Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the estimation of high-dimensional covariance matrices under elliptical factor models with 2 + {\epsilon}th moment. For such heavy-tailed data, robust estimators like the Huber-type estimat...

We establish central limit theorems for principal eigenvalues and eigenvectors under a large factor model setting, and develop two-sample tests of both principal eigenvalues and principal eigenvecto...

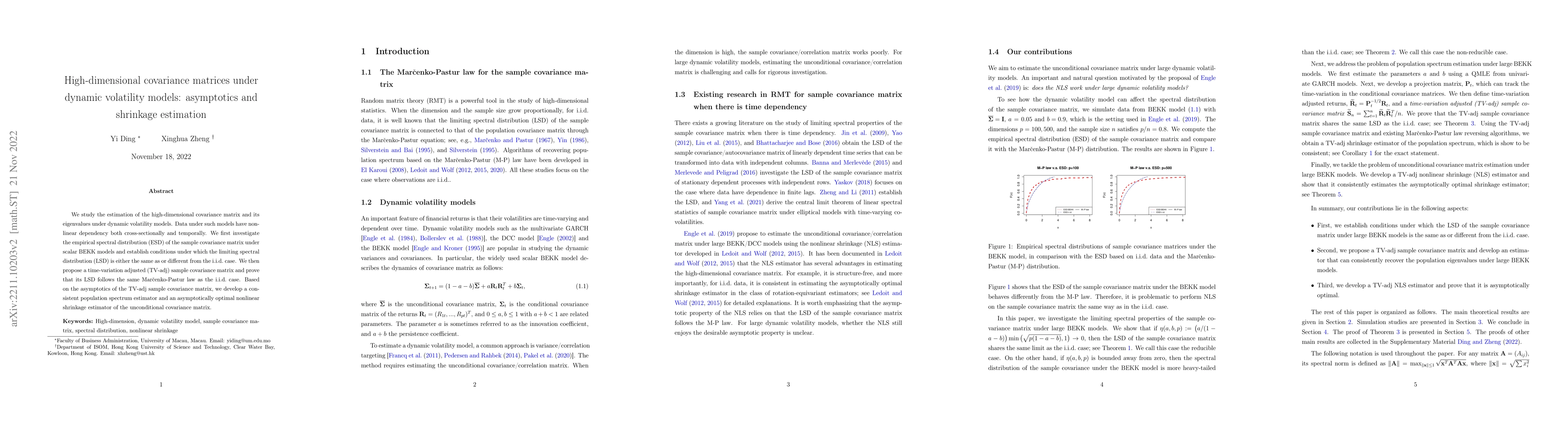

We study the estimation of the high-dimensional covariance matrix andits eigenvalues under dynamic volatility models. Data under such modelshave nonlinear dependency both cross-sectionally and tempo...

We study supercritical spatial SIR epidemics on $\mathbb{Z}^2\times \{1,2,\ldots, N\}$, where each site in $\mathbb{Z}^2$ represents a village and $N$ stands for the village size. We establish sever...

Bike Sharing Systems (BSSs) have been adopted in many major cities of the world due to traffic congestion and carbon emissions. Although there have been approaches to exploiting either bike trailers...

We consider a branching random walk on $\mathbb{Z}$ started by $n$ particles at the origin, where each particle disperses according to a mean-zero random walk with bounded support and reproduces wit...