Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper proposes a novel methodology for the online detection of changepoints in the factor structure of large matrix time series. Our approach is based on the well-known fact that, in the presen...

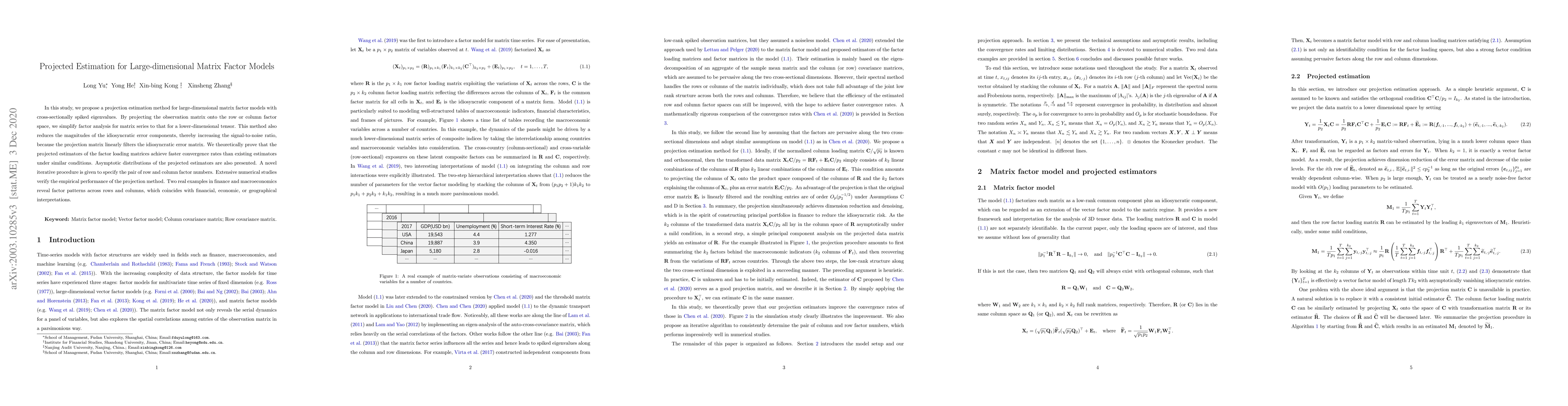

This paper investigates the issue of determining the dimensions of row and column factor spaces in matrix-valued data. Exploiting the eigen-gap in the spectrum of sample second moment matrices of th...

In this study, we propose a projection estimation method for large-dimensional matrix factor models with cross-sectionally spiked eigenvalues. By projecting the observation matrix onto the row or co...