Academic Profile

Statistics

Similar Authors

Papers on arXiv

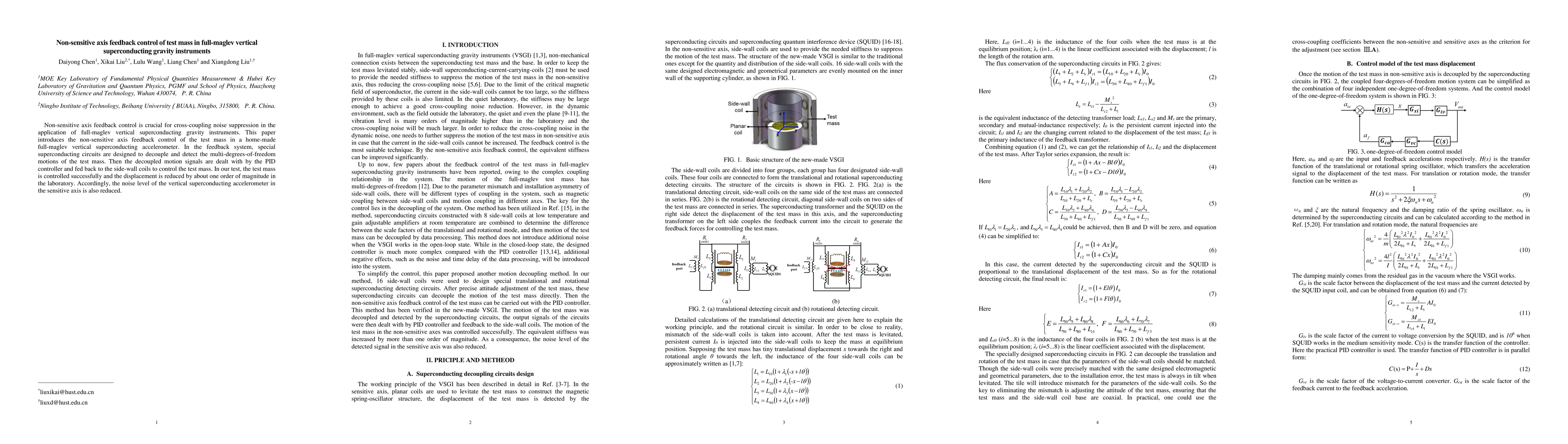

Non-sensitive axis feedback control is crucial for cross-coupling noise suppression in the application of full-maglev vertical superconducting gravity instruments. This paper introduces the non-sens...

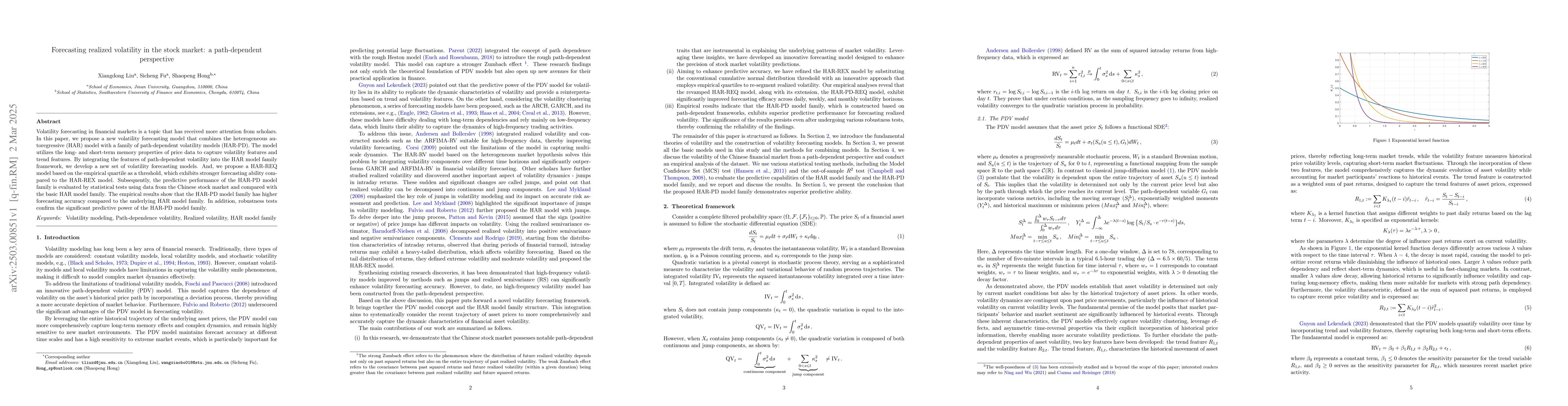

Volatility forecasting in financial markets is a topic that has received more attention from scholars. In this paper, we propose a new volatility forecasting model that combines the heterogeneous auto...

