain can be viewed as a telegraph process with one on state and ...

In his 1996 paper, Talagrand highlighted that the Law of Large Numbers (LLN) for independent random variables can be viewed as a geometric property of multidimensional product spaces. This phenomenon ...

The gambler's ruin problem for correlated random walks, both with and without delays, is addressed by Optional Stopping Theorem for martingales.

Assume that letters (from a finite alphabet) in a text form a Markov chain. We track two distinct words, $U$ and $D$. A gambler gains 1 point for each occurrence of $U$ (including overlapping occurren...

Stem cells, through their ability to produce daughter stem cells and differentiate into specialized cells, are essential in the growth, maintenance, and repair of biological tissues. Understanding the...