Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider reinforcement learning for continuous-time Markov decision processes (MDPs) in the infinite-horizon, average-reward setting. In contrast to discrete-time MDPs, a continuous-time process mo...

Risk-sensitive linear quadratic regulator is one of the most fundamental problems in risk-sensitive optimal control. In this paper, we study online adaptive control of risk-sensitive linear quadrati...

Intensity control is a type of continuous-time dynamic optimization problems with many important applications in Operations Research including queueing and revenue management. In this study, we adap...

When two players are engaged in a repeated game with unknown payoff matrices, they may be completely unaware of the existence of each other and use multi-armed bandit algorithms to choose the action...

Score-based generative modeling with probability flow ordinary differential equations (ODEs) has achieved remarkable success in a variety of applications. While various fast ODE-based samplers have ...

Score-based generative models (SGMs) is a recent class of deep generative models with state-of-the-art performance in many applications. In this paper, we establish convergence guarantees for a gene...

The optimized certainty equivalent (OCE) is a family of risk measures that cover important examples such as entropic risk, conditional value-at-risk and mean-variance models. In this paper, we propo...

We study reinforcement learning for continuous-time Markov decision processes (MDPs) in the finite-horizon episodic setting. In contrast to discrete-time MDPs, the inter-transition times of a contin...

It has been recently shown in the literature that the sample averages from online learning experiments are biased when used to estimate the mean reward. To correct the bias, off-policy evaluation me...

We study the model-based undiscounted reinforcement learning for partially observable Markov decision processes (POMDPs). The oracle we consider is the optimal policy of the POMDP with a known envir...

We study the temperature control problem for Langevin diffusions in the context of non-convex optimization. The classical optimal control of such a problem is of the bang-bang type, which is overly ...

We study a multi-armed bandit problem where the rewards exhibit regime switching. Specifically, the distributions of the random rewards generated from all arms are modulated by a common underlying s...

Affine point processes are a class of simple point processes with self- and mutually-exciting properties, and they have found useful applications in several areas. In this paper, we obtain large-tim...

This paper studies optimal market making for large-tick assets in the presence of latency. We consider a random walk model for the asset price, and formulate the market maker's optimization problem ...

We propose a new reinforcement learning (RL) formulation for training continuous-time score-based diffusion models for generative AI to generate samples that maximize reward functions while keeping th...

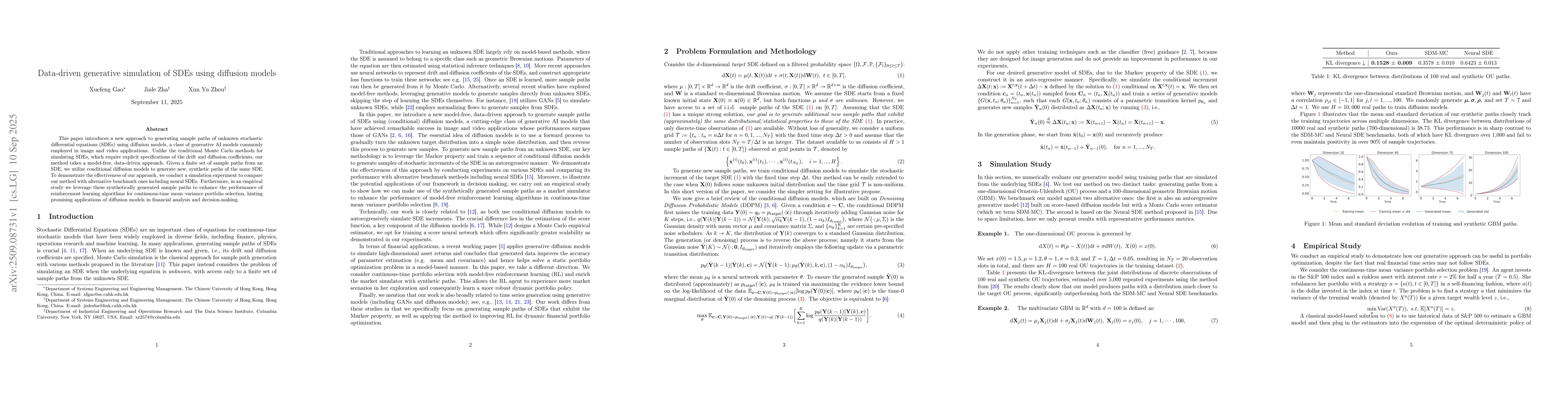

This paper introduces a new approach to generating sample paths of unknown stochastic differential equations (SDEs) using diffusion models, a class of generative AI models commonly employed in image a...

