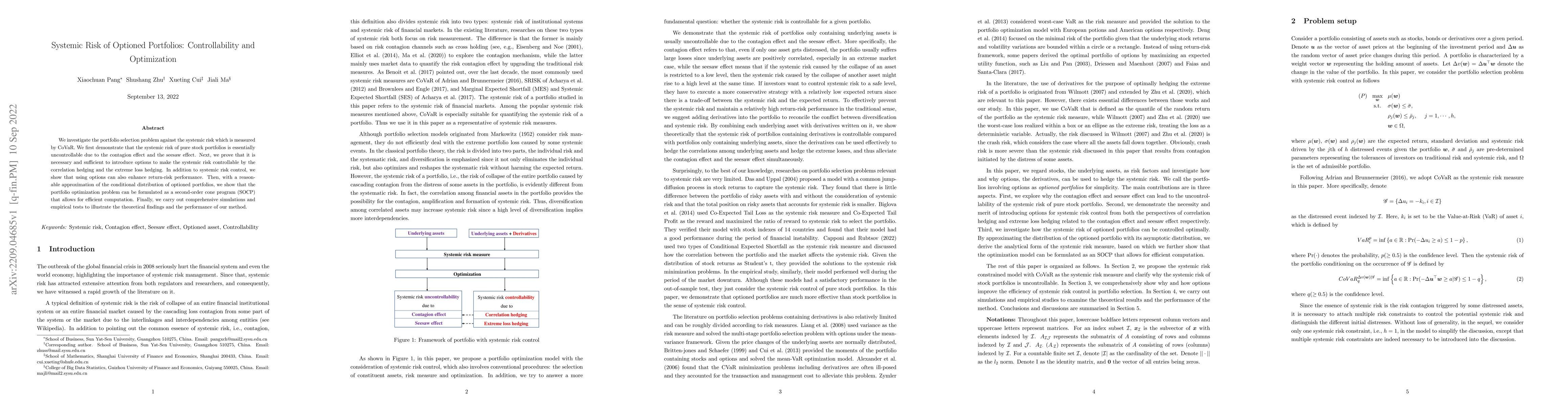

1

arXiv Papers

12

Total Publications

Profile

Academic Profile

Metrics

Statistics

1

arXiv Papers

12

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Systemic Risk of Optioned Portfolios: Controllability and Optimization

We investigate the portfolio selection problem against the systemic risk which is measured by CoVaR. We first demonstrate that the systemic risk of pure stock portfolios is essentially uncontrollabl...