Robust Statistical Inference for Large-dimensional Matrix-valued Time Series via Iterative Huber Regression

Publication

Metrics

AI Quick Summary

This paper develops robust statistical inference methods for matrix factor models in high-dimensional settings, proposing iterative Huber regression for effective estimation. It demonstrates the practical utility of the approach through numerical studies and real-world applications in finance and macroeconomics.

Paper Preview

Abstract

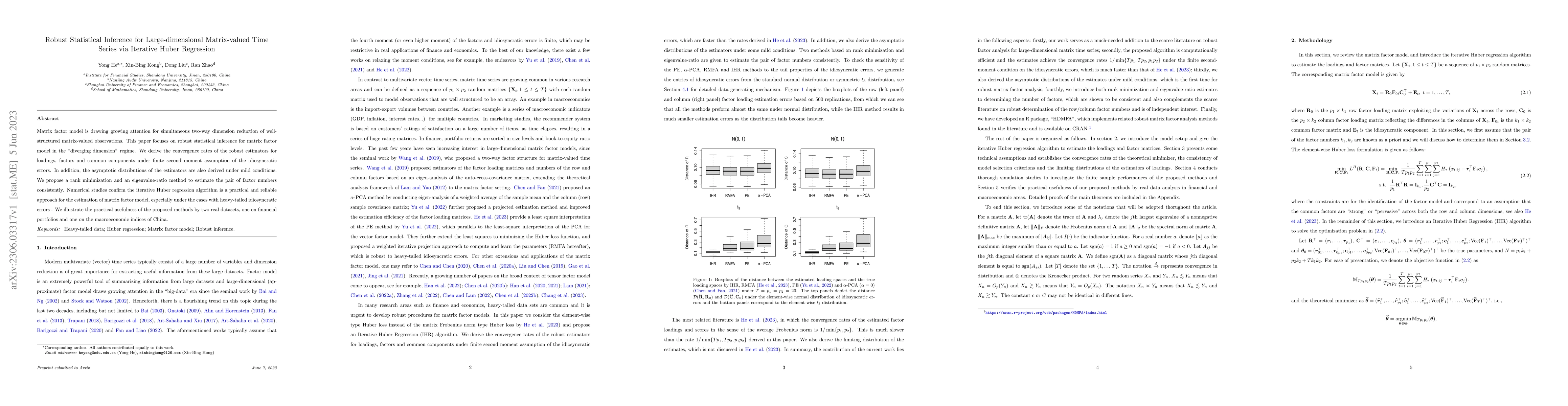

Matrix factor model is drawing growing attention for simultaneous two-way dimension reduction of well-structured matrix-valued observations. This paper focuses on robust statistical inference for matrix factor model in the ``diverging dimension" regime. We derive the convergence rates of the robust estimators for loadings, factors and common components under finite second moment assumption of the idiosyncratic errors. In addition, the asymptotic distributions of the estimators are also derived under mild conditions. We propose a rank minimization and an eigenvalue-ratio method to estimate the pair of factor numbers consistently. Numerical studies confirm the iterative Huber regression algorithm is a practical and reliable approach for the estimation of matrix factor model, especially under the cases with heavy-tailed idiosyncratic errors . We illustrate the practical usefulness of the proposed methods by two real datasets, one on financial portfolios and one on the macroeconomic indices of China.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0