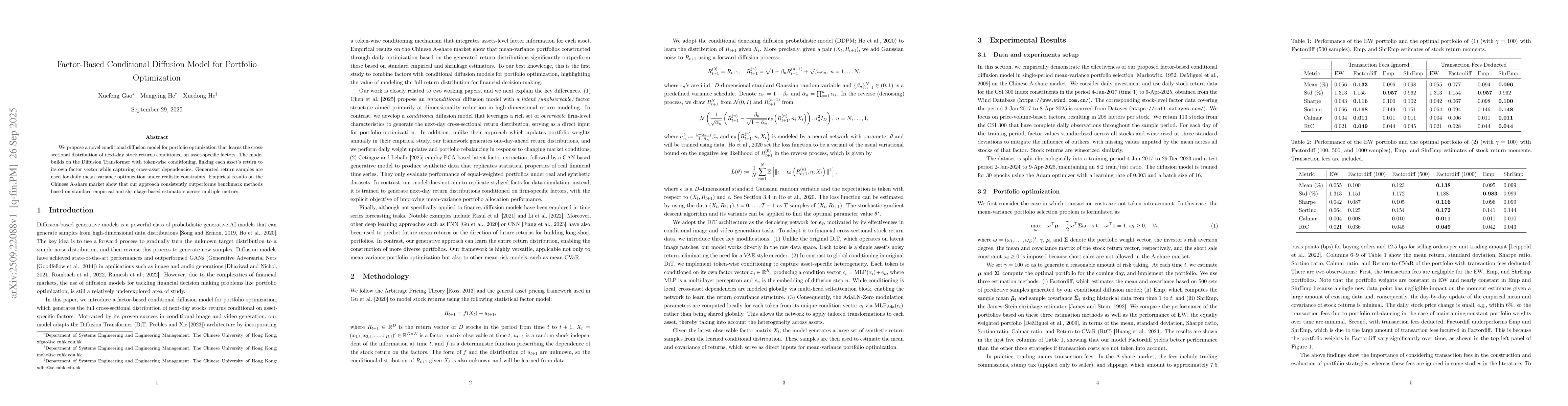

We propose a novel conditional diffusion model for portfolio optimization that learns the cross-sectional distribution of next-day stock returns conditioned on asset-specific factors. The model builds...

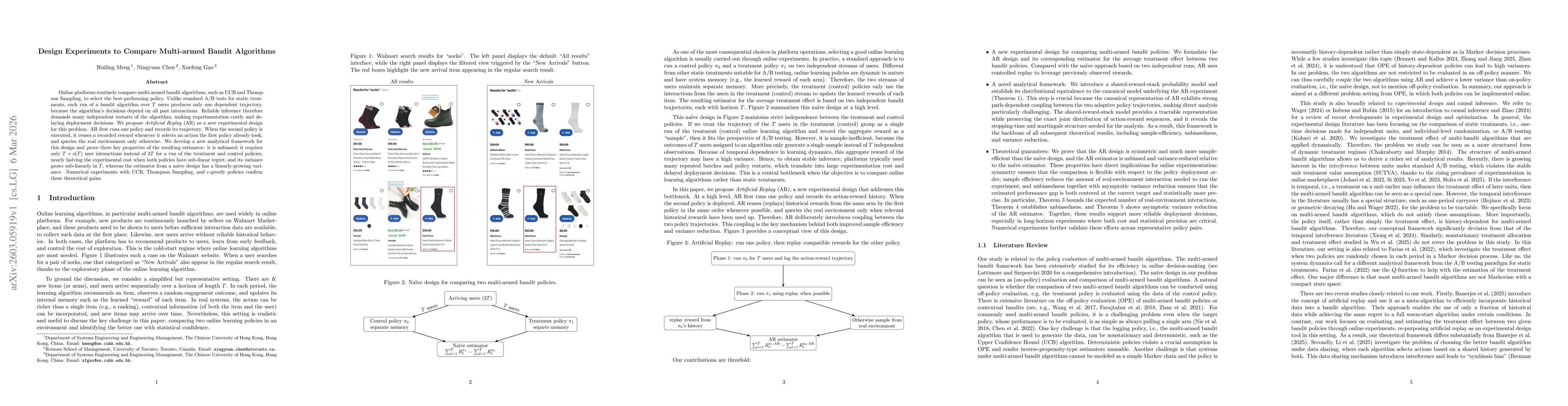

Online platforms routinely compare multi-armed bandit algorithms, such as UCB and Thompson Sampling, to select the best-performing policy. Unlike standard A/B tests for static treatments, each run of ...