Academic Profile

Statistics

Similar Authors

Papers on arXiv

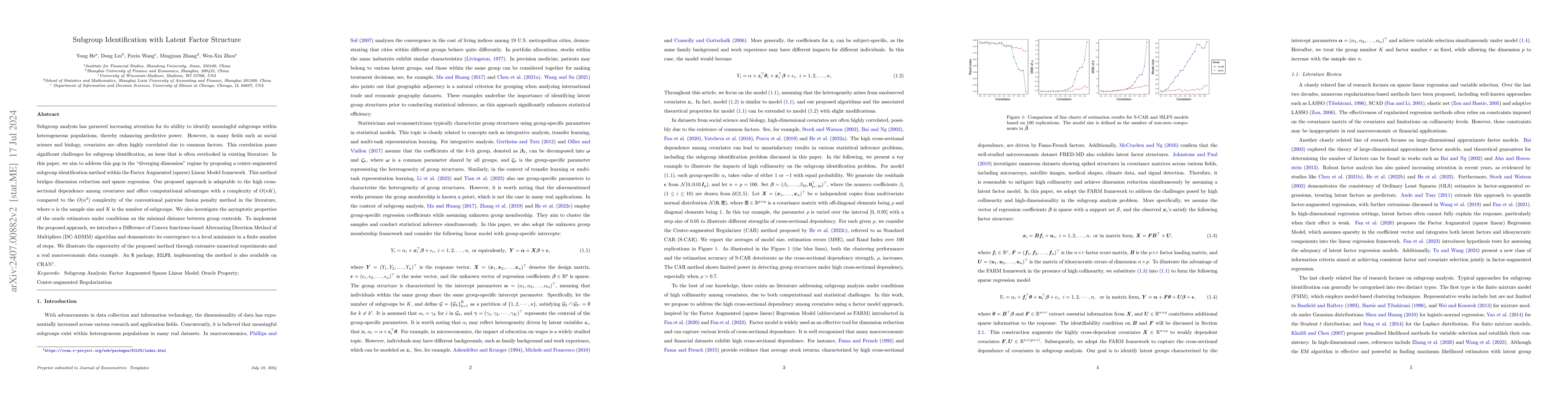

Subgroup analysis has attracted growing attention due to its ability to identify meaningful subgroups from a heterogeneous population and thereby improving predictive power. However, in many scenari...

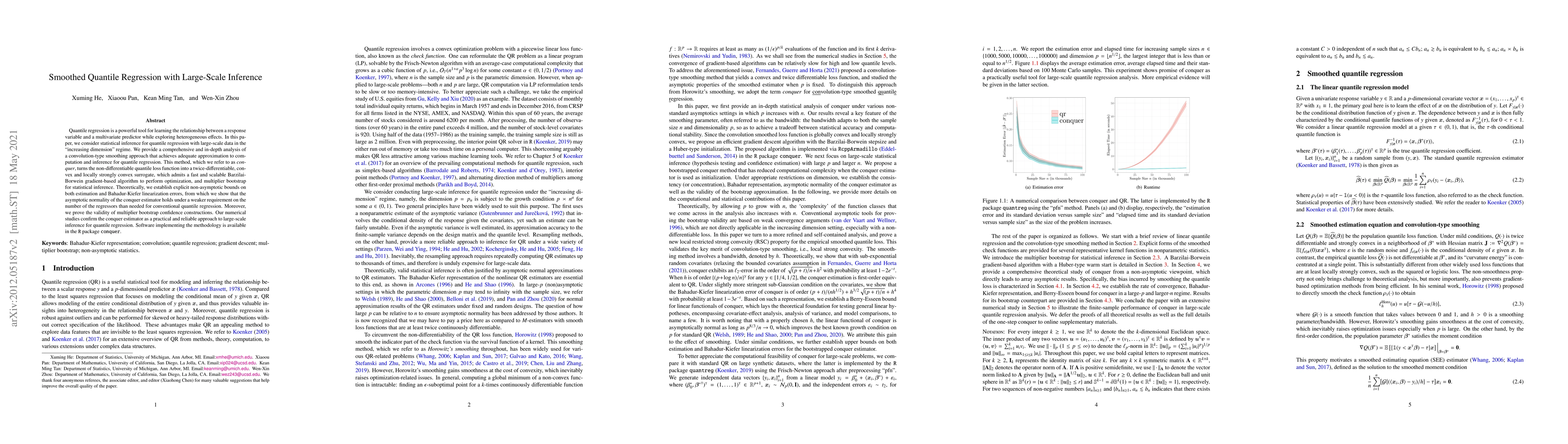

This paper addresses the challenge of integrating sequentially arriving data within the quantile regression framework, where the number of features is allowed to grow with the number of observations...