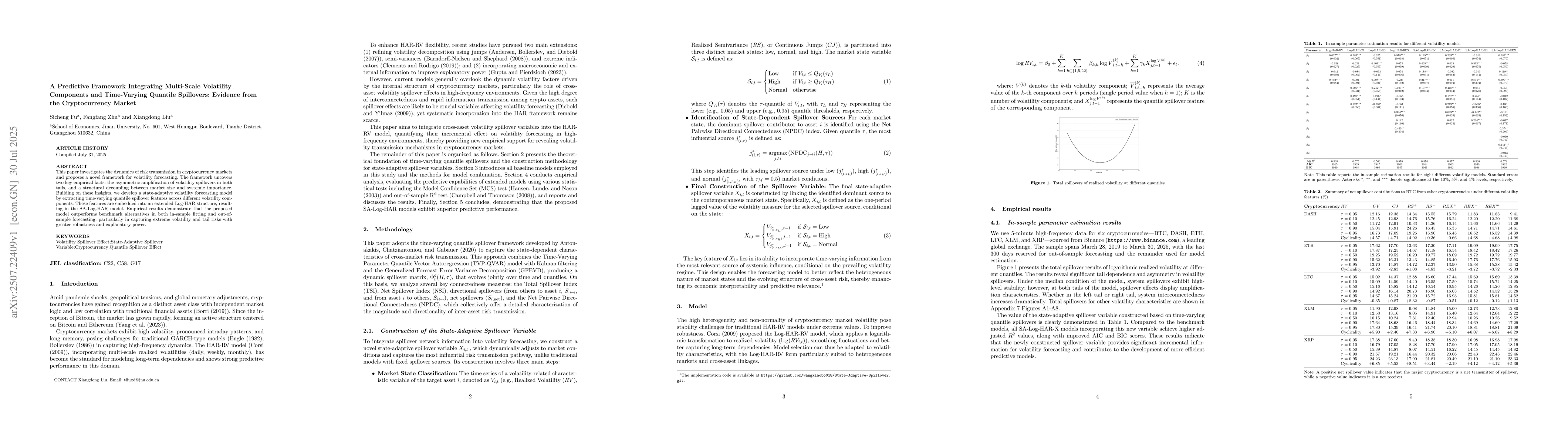

This paper investigates the dynamics of risk transmission in cryptocurrency markets and proposes a novel framework for volatility forecasting. The framework uncovers two key empirical facts: the asymm...

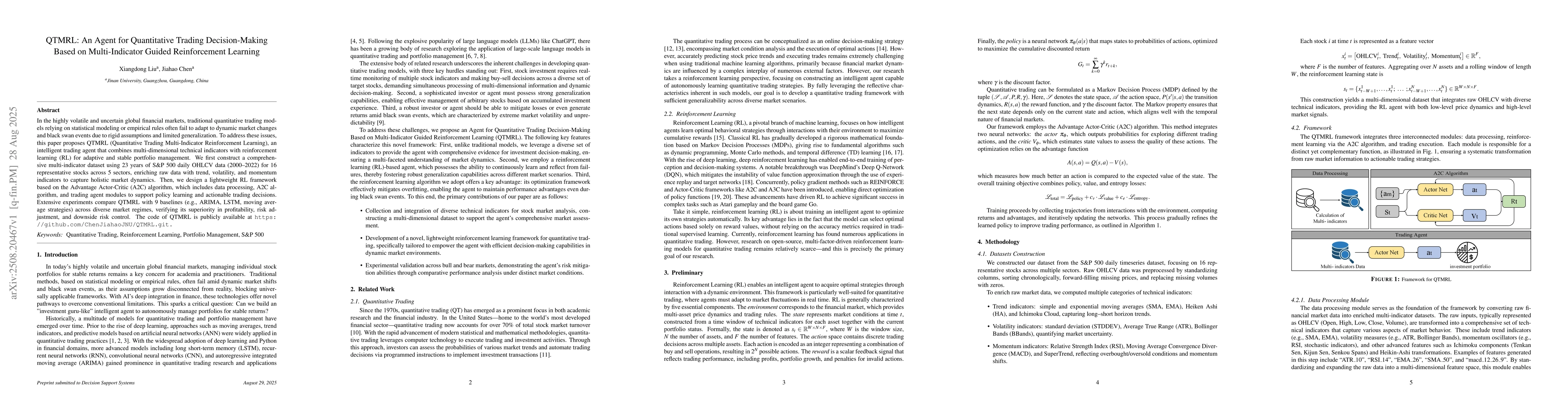

In the highly volatile and uncertain global financial markets, traditional quantitative trading models relying on statistical modeling or empirical rules often fail to adapt to dynamic market changes ...