Academic Profile

Statistics

Similar Authors

Papers on arXiv

The knockoffs is a recently proposed powerful framework that effectively controls the false discovery rate (FDR) for variable selection. However, none of the existing knockoff solutions are directly...

We propose a two-step procedure to model and predict high-dimensional functional time series, where the number of function-valued time series $p$ is large in relation to the length of time series $n...

This paper addresses the fundamental task of estimating covariance matrix functions for high-dimensional functional data/functional time series. We consider two functional factor structures encompas...

Nonparametric estimation of the mean and covariance functions is ubiquitous in functional data analysis and local linear smoothing techniques are most frequently used. Zhang and Wang (2016) explored...

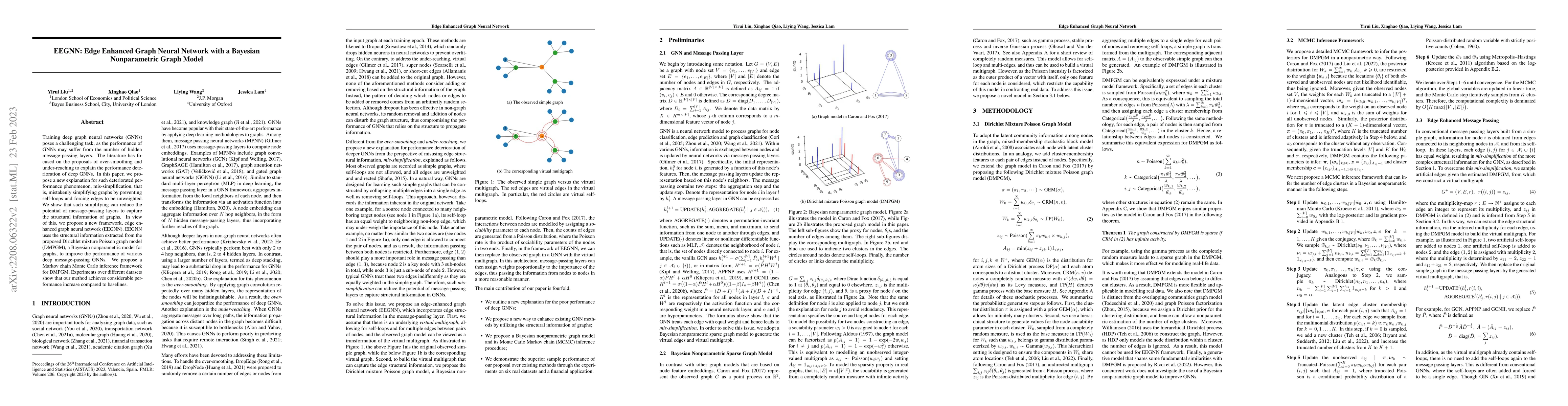

Training deep graph neural networks (GNNs) poses a challenging task, as the performance of GNNs may suffer from the number of hidden message-passing layers. The literature has focused on the proposa...

Covariance function estimation is a fundamental task in multivariate functional data analysis and arises in many applications. In this paper, we consider estimating sparse covariance functions for h...

Many economic and scientific problems involve the analysis of high-dimensional functional time series, where the number of functional variables ($p$) diverges as the number of serially dependent obs...

Many scientific and economic applications involve the statistical learning of high-dimensional functional time series, where the number of functional variables is comparable to, or even greater than...

Statistical analysis of high-dimensional functional times series arises in various applications. Under this scenario, in addition to the intrinsic infinite-dimensionality of functional data, the num...

Current variational inference methods for hierarchical Bayesian nonparametric models can neither characterize the correlation structure among latent variables due to the mean-field setting, nor infe...

Functional linear regression is an important topic in functional data analysis. It is commonly assumed that samples of the functional predictor are independent realizations of an underlying stochast...

The estimation of functional networks through functional covariance and graphical models have recently attracted increasing attention in settings with high dimensional functional data, where the numbe...

This paper studies the covariance matrix estimation for high-dimensional time series within a new framework that combines low-rank factor and latent variable-specific cluster structures. The popular m...