The expected shortfall is defined as the average over the tail below (or above) a certain quantile of a probability distribution. The expected shortfall regression provides powerful tools for learni...

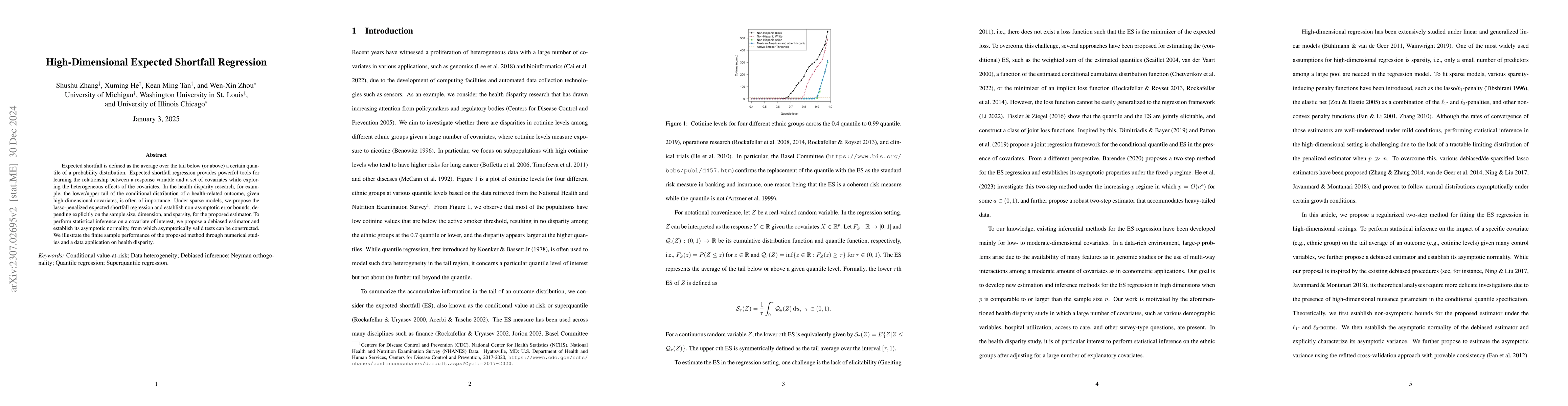

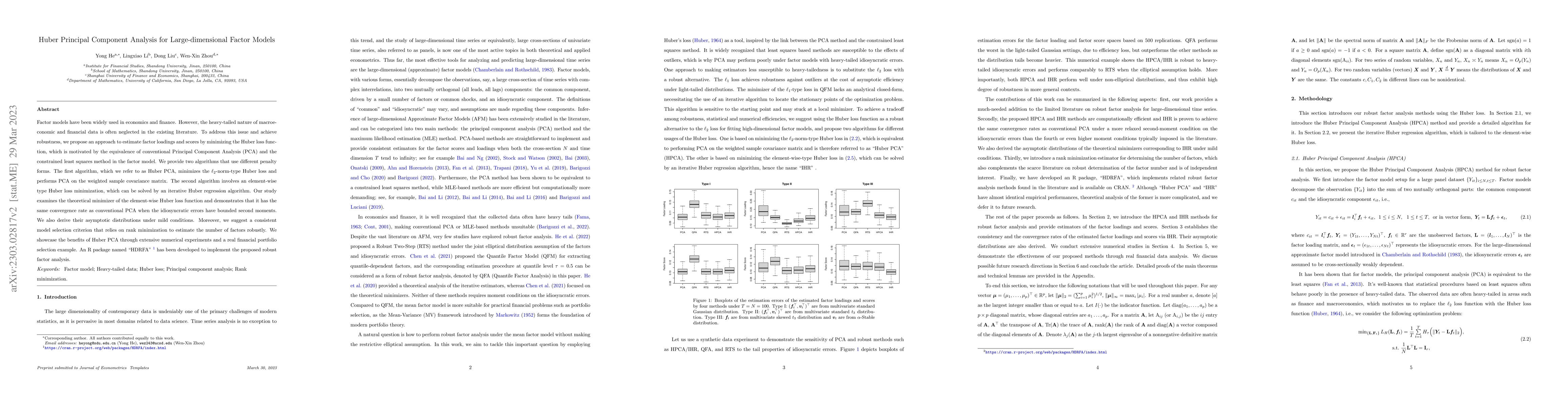

Factor models have been widely used in economics and finance. However, the heavy-tailed nature of macroeconomic and financial data is often neglected in the existing literature. To address this issu...

The matrix factor model has drawn growing attention for its advantage in achieving two-directional dimension reduction simultaneously for matrix-structured observations. In this paper, we propose a ...

