Xin-Bing Kong

3 papers on arXiv

Academic Profile

Statistics

Similar Authors

Papers on arXiv

Robust Statistical Inference for Large-dimensional Matrix-valued Time Series via Iterative Huber Regression

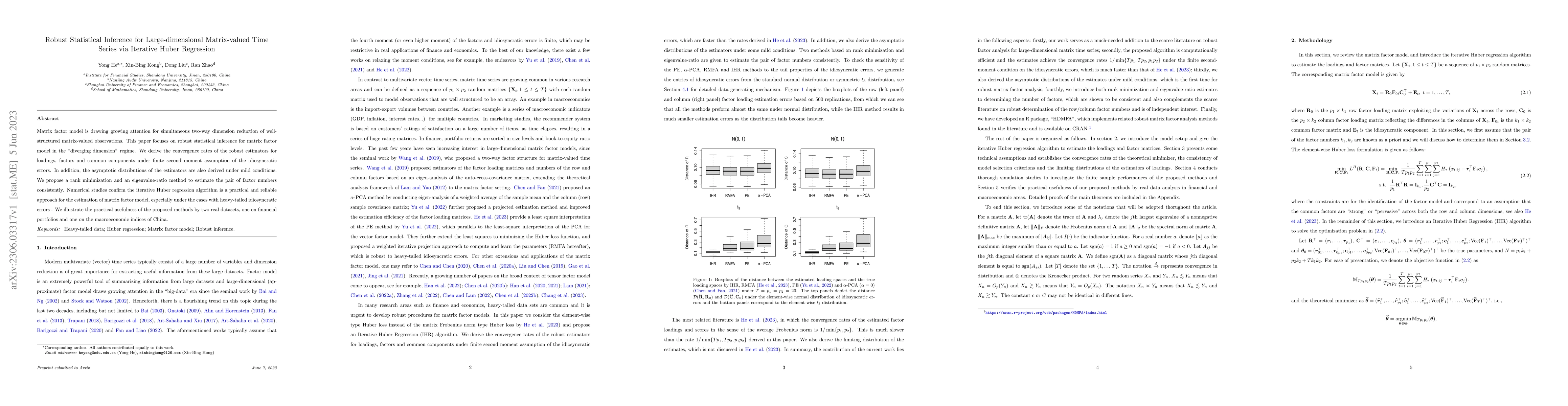

Matrix factor model is drawing growing attention for simultaneous two-way dimension reduction of well-structured matrix-valued observations. This paper focuses on robust statistical inference for ma...

Matrix Quantile Factor Model

This paper introduces a matrix quantile factor model for matrix-valued data with a low-rank structure. We estimate the row and column factor spaces via minimizing the empirical check loss function o...

Staleness Factor Model and Volatility Estimation

In this paper, we introduce a novel nonstationary price staleness factor model allowing for market friction pervasive across assets and possible input covariates. With large panel high-frequency data,...