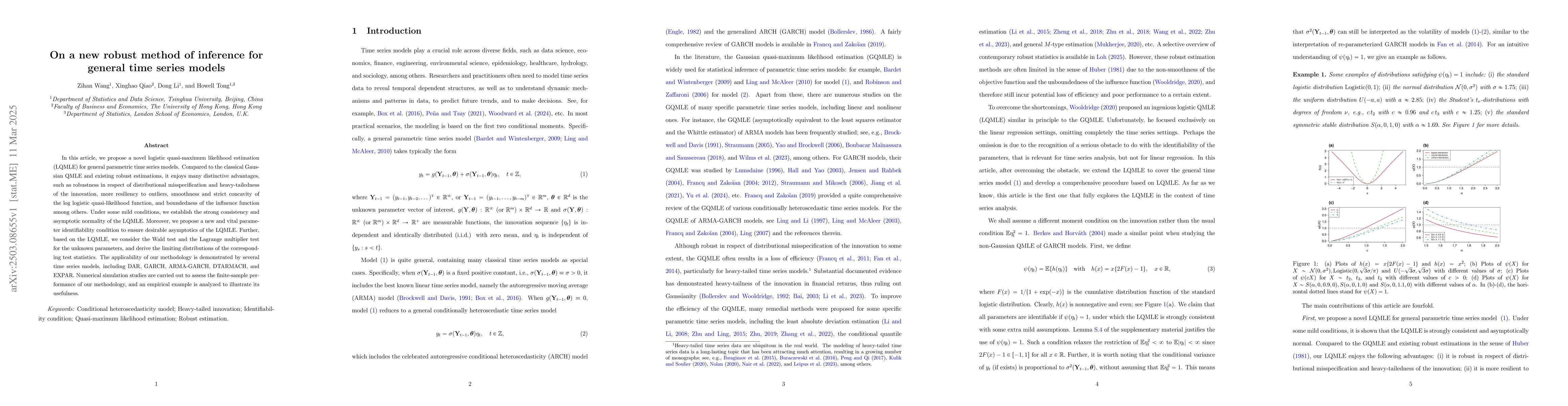

In this article, we propose a novel logistic quasi-maximum likelihood

estimation (LQMLE) for general parametric time series models. Compared to the

classical Gaussian QMLE and existing robust estimations, it enjoys many

distinctive advantages, such as robustness in respect of distributional

misspecification and heavy-tailedness of the innovation, more resiliency to

outliers, smoothness and strict concavity of the log logistic quasi-likelihood

function, and boundedness of the influence function among others. Under some

mild conditions, we establish the strong consistency and asymptotic normality

of the LQMLE. Moreover, we propose a new and vital parameter identifiability

condition to ensure desirable asymptotics of the LQMLE. Further, based on the

LQMLE, we consider the Wald test and the Lagrange multiplier test for the

unknown parameters, and derive the limiting distributions of the corresponding

test statistics. The applicability of our methodology is demonstrated by

several time series models, including DAR, GARCH, ARMA-GARCH, DTARMACH, and

EXPAR. Numerical simulation studies are carried out to assess the finite-sample

performance of our methodology, and an empirical example is analyzed to

illustrate its usefulness.

Discussion 0