Expected Shortfall (ES), also known as superquantile or Conditional Value-at-Risk, has been recognized as an important measure in risk analysis and stochastic optimization, and is also finding appli...

High-dimensional data can often display heterogeneity due to heteroscedastic variance or inhomogeneous covariate effects. Penalized quantile and expectile regression methods offer useful tools to de...

Censored quantile regression (CQR) has become a valuable tool to study the heterogeneous association between a possibly censored outcome and a set of covariates, yet computation and statistical infe...

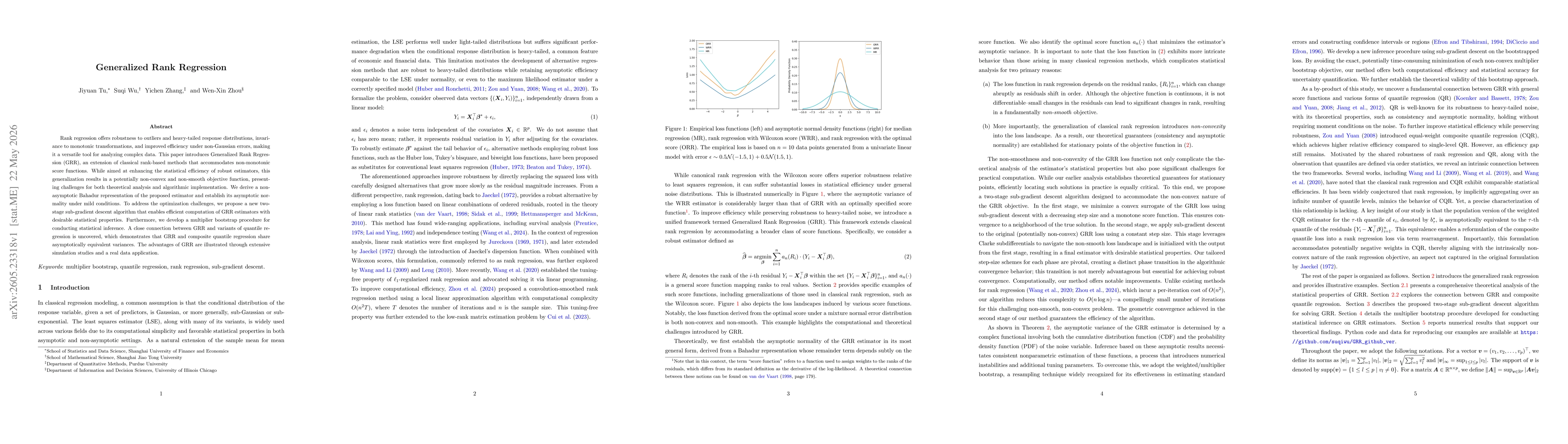

The composite quantile regression (CQR) was introduced by Zou and Yuan [Ann. Statist. 36 (2008) 1108--1126] as a robust regression method for linear models with heavy-tailed errors while achieving h...

In this article, we first propose generalized row/column matrix Kendall's tau for matrix-variate observations that are ubiquitous in areas such as finance and medical imaging. For a random matrix fo...

Penalized quantile regression (QR) is widely used for studying the relationship between a response variable and a set of predictors under data heterogeneity in high-dimensional settings. Compared to...

This paper investigates the stability of deep ReLU neural networks for nonparametric regression under the assumption that the noise has only a finite p-th moment. We unveil how the optimal rate of c...

We address the problem of how to achieve optimal inference in distributed quantile regression without stringent scaling conditions. This is challenging due to the non-smooth nature of the quantile r...