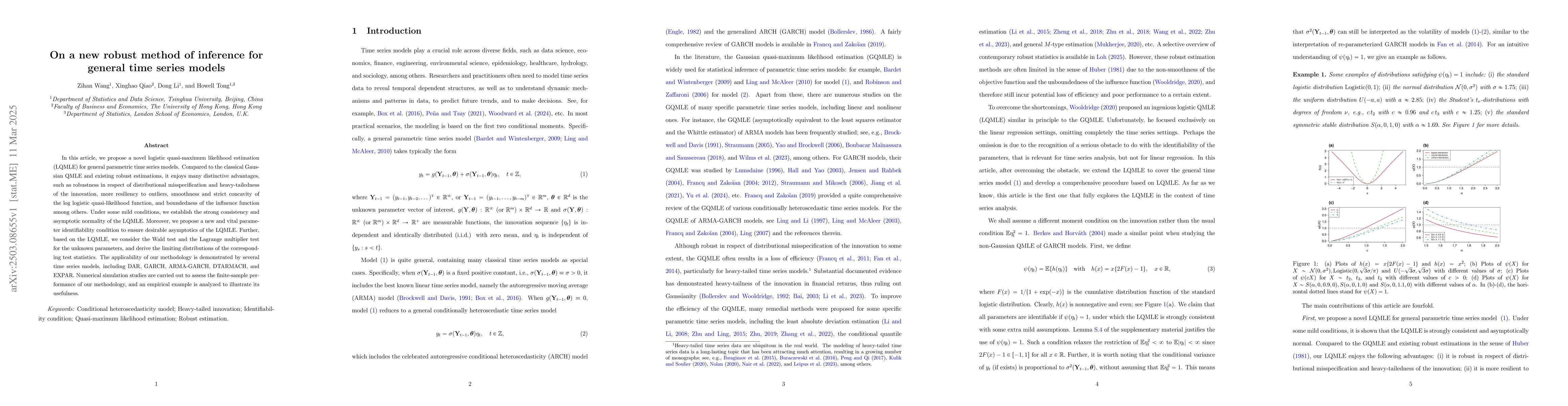

In this article, we propose a novel logistic quasi-maximum likelihood estimation (LQMLE) for general parametric time series models. Compared to the classical Gaussian QMLE and existing robust estimati...

The factor modeling for high-dimensional time series is powerful in discovering latent common components for dimension reduction and information extraction. Most available estimation methods can be di...

Empirical likelihood serves as a powerful tool for constructing confidence intervals in nonparametric regression and regression discontinuity designs (RDD). The original empirical likelihood framework...

Second-order characteristics including covariance and spectral density functions are fundamentally important for both statistical applications and theoretical analysis in functional time series. In th...

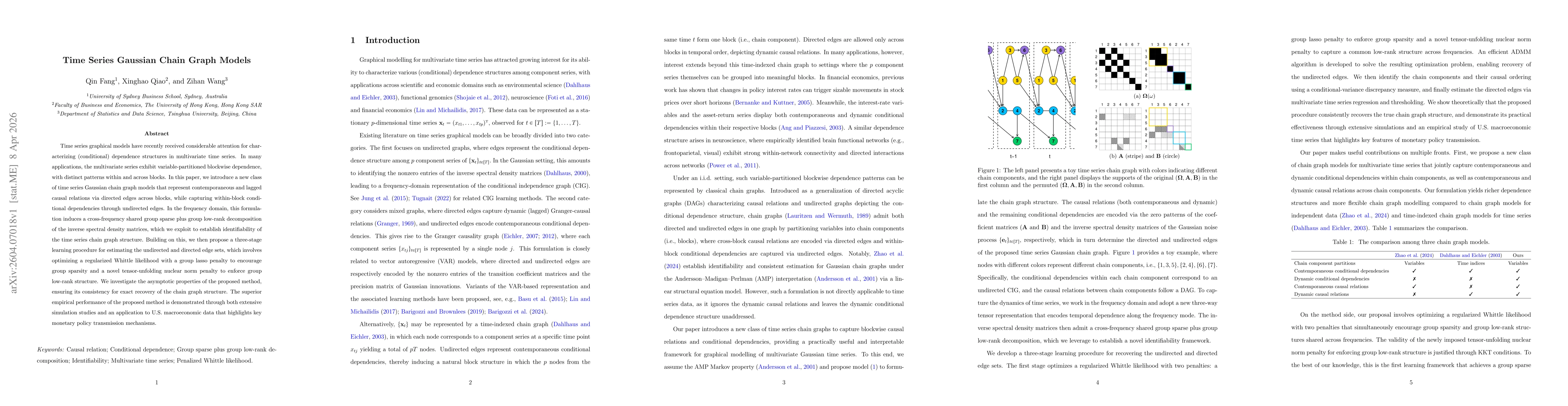

Time series graphical models have recently received considerable attention for characterizing (conditional) dependence structures in multivariate time series. In many applications, the multivariate se...