2

arXiv Papers

2

Total Publications

Profile

Academic Profile

Metrics

Statistics

2

arXiv Papers

2

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Quantum Computation for Pricing Caps using the LIBOR Market Model

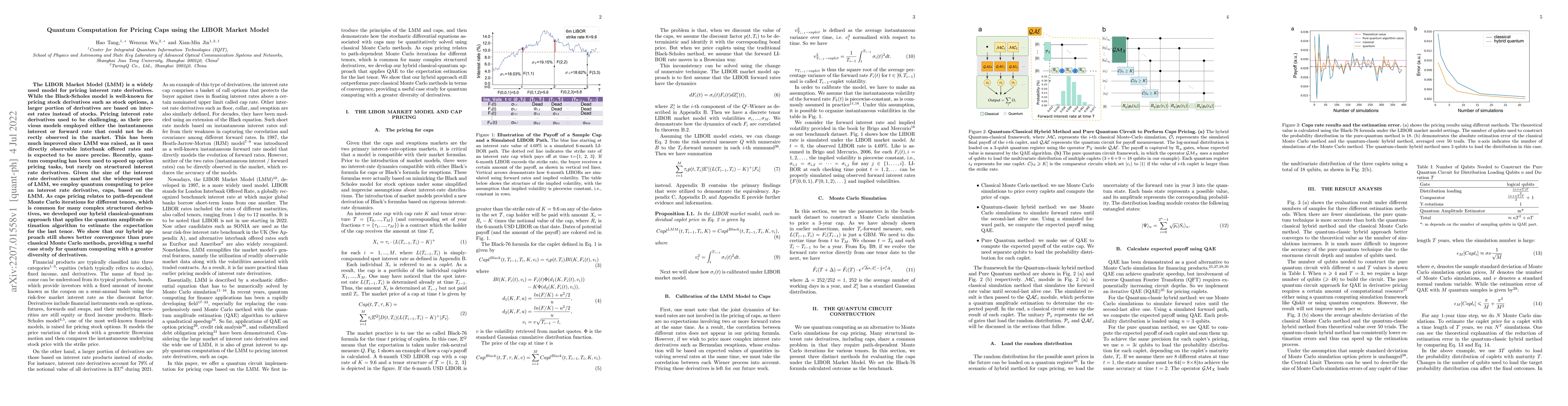

The LIBOR Market Model (LMM) is a widely used model for pricing interest rate derivatives. While the Black-Scholes model is well-known for pricing stock derivatives such as stock options, a larger p...

arXiv

Tool-Augmented Policy Optimization: Synergizing Reasoning and Adaptive

Tool Use with Reinforcement Learning

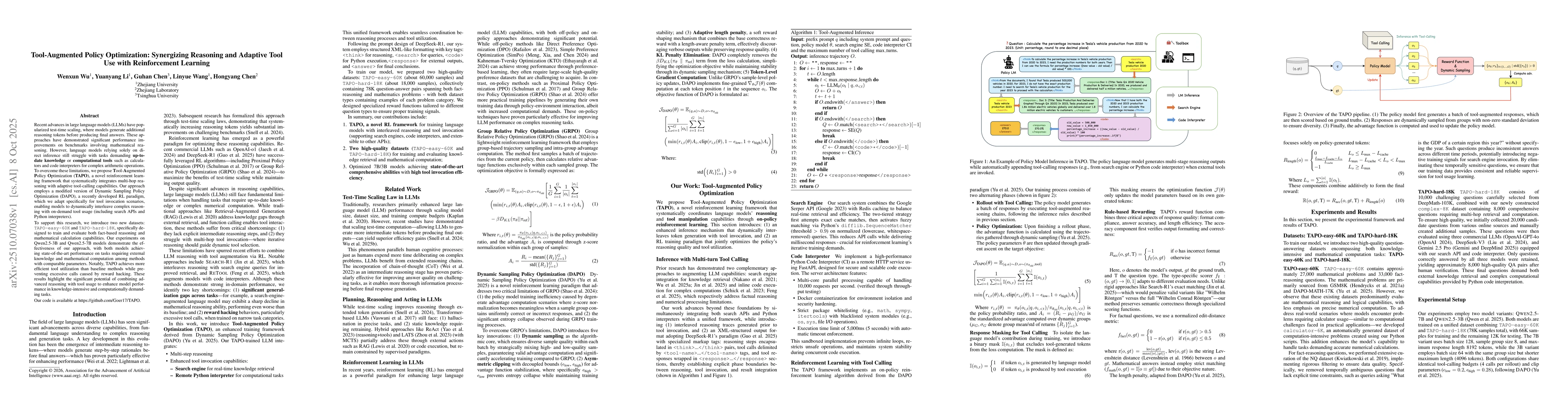

Recent advances in large language models (LLMs) have popularized test-time scaling, where models generate additional reasoning tokens before producing final answers. These approaches have demonstrated...