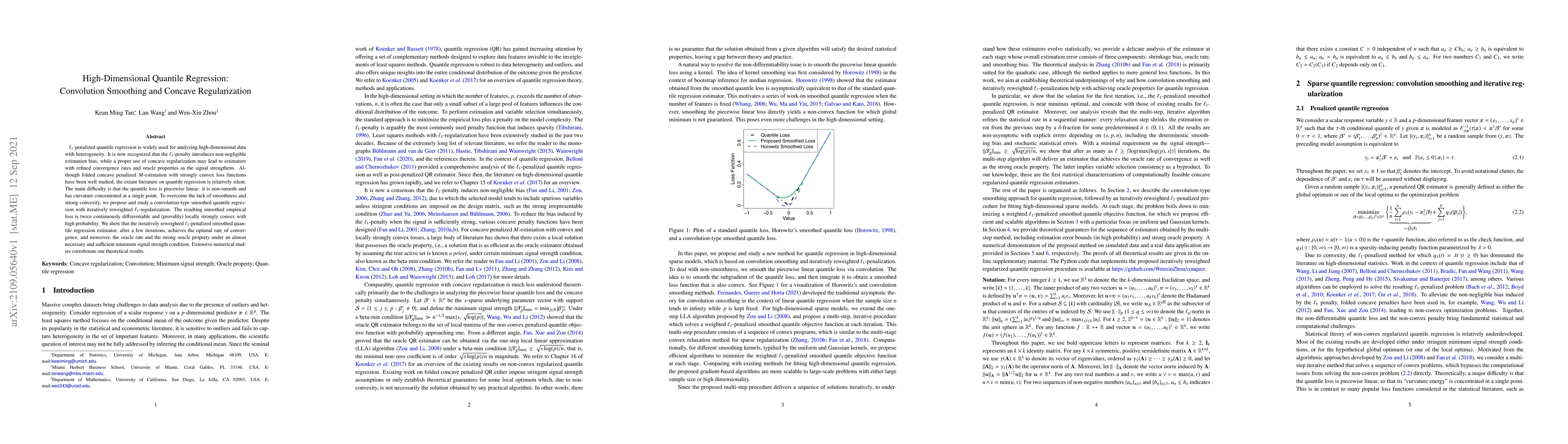

$\ell_1$-penalized quantile regression is widely used for analyzing high-dimensional data with heterogeneity. It is now recognized that the $\ell_1$-penalty introduces non-negligible estimation bias...

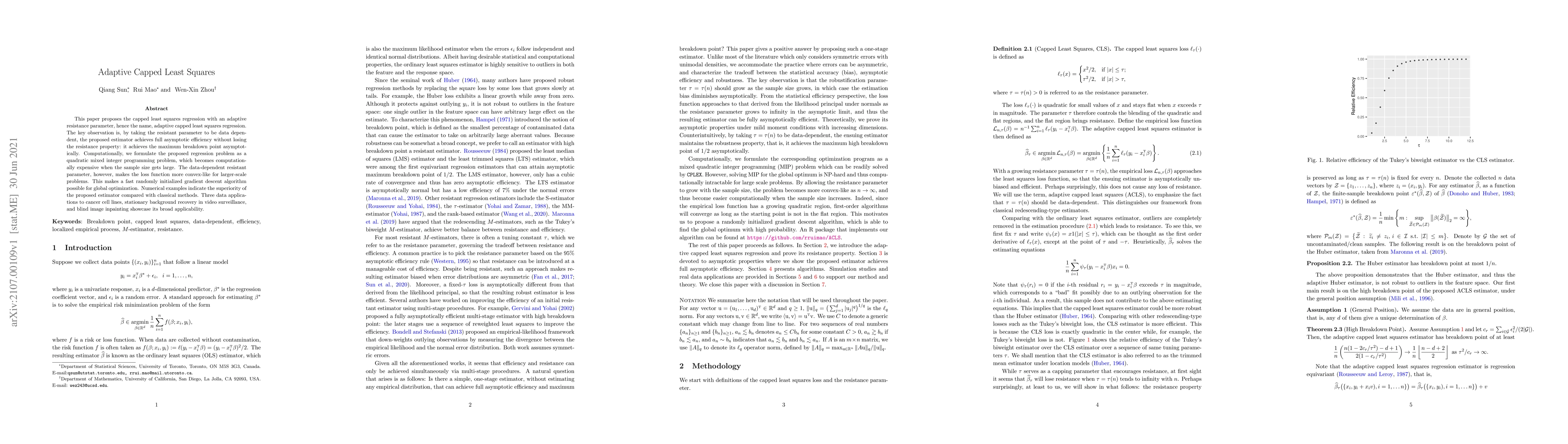

This paper proposes the capped least squares regression with an adaptive resistance parameter, hence the name, adaptive capped least squares regression. The key observation is, by taking the resista...

Quantile regression is a powerful tool for learning the relationship between a response variable and a multivariate predictor while exploring heterogeneous effects. In this paper, we consider statis...

This paper investigates tradeoffs among optimization errors, statistical rates of convergence and the effect of heavy-tailed errors for high-dimensional robust regression with nonconvex regularizati...

Expected shortfall (ES), also known as conditional value-at-risk, is a widely recognized risk measure that complements value-at-risk by capturing tail-related risks more effectively. Compared with qua...

This work investigates the performance of the final iterate produced by stochastic gradient descent (SGD) under temporally dependent data. We consider two complementary sources of dependence: $(i)$ ma...

Understanding the structural mechanisms of multi-layer networks is essential for analyzing complex systems characterized by multiple interacting layers. This work studies the problem of estimating con...

While the traditional goal of statistics is to infer population parameters, modern practice increasingly demands protection of individual privacy. One way to address this need is to adapt classical st...

Rank regression offers robustness to outliers and heavy-tailed response distributions, invariance to monotonic transformations, and improved efficiency under non-Gaussian errors, making it a versatile...